Member Annual Statements are distributed to NYSLRS members each spring. Don’t wait for a mailed copy — get your Statement online instead! You can update your delivery preference in Retirement Online to receive an email when your Statement is available.

From your Account Homepage, click “update” next to ‘Member Annual Statement by.’

Choose “Email” from the dropdown.

Check and Update Your Contact Information

Retirement Online is the fastest way to check your contact information and update it if needed. If you don’t already have an email address on file, please provide it so that we can contact you quickly if we need to notify you about important information such as a change to your benefits. Use a personal email address you will have access to before and after you retire, rather than a work email address. You should also make sure your mailing address and phone number are current.

To update your contact information, click “update” next to your email address, mailing address or phone number to make corrections.

Use Retirement Online to Stay Informed

Your annual Statement is a snapshot of your NYSLRS account as of March 31. For the most up-to-date information year-round, sign in to your Retirement Online account.

In Retirement Online, you can view your date of membership, tier, retirement plan, estimated total service credit and more. Check out what else members can do in Retirement Online.

When it comes to managing your NYSLRS account, Retirement Online is the fastest way to do it. Skip printing forms, having them notarized and sending them through the mail — when you submit your requests online, NYSLRS has them immediately and your changes will be completed more quickly. It’s convenient, and it’s secure.

Here’s a look at some of the things NYSLRS members (not yet retired) can do online.

View Your Account Information

Sign in to Retirement Online for easy access to key information to help you plan for retirement. On your Account Homepage, you can find your date of membership, tier, retirement plan (which you can use to find your retirement plan publication), estimated total service credit and more.

Change Your Delivery Preference to Email and Help Us ‘Go Green’

Save time and reduce paper waste — help us ‘go green’ by choosing the paperless option. When you choose to receive information from NYSLRS electronically, we will send you an email when important documents and letters are ready to view in Retirement Online.

From your Account Homepage, click the “update” link next to ‘Contact by’ or ‘Member Annual Statement by.’

Choose “Email” from the dropdown menu.

If you choose “Email” as your delivery preference, you will not receive a printed copy in the mail.

Update Your Contact Information

It’s important that we have your current contact information so you receive the news, letters and statements that we send you. You can update your email address, mailing address and phone number in the ‘My Profile Information’ section of your Account Homepage. Just click “update” next to the item you’d like to change. Use a personal email address that you will have access to before and after you retire, rather than a work email address.

View and Update Your Beneficiary

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. It’s a good idea to review your beneficiaries from time to time to make sure your choices reflect your current wishes. Retirement Online is the fastest way to add or remove beneficiaries or update their contact information. Click the “View and Update My Beneficiaries” button to get started.

Estimate Your Pension

How much will your pension be? It’s an important question as you’re planning for retirement. In just a few steps, most members can estimate their retirement benefit based on up-to-date account information, then save or print the estimate. Entering different dates and comparing the results can help you choose the retirement date that’s right for you. From your Account Homepage, click the “Estimate my Pension Benefit” button.

Apply for a Loan and Manage Loan Payments

It’s easy to apply for a loan in Retirement Online. If you are eligible to take a loan against your retirement contributions, you can see how much you can borrow, your repayment options and whether your loan will be taxable — all before you apply. Click the “Apply for a Loan” button to start an application.

If you have an existing loan, you can click the “Manage My Loans” button to adjust your payment amount or to make an additional one-time payment.

Request Credit for Previous Service

If you worked for a participating public employer before joining NYSLRS, or if you served in the U.S. Armed Forces, you may be able to purchase service credit for that time. Click the “Manage My Service Credit Purchases” button to request credit and upload any supporting documentation.

Purchase previous service credit as soon as possible. It’s cheaper and will make it easier to calculate your final monthly pension payment.

Get Your Member Annual Statement Faster

Your Member Annual Statement can help you understand your benefits. It’s a snapshot of your NYSLRS account based on the information we have on file for you as of March 31 each year, the close of our fiscal year. Statements will be available online in the spring, sooner than printed copies will be mailed — update your delivery preference to “Email” to get notified when it’s available online.

