Financial advisers say you will need to replace between 70 and 80 percent of your salary to maintain your lifestyle after retirement. Your NYSLRS pension could go a long way in helping you reach that goal, especially when combined with your Social Security benefit and your own retirement savings. Here’s a look at how Employees’ Retirement System (ERS) members in Tier 6 (who are vested once they’ve earned five years of credited service), can reach that goal. Members who joined NYSLRS since April 1, 2012 are in Tier 6.

Calculating an ERS Tier 6 Member’s Pension

Your NYSLRS pension will be based on your Final Average Earnings (FAE) and the number of years you work in public service. FAE is the average of the five highest-paid consecutive years. Note: The law limits the FAE of all members who joined on or after June 17, 1971. For example, for most members, if your earnings increase significantly through the years used in your FAE, some of those earnings may not be used toward your pension.

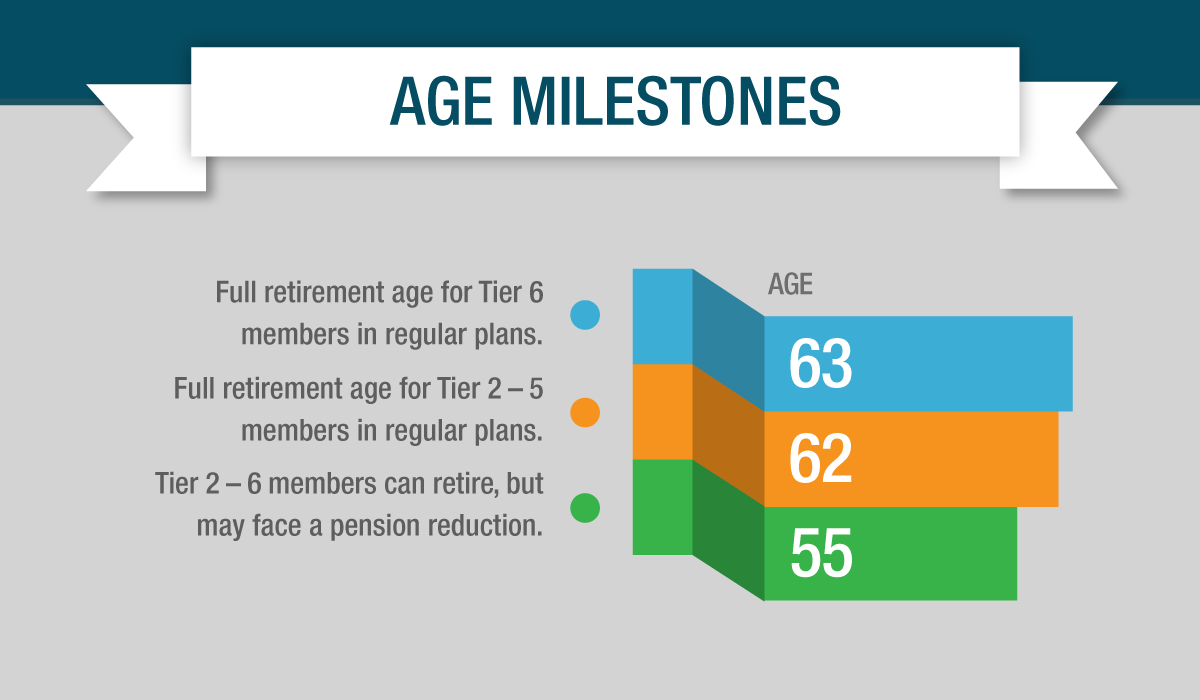

Although ERS members can generally retire as early as age 55 with reduced benefits, the full retirement age for Tier 6 members is age 63.

