NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring.

It’s important to name beneficiaries and review them periodically. Life circumstances change and a beneficiary you named before might not be one you would choose today. For instance, you may have a new partner or you may have children now. And NYSLRS can only pay a death benefit to the beneficiaries you’ve named.

If you are retired or planning to retire soon, read our blog post, Can You Change Your Beneficiary After You Retire?

2 Types of Beneficiaries

- Your primary beneficiary will receive your death benefit. You can list more than one primary beneficiary. If you do, they will share the benefit equally. Or, you can choose different percentages for each beneficiary, which must total 100 percent. (Example: John Doe, 50 percent; Jane Doe, 25 percent; and Mary Doe, 25 percent.)

- A contingent beneficiary will only receive a benefit if all your primary beneficiaries die before you do. If you list multiple contingent beneficiaries, they will share the benefit equally unless you choose different percentages.

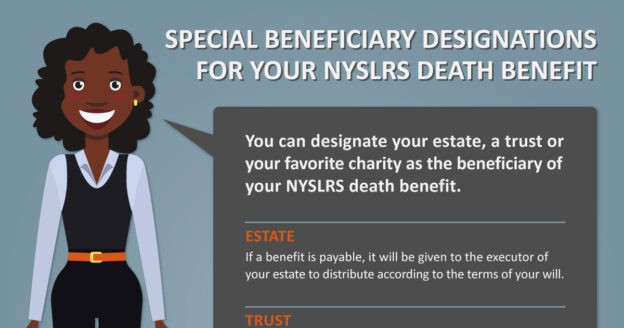

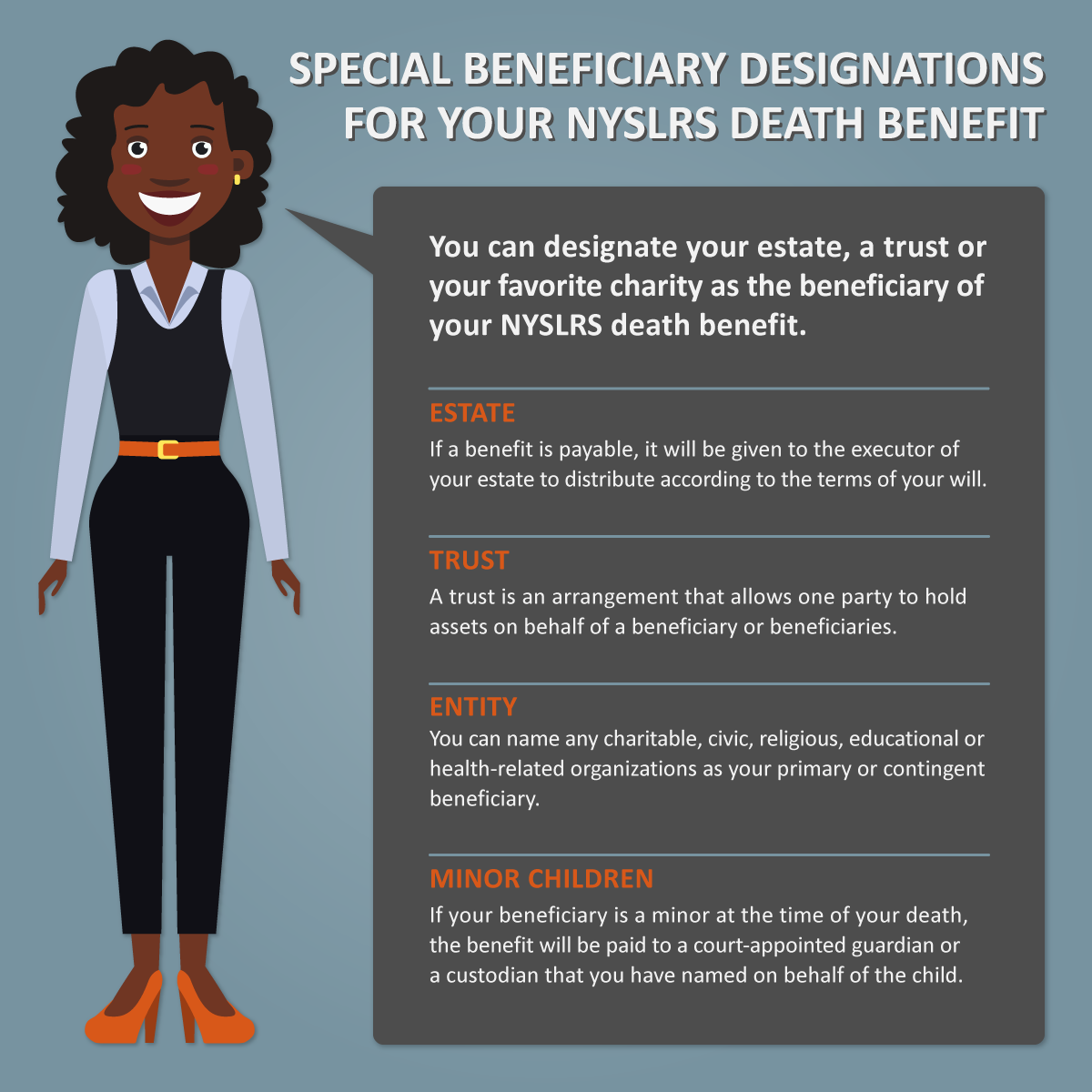

Special Beneficiary Designations

Your beneficiary doesn’t have to be a person. You can name your estate, a trust or a charity as your beneficiary.

