Are you a current New York State & Local Retirement System (NYSLRS) member working at a new job in the public sector? Even though you’re already a member, make sure your new employer sends us a membership application for you.

The Importance of Filing a New Membership Application

By sending a new membership application, your employer provides us with updated information about your membership, like the start date of your new position and your job title. But, it’s important for other reasons as well. Up-to-date member information:

- Ensures that your employment history and benefit projection are accurately reported in your Member Annual Statement;

- Helps guarantee that benefit determinations are based on the most current information;

- Highlights any delays between when you began working and when your employer started reporting you;

- Ensures that we will receive the correct contribution amount for your membership; and

- Allows us to update your retirement plan in our records, should you change plans as a result of your new employment.

Starting a new public sector job is also a good opportunity to update your beneficiary information . You should check your beneficiaries regularly to make sure any benefits will be paid according to your wishes. Payments are made to the last named beneficiary.

Retirement Online is the convenient and secure way to review and update your beneficiary information. Register or Sign In , and then click “Update My Beneficiaries.”

Being a Friend

While you have applications on your mind, think about any friends or coworkers you may have. Perhaps, like you, they have recently changed jobs. Remind them to make sure their employers submit new applications.

Or, maybe you know a coworker who isn’t a mandatory member of NYSLRS, but who has that option. Suggest they consider joining NYSLRS.

It’s a good idea to join even if you aren’t sure you’ll ever apply for a benefit. By becoming a NYSLRS member, you lock in your tier and protect your benefits. And, if you do decide to leave public employment and withdraw your membership, you’ll receive 5 percent on your contributions, which can be a competitive return.

For more information about the benefits of NYSLRS membership, check out our Membership in a Nutshell publication.

