As a NYSLRS member, your defined benefit pension plan is a good reason to be optimistic about your finances when you retire. Your pension will provide you with monthly payments for the rest of your life. But there is more to a financially secure retirement than having a pension. Understanding your potential sources of income will help you plan for your future and boost your retirement confidence.

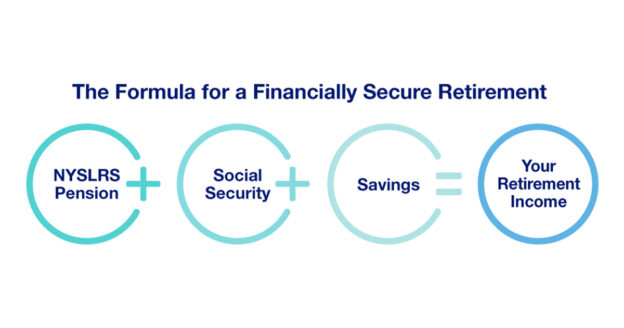

Think of retirement security as a three-legged stool. Each leg is a source of income to help support you when your working days are done.

Leg 1: Your NYSLRS Pension

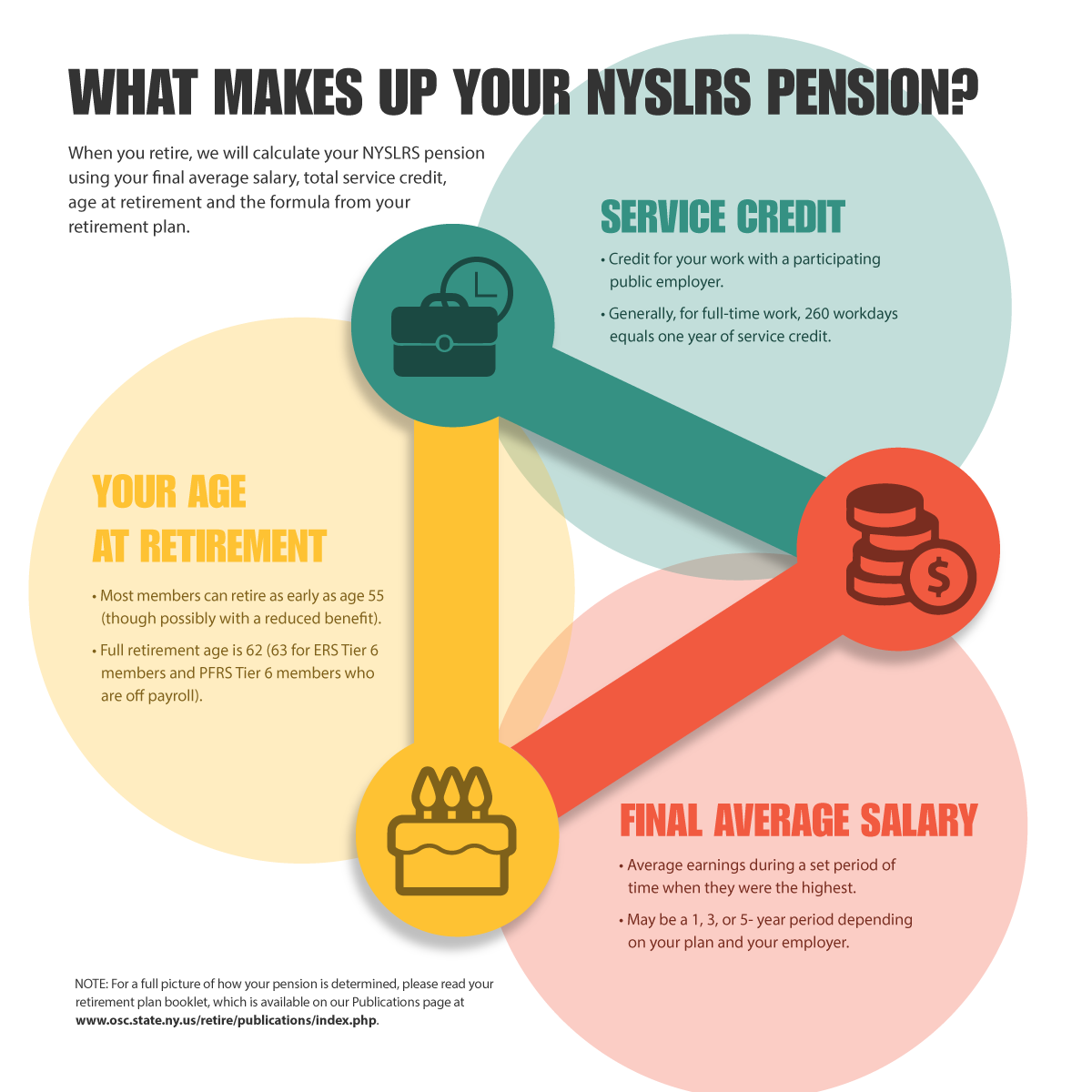

At retirement, vested NYSLRS members are eligible for a pension based on their final average earnings and the number of years they’ve worked in public service. Your NYSLRS pension provides you with a monthly payment for the rest of your life, no matter how long you live. Unlike workers who rely on a 401(k)-style retirement plan, you won’t have to worry about this income running out.

Most members can use Retirement Online to estimate how much their pension will be. But, if you’re a long way from retirement, it may be better to think in terms of earnings replacement. Financial advisers estimate you’ll need to replace 70 to 80 percent of your income to retire with confidence. Your pension can help get you there. For example, if you retire with 30 years of service, your NYSLRS pension could replace more than half of your earnings. (Pension benefits depend on your tier and retirement plan. Look up your retirement plan publication to find out how your retirement benefit will be calculated.)

Leg 2: Social Security

Your Social Security benefit is another source of income to help support you in retirement. It replaces a percentage of your pre-retirement income. At full retirement age, your social security benefit can replace from about 75 percent for lower income earners to about 27 percent for higher income earners. Visit Social Security’s Plan for Retirement page to estimate your income and learn more about your benefit.

Leg 3: Retirement Savings Can Boost Your Confidence

A lifetime pension and Social Security income will be substantial financial assets, but it’s still important to save for retirement. A healthy retirement savings will give you more flexibility during retirement, helping to ensure that you’ll be able to do the things you want to do. It can also help in case of an emergency and act as a hedge against inflation.

Saving is the retirement factor you have the most control over. You decide when to start, how much to save and how to invest your money. The key is to start saving early so your money has time to grow, even if you can only afford to save a small amount in the beginning.

Eligible employees might consider saving with the New York State Deferred Compensation Plan (NYSDCP). Money gets deducted from your paycheck so you won’t even have to think about it. NYSDCP is not affiliated with NYSLRS, but New York State employees and some municipal employees can participate. If you’re a municipal employee, ask your employer whether you’re eligible for NYSDCP or another retirement savings plan.