When you retire from NYSLRS, you’ll need to decide how you want to receive your pension benefit.

You’ll have several pension payment options to choose from. All of them will provide you with a monthly benefit for life. Some provide a limited benefit for one or more beneficiaries after you die. Others let you pass on a monthly lifetime pension to a single beneficiary. Each option pays a different amount, depending on your age at retirement, your beneficiary’s age and other factors.

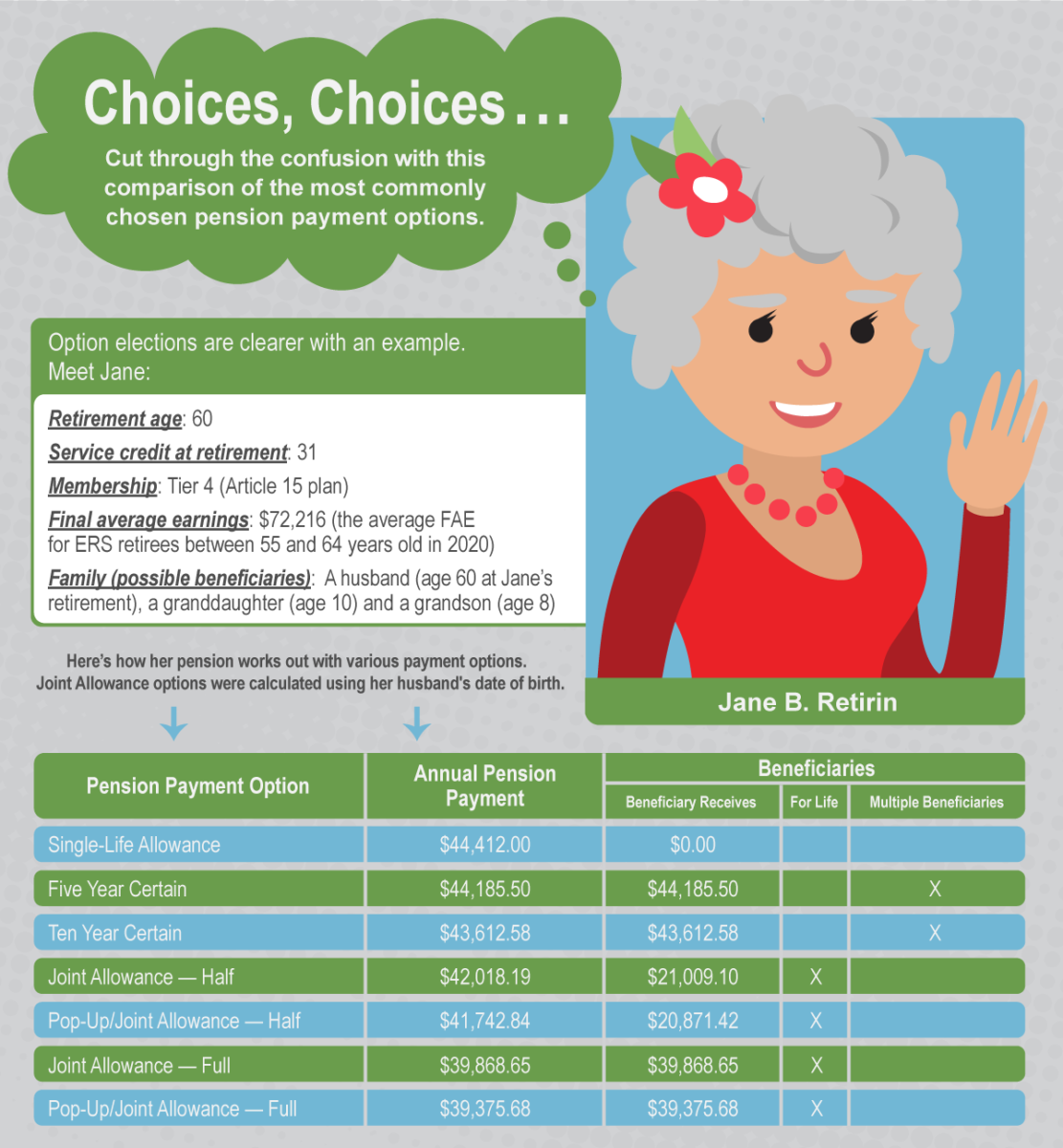

That’s a lot to think about, so let’s make this clearer with an example.

Meet Jane. Jane plans to retire at age 60, and she has a husband, a granddaughter and a grandson who are financially dependent on her. First, Jane needs to decide whether she wants to leave a benefit to someone after she dies. She does.

That eliminates the Single-Life Allowance option. While it pays the highest monthly benefit, all payments stop when you die.

Jane considers naming her grandchildren as beneficiaries to help pay for their college education.

The Five Year Certain and Ten Year Certain options don’t reduce her pension much, and they allow her to name more than one beneficiary. If Jane dies within five or ten years of retirement, depending which option she chooses, her grandkids would split her reduced benefit amount for the rest of that period.

However, the Five and Ten Year Certain options wouldn’t be lifetime benefits, and since her husband doesn’t have his own pension, she decides to leave him a lifetime pension benefit and look into a tax-deferred college savings plan for her grandkids instead.