- Estate. When you die, your estate is the money and property you owned. Your death benefit will be given to the executor of your estate to be distributed according to the terms of your will. You can name your estate as the primary or contingent beneficiary of your death benefit. If you name your estate as the primary beneficiary, do not name a contingent beneficiary.

- Trust. You can name a trust as a primary or contingent beneficiary if you have a trust agreement or provided for a trust in your will. The trust itself would be your beneficiary, not the individuals for whom you established the trust. (Speak with your attorney if you’re thinking about making your trust a beneficiary.)

- Entity. You can also name any charitable, civic, religious, educational or health-related organization as a beneficiary.

- Minor children. If your beneficiary is under the age of 18 at the time of your death, your benefit will be paid to the child’s court-appointed guardian. You may instead choose a custodian to receive the benefit on the child’s behalf under the Uniform Transfers to Minors Act (UTMA). Custodians can be designated in Retirement Online, or you can contact us for more information and the appropriate form before making this type of designation.

For more information, read our publication, Life Changes: Why Should I Designate a Beneficiary?

Keep Your Beneficiaries Up to Date with Retirement Online

You can change your beneficiaries at any time. In addition to adding or removing them to reflect your current wishes, you should review the contact information for your named beneficiaries so we can find them when needed.

The fastest way to view or update your beneficiaries is in Retirement Online.

- Sign in to Retirement Online.

- Look under My Account Summary.

- Click View and Update My Beneficiaries button.

If you mail out a change of beneficiary form that was notarized for New York State retirement life insurance and it was received, how long does it take to be approved? Also what if they pass away after the change paperwork is received but before the approval takes place?

Paper forms take longer to process. For questions about forms you’ve submitted, including timeframes for approval, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

We must reject any Designation of Beneficiary form we receive after a member dies—even if the member properly completed it prior to his or her death. As long as a valid Designation of Beneficiary form is received by our system prior to the death of the member, the form will be processed according to the designations listed regardless of processing delays within the unit.

Thank You for having staff that are attentive, informative, kind, and courteous. Today I spoke with Angelica- after waiting patiently for about 45 minutes… Angelica came on the line and was very helpful, as I am computer illiterate… Just wanted to say the information was worth the wait. Awesome customer service!!! Kudos!

We’re glad she was able to help!

You encourage us to use Retirement Online. I registered in Jan 2026, but each time I try to log I. The system is down. I called the helpline on a Tuesday, Jan 13, 2026 when I was locked out for some unknown reason, and was told there’d be a 75 minute wait. Are you kidding…”quick and easy” Hah

We’d like to help resolve your issue. Your message is important to us, and we have sent you a private message in response.

My father died in April of 2023. My brother sister and I are his beneficiaries and we all received a designation form for his final payout.

My sister and I both sent our notarized forms back in June, but our brother who has a serious substance abuse problem has yet to return his.

My sister called a few weeks ago and said that the payout wont be processed until all three forms are received. I was wondering if there is any recourse for the two of us to get ours taken care of as no one is able to locate our brother?

We would like to extend our condolences regarding your father. Please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Every time I try to sign up for online retirement portal it says unavailable. I have been trying for over a month now. I have tried all of the trouble shooting stows but still unable to sign up. I can never seem to get in contact when I call either

Your message is important to us, and we have sent you a private email in response.

I changed my Contingent Beneficiary 13 days ago and when I went back in to make sure it updated it still has the old Contingent Beneficiary name. How long should it take to update?

For help updating beneficiaries in Retirement Online, please call our customer service representatives at 866-805-0990, press 2, then follow the prompts. You can also message them using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

What happens if there is no contingent beneficiary designated and the primary beneficiary predeceases you?

If your primary beneficiary predeceases you and there is no contingent beneficiary designated, any death benefits payable would go to your estate.

My former spouse passed away on June 14, 2025. According to our divorce agreement, I had been recieving monthly benefits which appear to have been suspended pending death certificate. In addition, I am to recieved 50 % of his pension as allocated by survivor option he chose as dictated by the divorce. I do not have any control over the death certificate, as he remarried 20 years ago and this is the concern of his wife. I’ve seen a lot of information stating that paperwork will now need to be filled out, mailings will arrive etc. I rely on the funds I was recieving and the suspension of those will become a problem if they aren’t reinstated soon. Can I find out the progress of the case and when I may expect to recieve the funds currently suspended? The new benefits are less an issue, since I wasn’t already receiving them. But those that I was receiving are iimportant. Thank you.

For account-specific questions, please call our customer service representatives at 866-805-0990. Press 2, then follow the prompts. You can also message them using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Hi I am just wondering about something. My mom passed 3 1/2 years ago and after numerous attempts from myself and the worker in NYSLRS office to contact my brother who has benefit just sitting there he remains estranged. He didn’t even respond when I let him know she passed and didnt even come to her burial. What can I do?