Generate a Mortgage Verification Letter

If you need to provide proof of your NYSLRS account information for a mortgage, you can get your own income verification letter online. From your Account Homepage, in the ‘I want to…’ section at the top right, click the “Generate Income Verification Letter” link. You can print a document that shows your contribution balance, and — if you have an outstanding loan — the date of your last loan, the current balance and the interest rate.

Apply for Retirement

When you are ready to retire, Retirement Online allows you to skip the hassle of mailing paper forms or visiting our office. You can apply for a service retirement benefit, choose your pension payment option, sign up for direct deposit and submit retirement-related paperwork online. A big advantage of applying online is that you don’t have to get anything notarized. Read our blog post about applying for retirement for more information and links to resources.

Other Online Transactions

If you previously were a member of another New York State public retirement system before joining NYSLRS, your service could be recredited and your date of membership and tier restored. You can click the “Reinstate a Previous Membership” button to get started.

If you leave public employment with less than ten years of service credit, you can use Retirement Online to withdraw your membership. However, this will terminate your membership with NYSLRS. If you have any questions, speak with a customer service representative before you submit your withdrawal application. You can message them using our secure contact form.

Your Member Annual Statement is a snapshot of your NYSLRS account with information about your NYSLRS membership and benefits. It is based on the information we have on file for you as of March 31, 2023, the end of our fiscal year.

You can view your 2023 Statement now by signing into Retirement Online. From your Retirement Online Account Homepage, go to the ‘My Account Summary’ area, click the “View My Member Annual Statement” button and follow the steps to view, print or save your Statement. Don’t have an account? Register today. If you need help signing in to your account, these tools and tips will come in handy.

Delivery of Your Member Annual Statement

If you chose email delivery of your Statement, you should receive an email informing you that your Statement is ready to be viewed in Retirement Online. All other members will receive their 2023 Statement by mail before the end of June.

Get Up-to-Date Account Information Year Round

Your Member Annual Statement provides information as of March 31, 2023, but with Retirement Online you can access up-to-date information about your retirement account year-round. Sign in to see the date you joined NYSLRS, your tier, your retirement plan and your current total estimated service credit. Retirement Online is also the fast, easy way to conduct business securely with NYSLRS. Here are some of the things you can do:

Pension Estimates: Most members can create customized benefit estimates and calculate their pension payment options using Retirement Online. From your Account Homepage, scroll down to ‘My Account Summary’ and click the “Estimate my Pension Benefit” button. You can base your estimate on the salary and service information we have on file or adjust your earnings or service credit to account for possible increases in earnings or service credit purchases. By entering different retirement dates and beneficiaries, you will see how your choices affect your potential benefit. If you are not able to use the Retirement Online calculator, contact us for an estimate.

Employment History: You can view your recent employment history and reported earnings for the past five years in Retirement Online. From your Account Homepage, scroll down to ‘My Account Summary’ and click the “View My Recent Employment Summary” button. Think you may be eligible for past service that’s not included in your employment history? You can request to purchase service credit by returning to ‘My Account Summary’ and clicking the “Manage My Service Credit Purchases” button.

Contact Information Change: Did you move or change your email address recently? On your Account Homepage, in the ‘My Profile Information’ section, you can update your address and other contact information.

Update Your Delivery Preference for Next Year

Want to be notified by email next year when your Statement is ready? Sign in to Retirement Online to change your Statement delivery preference. Go to the ‘My Profile Information’ section on your Account Homepage, click “update” next to ‘Member Annual Statement By,’ then choose “email” from the dropdown menu.

Have Questions About Your Member Annual Statement?

Visit our Member Annual Statement page for answers to common questions or to find out how to correct any errors.

Reminder for retirees: Retiree Annual Statements were mailed at the end of February and are not yet available online.

If you have general questions about NYSLRS or your benefits, we have a web page that can help you find the answers.

That’s because the NYSLRS Contact Us page does double duty. It not only lists contact information, it also helps you find answers for many of the common questions we get from members, retirees and beneficiaries. It covers subjects like address changes, loans, pension estimates, direct deposit and cost-of-living adjustments (COLA).

To get started, go to the Contact Us page and select the Member, Retiree or Beneficiary button to find the questions and answers you need. Each section has categories specific to that member group.