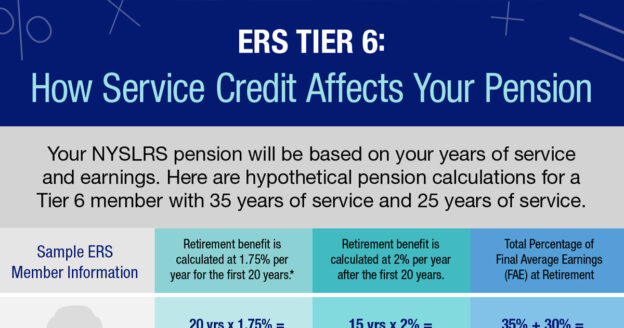

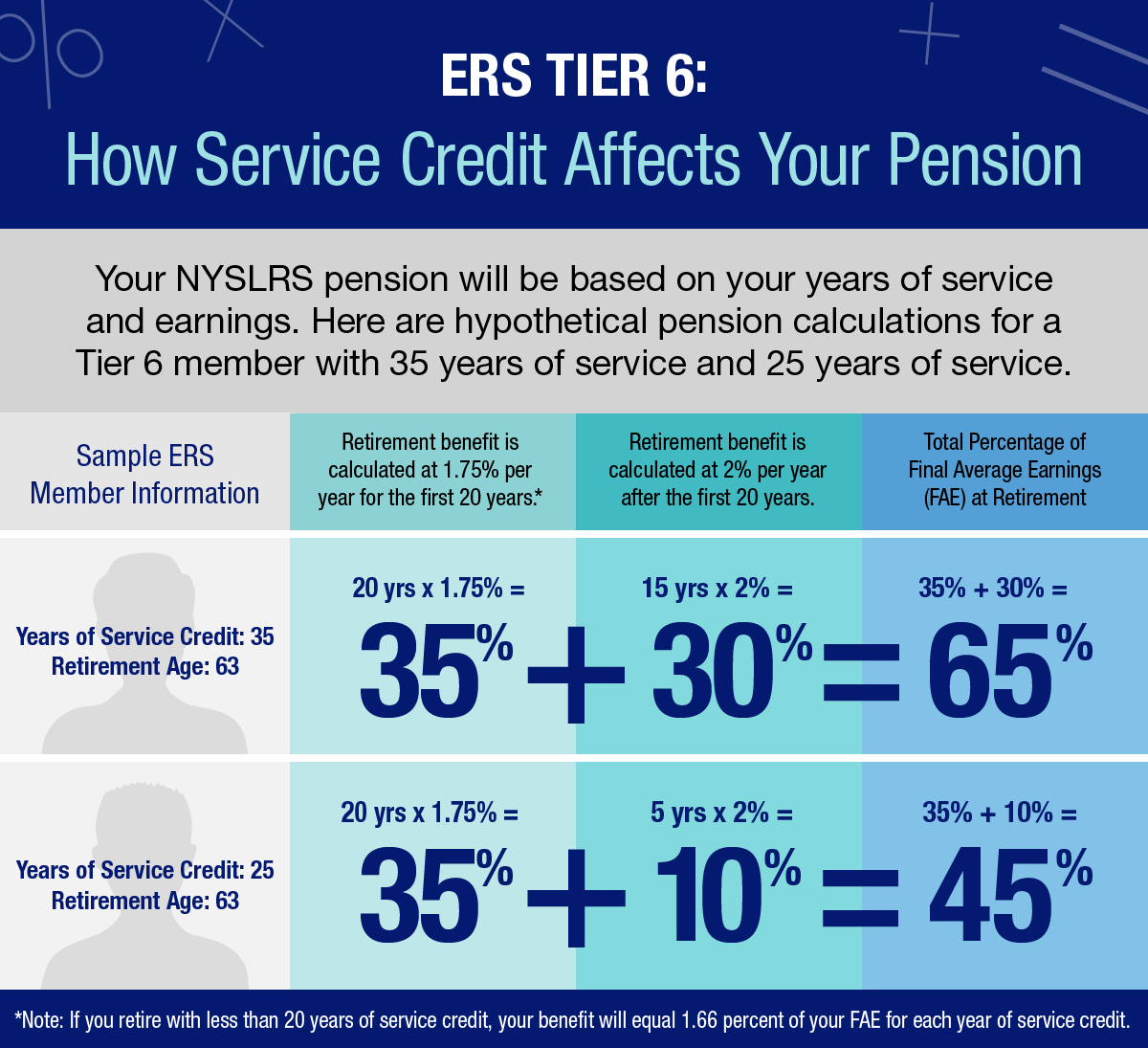

For ERS Tier 6 members in regular plans (Article 15), the benefit is 1.66 percent of your FAE for each full year you work, up to 20 years. At 20 years, the benefit equals 1.75 percent per year for a total of 35 percent. After 20 years, the benefit grows to 2 percent per year for each additional year of service. (Benefit calculations for members of the Police and Fire Retirement System and ERS members in special plans vary based on plan.)

Say you begin your career at age 28 and work full-time until your full retirement age of 63. That’s 35 years of service credit. You’d get 35 percent of your FAE for the first 20 years, plus 30 percent for the last 15 years, for a total benefit that would replace 65 percent of your salary. If you didn’t start until age 38, you’d get 45 percent of your FAE at 63.

So, that’s how your NYSLRS pension can help you get started with your post-retirement income. Now, let’s look at what the addition of Social Security and your own savings can do to help you reach your retirement goal.

Other Sources of Post-Retirement Income

Social Security: According to the Social Security Administration, Social Security currently replaces about 40 percent of the wages of a typical worker who retires at full retirement age. In the future, these percentages may change, but you should still factor it in to your post-retirement income.

Your Savings: Retirement savings can also replace a portion of your income. How much, of course, depends on how much you save. The key is to start saving early so your money has time to grow. New York State employees and some municipal employees can participate in the New York State Deferred Compensation Plan. If you haven’t already looked into Deferred Compensation, you might consider doing so now.

After months or years of retirement planning, you’re probably looking forward to the day when you

After months or years of retirement planning, you’re probably looking forward to the day when you

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines