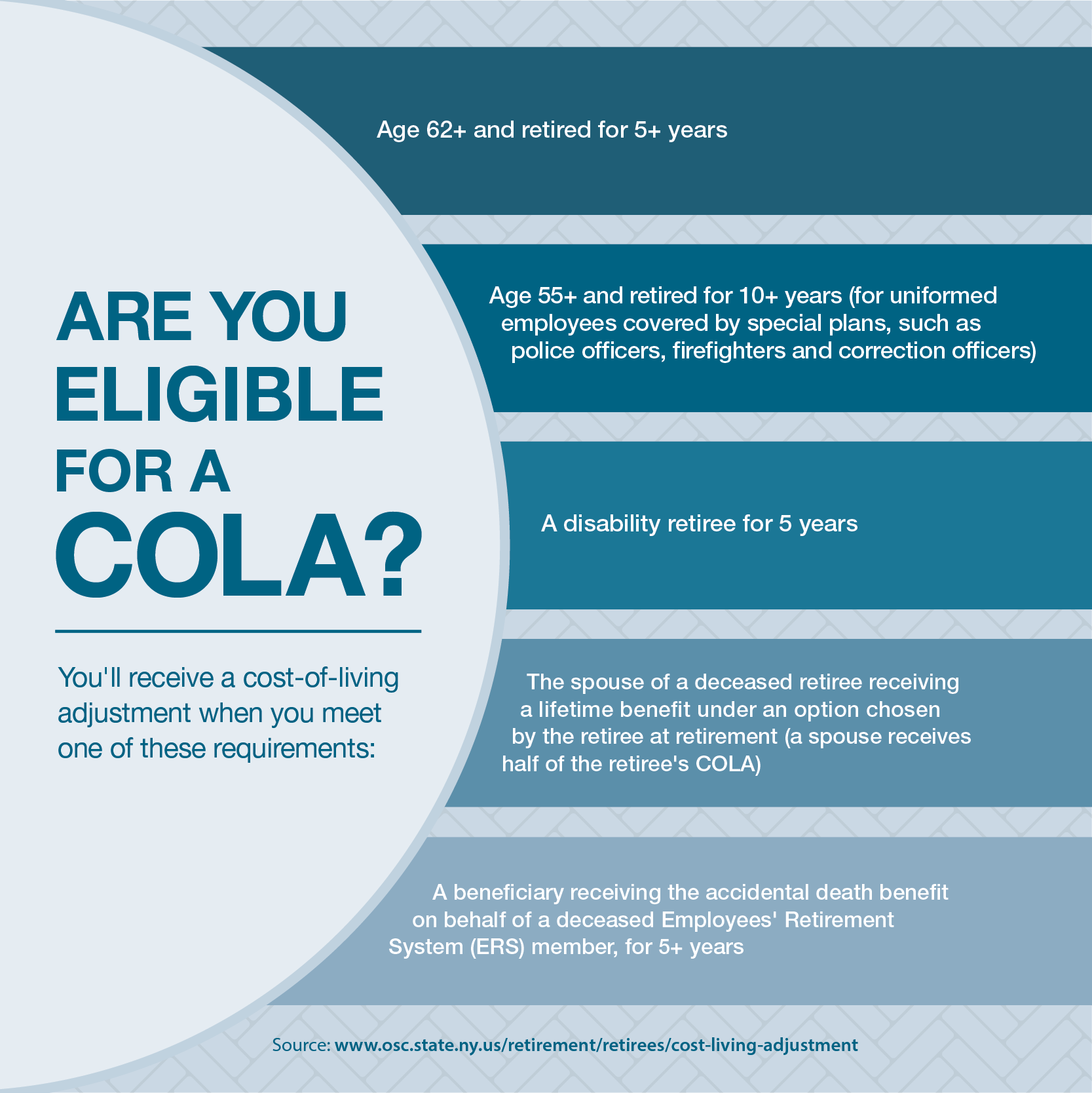

Eligible NYSLRS retirees will see a cost-of-living adjustment (COLA) in their monthly pension payments at the end of September 2023. This is a permanent annual increase to your retirement benefit that is based on the cost-of-living index and a formula set by State law. For upcoming pension payment dates, check our pension payment calendar.