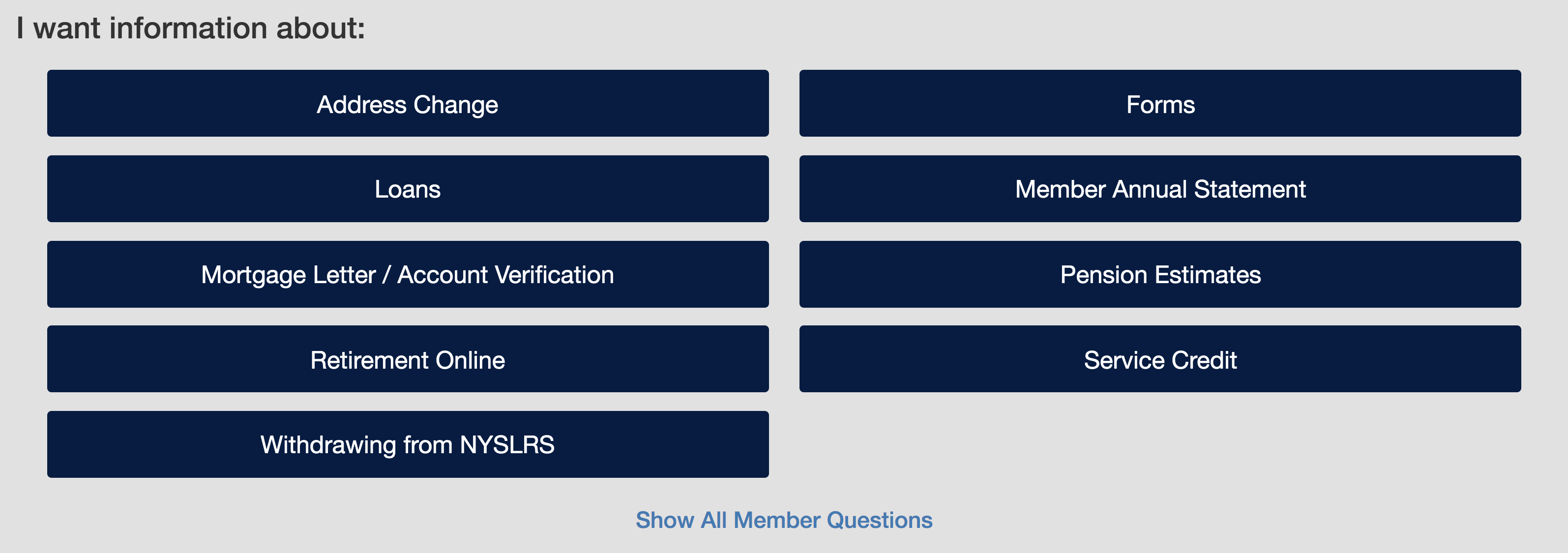

Member

Address Change

Forms

Loans

Member Annual Statement

Mortgage Letter/Account Verification Letter

Pension Estimates

Retirement Online

Service Credit

Withdrawing from NYSLRS

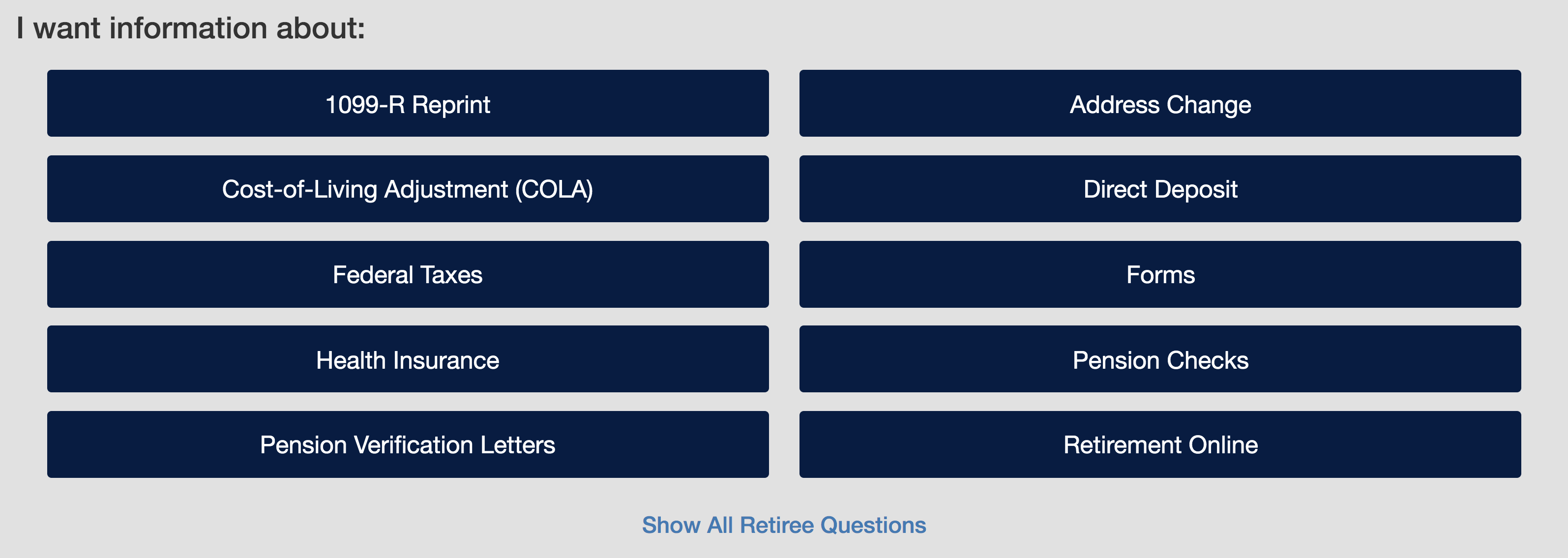

Retiree

1099-R Reprint

Address Change

Cost-of-Living Adjustment (COLA)