We’re very sorry for your loss. We understand you’ve been working with our customer service representatives to review your brother’s options. Unfortunately, the NYSLRS social media team won’t be able to add anything they haven’t already covered with you.

How do I confirm that I signed up designated beneficiaries and who currently they are?

Retirement Online is the quickest and best way to manage your beneficiary information.

Once there, you can view or add beneficiaries, update their contact information, or remove them.

If you don’t have a Retirement Online account, you can message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

My minor children are the benficiaries of a death benefit from their uncle. We received forms RS 5532-R and RS 5531. Their funds must go into a guardianship bank account. I do not see any of these options on these forms. Additionally, the forms are noted as being last Revised 11/18. I cannot locate the forms online to see if there are updated versions and since I have to send original/court stamped Guardian documents, I do not want to send the wrong/old forms. Any help is gratefully appreciated as I’ve called weekly for 4 months and been on hold for 30 minutes then it hangs up, or I receive an automated recording stating the volume is too high and to call another day/time, then it disconnects. Thank you!

We’re sorry for your loss. Your message is important to us, and we have sent you a private message in response.

June 13,2025

To whom it may concern :

I am attempting to find the office that sends out the “Retiree Notes”, the semiannual newsletter published by the New York State Comptroller (NYSLRS) for retirees.

The last Retiree Notes I received was Winter 2024.

I know from other retirees that there was an issue sent out with the 2025 Pension Payment Calendar on it. I did not get this publication. (I know how to get a copy of the 2025 Calendar; this is not the issue).

I have also received the 2024 Retiree Annual Statement sent 2/15/25.

I am trying to get a copy of any Retiree Notes sent out after the Winter of 2024. And to add/update my address to the mailing list for the “Retiree Notes” that will go out in the future.

I have sent emails and made phone calls (waiting more than a half hour each time) to NYSLRS. Each time they disavow knowing anything about these newsletters. They say they only send out the Annual Statements and the 1099’s. I called the Comptroller’s office and they have no idea of what I am talking about.

I have an account on Retirement Online.

I would appreciate a response to this communique as soon as possible.

I am posting this everywhere until I get answers

We’re sorry you’ve missed recent issues of Retiree Notes. The latest issue is Winter 2024-25, which you can find on our Newsletters page.

If you changed your address recently, we may have received that change after we began mailing Retiree Notes but in time for Retiree Annual Statements.

Retirement Online is the fastest and most convenient way to check the mailing address we have on file for you—and update it if needed:

• Sign in to Retirement Online.

• Look under My Profile Information.

• Click update next to mailing address.

The next issue of Retiree Notes will be going out this summer, and we’ll be sure to mail it to the address listed in Retirement Online.

Will my family receive money to bury me?

As a NYSLRS member or retiree, you may have benefits that a beneficiary would receive upon your death. Your death benefits depend on whether you’re a member (working for a public employer) or retiree (retired and receiving a pension), your system, tier and specific retirement plan.

For information about your specific benefits, find your NYSLRS retirement plan publication. If you have questions, please call our customer service representatives at 866-805-0990, press 2, then follow the prompts.

My father retired under the Ten Year Certain Option. He passed away January 2025. I received a letter stating that a continuing benefit is payable to me. With that letter, I received a Beneficiary Application with Rollover Option form 5532-R. Is this the correct document to fill out and return to receive the continuing benefit? Should I also complete the W4 and direct deposit forms and return with the 5532-R application? Please advise. Thank you!

We’re sorry for your loss. Your message is important to us, and we have sent you a private message in response.

My name is Elizabeth Viana De Jesus daughter and beneficiary of Migdalia De Jesus. In June 2024 I received a letter where they asked me to answer it.

I answerthe letter and fill Out the document with the Notary Public.

Currently I have not received a response or benefit as beneficiarios from Migdalia De Jesús.

I change my address.

We’re sorry for your loss. Your message is important to us, and we have sent you a private message in response.

I recieved a letter in regard to a benefit left to me by my Dad. The letter is addressed in my maiden name. When I return the required information will I need to also include a copy of my marriage certificate?

We’re sorry for your loss. Your message is important to us, and we have sent you a private message in response.

I need to change the beneficiary on the retirement forms….please advise how to do so….

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. The fastest way for NYSLRS members to view or update beneficiaries is in Retirement Online.

If you are retired or planning to retire soon, read our blog post, Can You Change Your Beneficiary After You Retire?

I saw a complicated PoA in an email from you and was wondering if my lawyer PoA is good enough or do I have to have yours completed too?

The NYSLRS special durable power of attorney form meets all of New York State’s legal requirements, and it’s limited to NYSLRS pension benefit transactions.

You do not need to use the NYSLRS form to designate power of attorney. However, a power of attorney document is not effective until it has been reviewed by NYSLRS for legal soundness, and our review process is simplified for submissions using the NYSLRS form. We can complete our review faster if you use it.

For more information, read our Power of Attorney blog post.