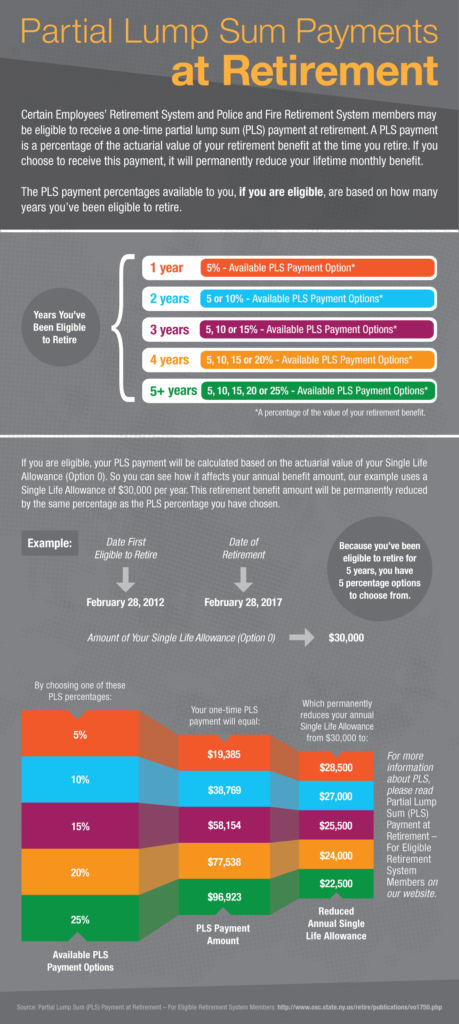

How the Partial Lump Sum Payment Works

How the Partial Lump Sum Payment Works

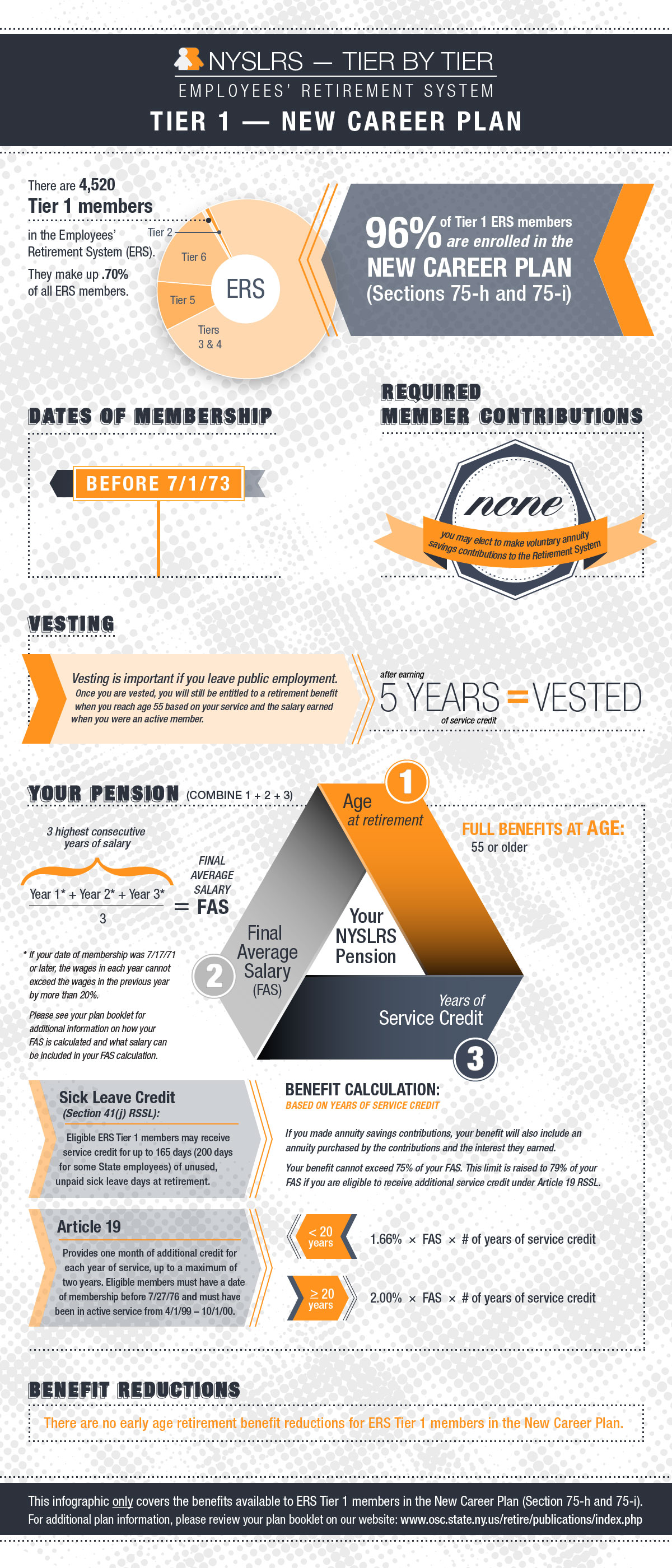

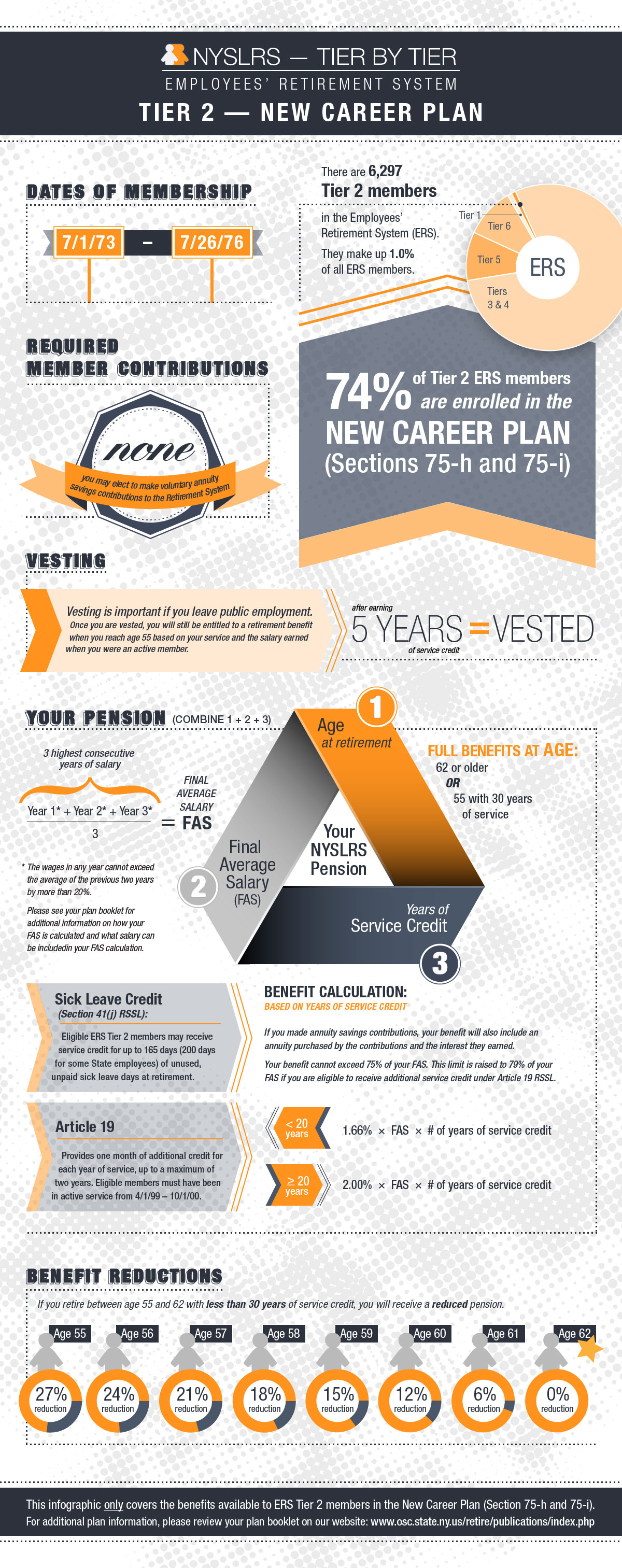

Filing Forms with the Comptroller

Filing Forms with the Comptroller