Direct Deposit

Federal Taxes

Forms

Health Insurance

Pension Checks

Pension Verification Letters

Retirement Online

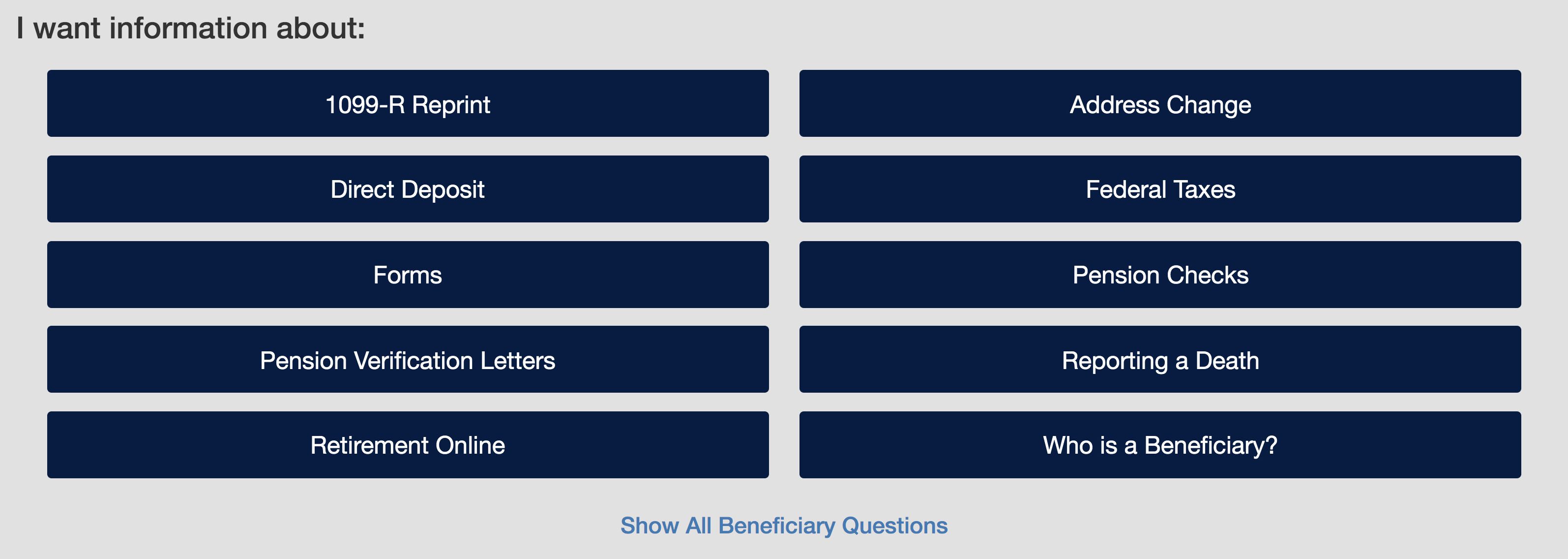

Beneficiary

1099-R Reprint

Address Change

Direct Deposit

Federal Taxes

Forms

Pension Checks

Pension Verification Letters

Reporting a Death

Retirement Online

Who is a Beneficiary?

Getting Account-Specific Answers

The information on the Contact Us page is general. If you’re looking for information specific to your situation, like your loan balance or a breakdown of your pension payment, sign in to Retirement Online. If you don’t already have a Retirement Online account, sign up today.