How the COLA is Determined

The COLA is based on the rate of inflation, as reflected in the consumer price index published by the U.S. Bureau of Labor Statistics. The law requires that COLA payments be calculated based on 50 percent of the annual rate of inflation, as measured at the end of the State fiscal year (March 31). Once you are eligible, your annual increase will be at least 1 percent, but no more than 3 percent.

The percentage is applied to the first $18,000 of your benefit as if you had chosen the Single Life Allowance pension payment option, even if you selected a different option at retirement. Using the Single Life Allowance gives you the highest COLA amount possible, since this option pays the highest benefit. Once your COLA payments begin, you will automatically receive an increase to your monthly benefit each September.

The September 2023 COLA is 2.5 percent, for a maximum annual increase of $450.00, or $37.50 per month before taxes.

When Will You See the Increase?

Eligible retirees will see the annual 2023 COLA in their end-of-September pension payment, which will be available to those with direct deposit on September 29, 2023. If you receive a paper check, your COLA will be included in the check mailed on September 28, 2023.

Viewing Your Benefit Payment

You can view your benefit payment pay stubs, including your current COLA amount, in Retirement Online. At the end of September, if you are eligible for the increase, you’ll be able to view a breakdown of your September payment with your new COLA amount.

To view your pension payments, sign in to Retirement Online. From the top of your Account Homepage, in the ‘I want to’ section, click the “View Pension Check” link. Then select the date of the pension payment that you want to view. You’ll see a list of payments you received beginning with your January 2023 payment and going forward. If you have direct deposit, you will also receive a notification of the net change in your monthly payment amount at the end of September.

What an insult to veteran teachers and staff !!! Let’s get reasonable people on the Board.

What a truly distorted benefit retirees are receiving. Retired association, throughout the state, are sleeping the last 20 plus years……WAKE UP!!!

retired in 2015 and had to get another job almost immediately, retirement has never been enough to cover the bills and I don’t even qualify for the COLA.

Are you kidding me 37 dollars what a joke, this is the great American dream to retire after working your whole life!

PEF COLA bill

Would adjust maximum base of $18K for calculating – NY’s Permanent COLA law provides annual inflation protection equal to 50% of the annual increase in inflation calculated on a maximum base retirement benefit of $18K with a minimum increase of 1%/year and a maximum cap of 3%/year. While this law has provided important inflation protection for public sector retirees living on fixed incomes since its enactment, this protection is limited in its scope and has weakened over time. This legislation would increase the base benefit amount of $18K used to calculate the annual COLA equal to 50% of the annual rate of inflation ( Up to 1% and capped at 3% ). This annual escalator will protect the buying power of those who are already retire and more accurately reflect the higher base benefits of staff retiring now or in the future. This modest increase is critical to protecting retirees from the loss of purchasing power, especially at a time when inflation is rising.

Visit the PEF website for more information and to sign an email to your elected.

COLA-

https://actionnetwork.org/letters/permanent-cola-increase

Health Insurance-

https://actionnetwork.org/letters/health-insurance-protection

This is shame.unfair, not realistic for the current economic economy.

I am still waiting on my raise from former governor. Who dishonored our raise as retirees. previously.

I am still waiting for my due justice as a retiree

Well said Omega.

Keep it going and add your comments and ask others to join in.

https://nyretirementnews.com/cola-coming/#comments

Time to update the COLA that has not changed in 22 years or so. Unions, Alliance Public Retiree Organizations of NY, RPEA, NYSARA, NYSCOPBA, NY Teamsters, NYSOMCE, CSEA Retiree Locals, PEF Retiree Locals have all pushed their numerous COLA improvements without success for 22 years. Time for these groups to work together. We should challenge the State AFL/CIO and NYS Comptroller’s retiree committee to commit to a unified and coordinated approach. Past time to resolve. Elderly are struggling and deserve respect and dignity. This crisis has been exacerbated by high inflation, losses in all the financial markets, low interest rates on savings and loss of income by excluding pay increases and benefits to select groups such as M/Cs.

Time for these organizations to work together and reach a consensus for those they represent. Get involved and push your respective organizations.

P.S.

Members of AARP should push AARP NYS Lobbyist to join the fight. PEF has a very modest COLA improvement that will help those with the greatest need and address the above concerns. Check it out on the PEF website.

The time is now to contact your state elected. This includes emails, Snail mails, texts, phone calls and visit their offices. Simply tell them the present COLA leaves you and your loved ones to struggling. Find your NYS rep in Albany; use both links: copy and drop

https://www.nyassembly.gov/mem/search/.