There are several options that leave a lifetime benefit. Under these options, you can only name one beneficiary. Benefit amounts are determined based on the birth dates (life expectancy) of both the retiree and their beneficiary, so Jane will receive less of a pension reduction leaving a benefit to her husband than she would if she were to consider leaving a lifetime benefit to a grandchild.

Under the Joint Allowance — Full or Joint Allowance — Half option, if a retiree dies, depending which option they choose, their beneficiary would receive half or all of their reduced benefit for life.

Under the Pop-Up/Joint Allowance — Full or Pop-Up/Joint Allowance — Half option, if a retiree dies, depending which option they choose, their beneficiary would also receive half or all of their reduced benefit. These options reduce the pension a little more, but they have an advantage: If the retiree outlives his or her beneficiary, the retiree’s monthly payment will “pop up” to the maximum payable under the Single-Life Allowance option.

As you plan for your own retirement and whether you’ll leave a pension benefit to a beneficiary or beneficiaries, you may also want to consider questions such as:

- Do you qualify for a death benefit?

- Do you have life insurance?

- Do you have a mortgage, unpaid loans or other monthly payments that will have to continue to be paid if you die?

These and other factors can significantly impact your retirement planning.

To find out more about pension payment options, check your retirement plan booklet on our Publications page. Most NYSLRS members can also create their own pension estimate in minutes using Retirement Online. You can enter different retirement dates to see how those choices would affect your benefit. When you’re done, you can print your pension estimate or save it for future reference.

Is there an insurance ‘policy’ with retirement?

NYSLRS does not offer life insurance, but most NYSLRS members are eligible for a post-retirement death benefit if they retire directly from payroll or within one year of leaving covered employment. The post-retirement benefit is a percentage of the benefit available during your working years. Death benefits vary by tier and retirement plan. You can find general information about death benefits on our website.

For information about how this may apply in your situation, please email our customer service representatives using our secure email form. Filling out the secure form allows them to safely contact you about your personal account information.

May I ask that you give an example that is more real life. On LI, most of your canvas letters are starting at $32K. 15 to 20 years is the new “norm” for tier 6. At 2-3% annual increase (which is pretty generous) , the person would be lucky if they even make $55 grand after those 15/20 yrs.

Most members can use the benefit calculator in Retirement Online to estimate their pensions based on information we have on file for them. Sign in to your account (https://web.osc.ny.gov/retire/sign-in.php), go to the My Account Summary area of your Account Homepage and click the “Estimate my Pension Benefit” button.

Can a trust be a beneficiary?

Thank you.

You can name a trust as the beneficiary of your death benefit. You can find more information in our publication, Why Should I Designate a Beneficiary?

If you have questions, please email our customer service representatives using our secure email form. Filling out the secure form allows them to safely contact you about your personal account information.

What about a 10% popup? May I have a form for that option? I was told on the phone one can do that?

NYSLRS will consider requests for alternative pension payment options. You must submit in writing a detailed outline of your request, which would then be reviewed by NYSLRS for legal and actuarial soundness.

If you are considering an alternative payment option, we recommend you speak to one of our customer service representatives for details. You can call our representatives at 1-866-805-0990 (or 518-474-7736 in the Albany, NY area), press 2, then follow the prompts. You can also email them using our secure email form. Filling out the secure form allows them to safely contact you about your personal account information.

Continue using Jane as the same example as above…what would the figures be if she had not husband and wanted to name one grandchild as a beneficiary ?

Beneficiary calculations are based on life expectancy, so if she were to pick a grandchild as a beneficiary, the monthly benefit amount would be reduced.

If you are considering naming a child or grandchild as a beneficiary, you can use the pension benefit estimator in Retirement Online. Sign in to Retirement Online and from your account homepage, click the “Estimate my Pension Benefit” button.

Yes I realize that.

Can you provide the amount Jane’s grandchild who is 9 years old would received if the child was the only beneficiary based on NYSLRS’s example of how long Jane has worked and Jane’s final average salary.

I retired in June of 2021. Just recieved my 4th retirement check. When will I get my final check amount with my final numbers. Is the retirement system still 2 years behind figuring out our final numbers and getting us our back pay ?

For questions about current processing times, please email our customer service representatives using the secure email form on our website (http://www.emailnyslrs.com).

Now that the Gov classified 911 Dispatchers First Responders – What is the status of a 25 year retirement plan? like nypd and fdny comm’s center rec’d years ago, the rest of the state is supp to piggy back off of their plan now. that’s what we were told anyways.

To see if your employer is offering a 25-year retirement plan with NYSLRS, we recommend contacting your Human Resources department.

they are telling me to contact you, you are telling me to contact them this is the problem in NYS pass the buck. Last I checked NYS is my retirement system since (1989) and oversees Tier 4 public employees.

If your employer decides to adopt a 25-year retirement plan, NYSLRS would administer that plan.

For questions about your existing retirement benefits, please contact our customer service representatives. You can email them using the secure email form on our website (http://www.emailNYSLRS.com). One of them will review your account and respond to your questions. Filling out the secure form allows them to safely contact you about your personal account information.

thank you…

I have issues with days reporting to service credit.Who is reporting days to service credit I have to find out.

Your employer provides us with your days worked, and we use that data to determine your service credit.

For other questions about your service credit, please email our customer service representatives using the secure email form on our website. One of them will review your account and respond to your questions. Filling out the secure form allows them to safely contact you about your personal account information.