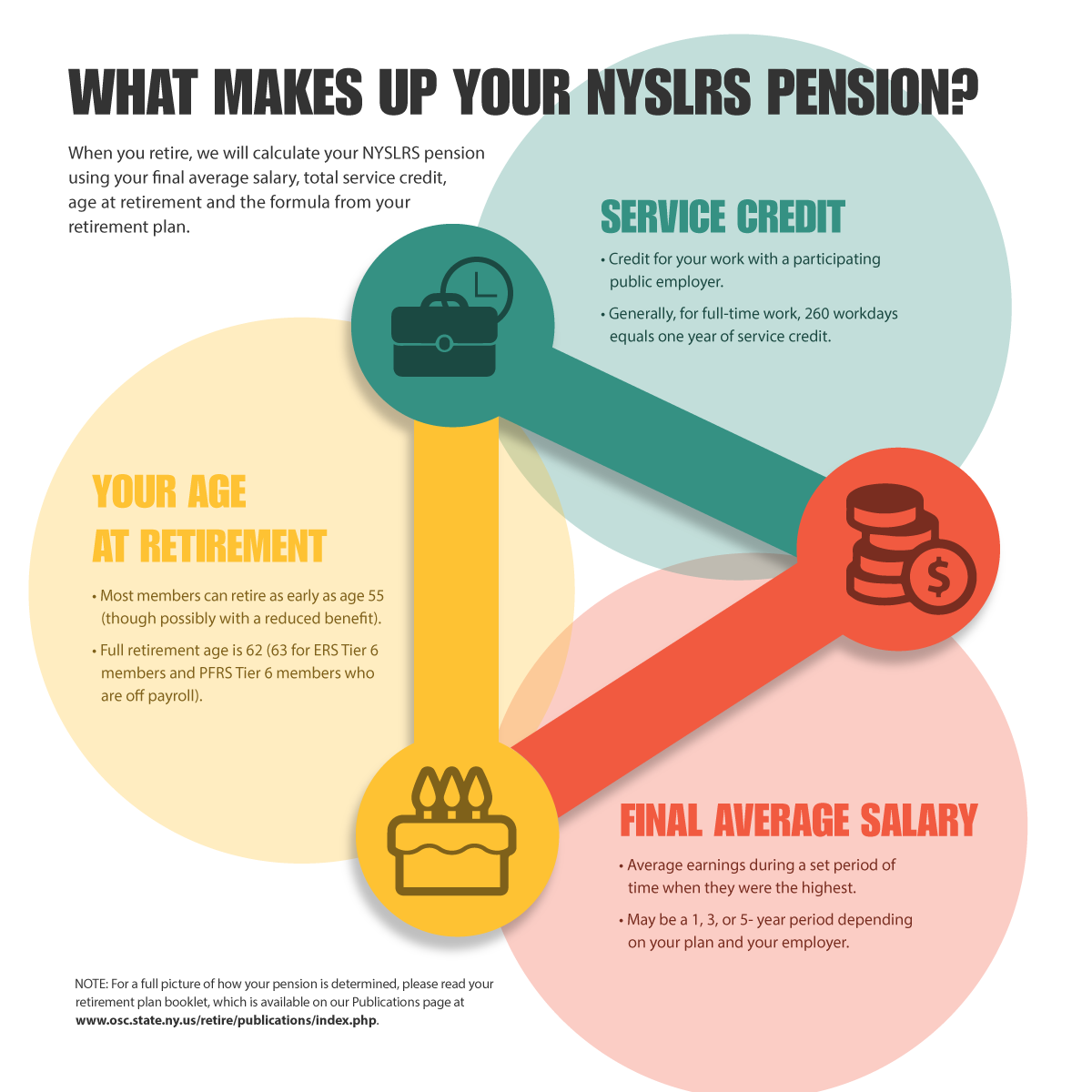

Generally, three main components determine your NYSLRS pension: your retirement plan, your final average salary (FAS) and your total service credit.

Your Retirement Plan

NYSLRS retirement plans are established by law. Your plan lays out the formula we’ll use to calculate your pension as well as eligibility requirements. It’s important to read your plan booklet, which you can find on our Publications page. If you aren’t certain what retirement plan you’re in, check your Member Annual Statement or ask your employer.

Final Average Salary

Your FAS is the average of your earnings during the set period of time when they were the highest. For ERS and PFRS members in Tiers 1 through 5, that period is three consecutive years; for Tier 6 members, it’s five consecutive years. Some PFRS members may be eligible for a one-year period, if their employer offers it. We will use your FAS, age at retirement, total service credit and the formula from your retirement plan to calculate your NYSLRS pension.

Generally, the earnings we can use for your FAS include regular salary, overtime and recurring longevity payments earned within the period. Some payments you receive won’t count toward your FAS, even when you receive them in the FAS period. The specifics vary by tier, and are listed in your retirement plan booklet.

In most cases, the law also limits how much your pensionable earnings can increase from year to year in the FAS period. Earnings above this cap will not count toward your pension.

Our Your Retirement Benefits publications, (ERS and PFRS), provide the limits for each tier and examples of how we’ll determine your FAS.

Service Credit

Service credit is credit for time spent working for a participating public employer. For most members who work full-time, 260 workdays equals one year of service credit. Members who work part-time or in educational settings can refer to their retirement plan publication for their service credit calculation.

Service credit is a factor in the calculation of your NYSLRS pension. Generally, the more credit you have, the higher your pension will be. Some special plans (usually for police officers, firefighters or correction officers) let you retire at any age once you’ve earned 20 or 25 years of service credit. In other plans, if you retire without enough service credit and don’t meet the age requirements of your retirement plan, your pension will be reduced.

Planning Ahead for Your NYSLRS Pension

As you get closer to retirement age, keep an eye on your service credit and FAS. Make sure we have an accurate record of your public employment history. You can sign in to Retirement Online or check your latest Member Annual Statement to see the total amount of service credit you’ve earned. You may also want to take a look at our budgeting worksheet or try our Benefit Projector Calculator as you plan for your retirement.

If you have questions, or want to find out more information about what makes up your NYSLRS pension, please contact us.