Assembly Member Search | New York State Assembly

News and Information from the New York State Assembly

http://www.nyassembly.gov

https://www.nysenate.gov/find-my-senator

Comptroller DiNapoli has a fiduciary responsibility to protect the PENSION FUND for public retirees. Therefore the Comptroller must continue to devote all his efforts to this end. It is up to all of us to take action now and repeatedly to help those pensioners that are clearly struggling by pushing a bill focused on those with the greatest needs.

2.5% on the first 18000 is embarrassing to NYS Retirees….it needs to be changed. When was the 18000 cap started. It should be at least 50000. Retirees are falling way behind with this last few years inflation. What needs to be done to change this?

You need to consider that the average pension is far less than 50K. Using the first 18K is an equalizer. People who scammed 6 figure pensions get the same COLA as a retiree whose pension is more modest.

Keep it going and add your comments and ask others to join in.

https://nyretirementnews.com/cola-coming/#comments

Time to update the COLA that has not changed in 22 years or so. Unions, Alliance Public Retiree Organizations of NY, RPEA, NYSARA, NYSCOPBA, NY Teamsters, NYSOMCE, CSEA Retiree Locals, PEF Retiree Locals have all pushed their numerous COLA improvements without success for 22 years. Time for these groups to work together. We should challenge the State AFL/CIO and NYS Comptroller’s retiree committee to commit to a unified and coordinated approach. Past time to resolve. Elderly are struggling and deserve respect and dignity. This crisis has been exacerbated by high inflation, losses in all the financial markets, low interest rates on savings and loss of income by excluding pay increases and benefits to select groups such as M/Cs.

Time for these organizations to work together and reach a consensus for those they represent. Get involved and push your respective organizations.

P.S.

Members of AARP should push AARP NYS Lobbyist to join the fight. PEF has a very modest COLA improvement that will help those with the greatest need and address the above concerns. Check it out on the PEF website.

The time is now to contact your state elected. This includes emails, Snail mails, texts, phone calls and visit their offices. Simply tell them the present COLA leaves you and your loved ones to struggling. Find your NYS rep in Albany; use both links: copy and drop

https://www.nyassembly.gov/mem/search/.

Assembly Member Search | New York State Assembly

News and Information from the New York State Assembly

http://www.nyassembly.gov

https://www.nysenate.gov/find-my-senator

Comptroller DiNapoli has a fiduciary responsibility to protect the PENSION FUND for public retirees. Therefore the Comptroller must continue to devote all his efforts to this end. It is up to all of us to take action now and repeatedly to help those pensioners that are clearly struggling by pushing a bill focused on those with the greatest needs.

We couldn’t even receive the full 3% on the the first $18,000 of retirement income? I read that social security recipients are to expect a 3% COLA. Does the Federal government and NYS government look at two seperate and completely different inflationary charts? Given the fact that NYS retirees only receive a COLA on the first $18,000, the COLA, at the very least should have been 3%. All I read is how well the pension fund is doing and kudos to Mr. DiNapoli for that but come on, spread the wealth a little bit ! Remember this come Election Day my fellow NYS retirees.

They should pass a law that provides full cola on the entire pension for at least the first $60,000 per year. Not 1/2 a cola on the just the first $18,000.

DoesNYS honestly think that an increase of 37.50 Before taxes, is helping the average retiree in these days of inflated prices across the board? Social security increases are in line with inflation, COLA is not a cost of living increase. Let’s wake up and treat retirees with respect please and not insult our intelligence.

He is right! We should get a full cola on the entire pension for at least the first $60,000 per year

Joe, you are so right! NYS has PLENTY of revenue coming from all directions, yet a lousy COLA of less than 3 percent is supposed to be enough?? Not!! And don’t work too much in other public work, they’ll cap you there too!! No wonder I left NYS!

Our pensions should be better; we earned it!

How/where do I find the cola raise for 2023

Eligible retirees will see the annual 2023 COLA in their end-of-September pension payment, which will be available to those with direct deposit on September 29, 2023. If you receive a paper check, your COLA will be included in the check mailed on September 28, 2023.

You can find details about the 2023 COLA in this blog post and on our Cost-of-Living Adjustment page.

I had money taken out of my state retirement (COLA) monthly deposits so don’t understand this article about an $ increase.

For questions about your benefit payments, please call our customer service representatives at 866-805-0990, press 2, then follow the prompts. You can also message them using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.