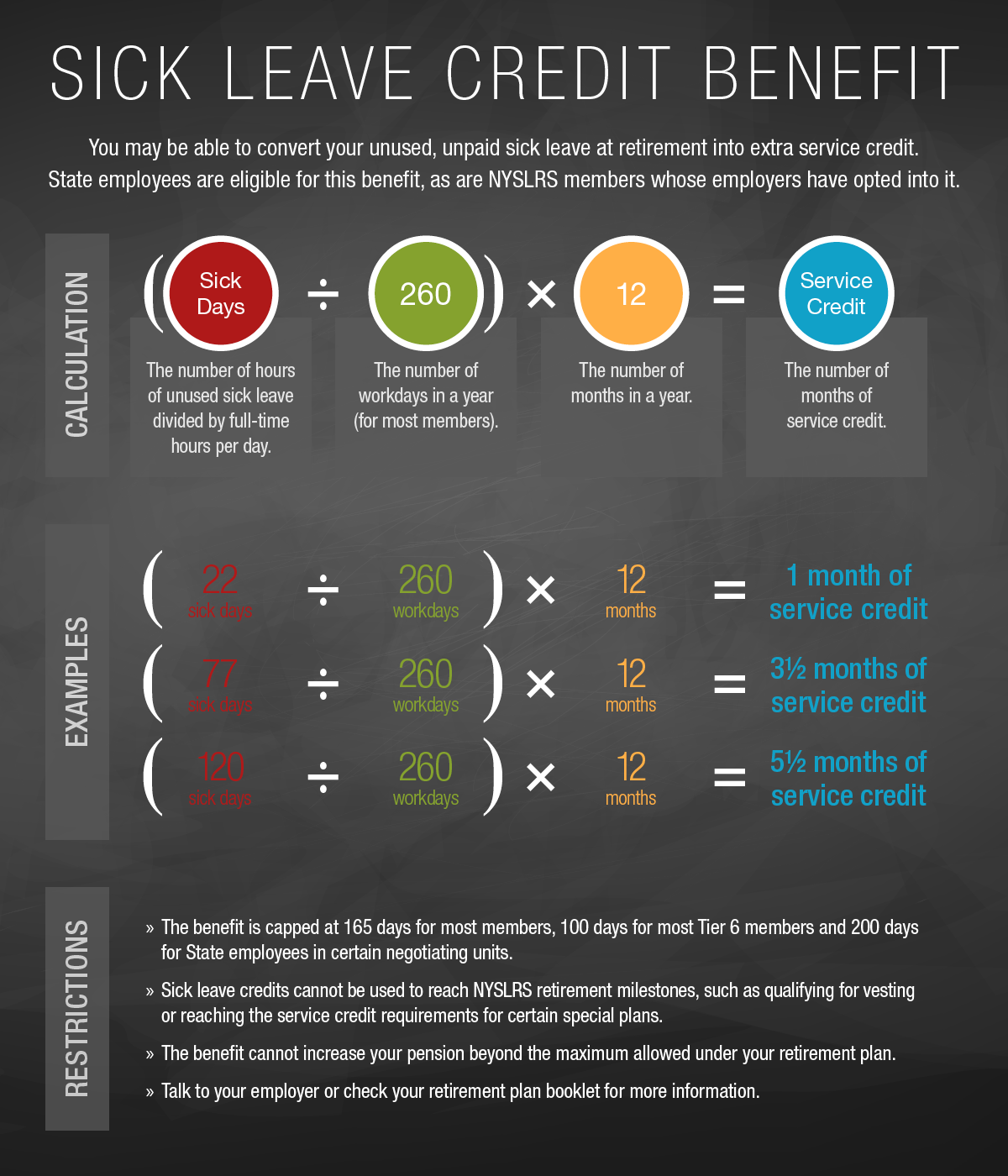

If you’ve accumulated unused, unpaid sick leave, you may be able to use it toward your NYSLRS pension benefit.

New York State employees are eligible for this benefit. You also may be eligible if your employer has adopted Section 41(j) for the Employees’ Retirement System (ERS), or 341(j) for the Police and Fire Retirement System (PFRS), of Retirement and Social Security Law. Not sure? Ask your employer or check your Member Annual Statement.

Here’s How It Works

Your additional service credit is determined by dividing your total unused, unpaid sick leave days by 260. Most ERS members can get credit for up to 165 days (7½ months) of unused sick leave. The benefit is capped at 100 days (4½ months) for most Tier 6 members. State employees in certain negotiating units may be able to use 200 days (about nine months). Those extra “months” would be used in calculating your retirement benefit.

Also, depending on your employer, your unused sick leave may be used to cover some health insurance costs during your retirement. Please check with your employer for information about health insurance.

Restrictions

Unused sick leave cannot be used to reach NYSLRS retirement milestones. Let’s say you have 19½ years of service credit. At 20 years, your pension calculation would improve substantially. You also have 130 days of unused sick leave. Can you add the six months of sick leave credit to get you to 20 years? No. Retirement law does not permit it. You’ll have to work those extra six months to get the 20-year benefit rate, though sick leave credits can still be used in your final pension calculation.