Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement. As a NYSLRS member, your plan for income in retirement likely includes your NYSLRS pension and Social Security benefits. However, for greater financial stability and flexibility, you may want to supplement with retirement savings. For example, you might start investing in a savings plan like the New York State Deferred Compensation Plan (NYSDCP).

What is Deferred Compensation?

Deferred compensation plans are voluntary retirement savings plans like 401(k) or 403(b) plans—but designed and managed with public employees in mind. NYSDCP is the 457(b) plan created for New York State employees and employees of other participating public employers in New York.

Once you sign up for NYSDCP, you can build your own investment portfolio or invest in established investment funds. Your contributions can be automatically deducted from your paycheck, and you can contribute as little as 1 percent of your earnings.

Just like with other retirement savings plans, you have options for how you make your NYSDCP contributions. You might choose a tax-deferred account where you make contributions with pre-tax money. With this option, you won’t pay State or federal taxes on the earnings you contribute until you start making withdrawals. Your employer may also offer the option for a Roth account where you make contributions with after-tax money. With this option, you do pay taxes now, but you won’t pay taxes on the withdrawals you make in retirement. Learn more about how traditional retirement savings and Roth accounts compare.

If your employer is not an NYSDCP participating employer, check with your human resources or personnel office about other retirement savings options.

What Does Deferred Compensation Mean for Me?

Deferring income from your take-home pay may mean less money to spend in the short-term, but you’re planning ahead for your financial future.

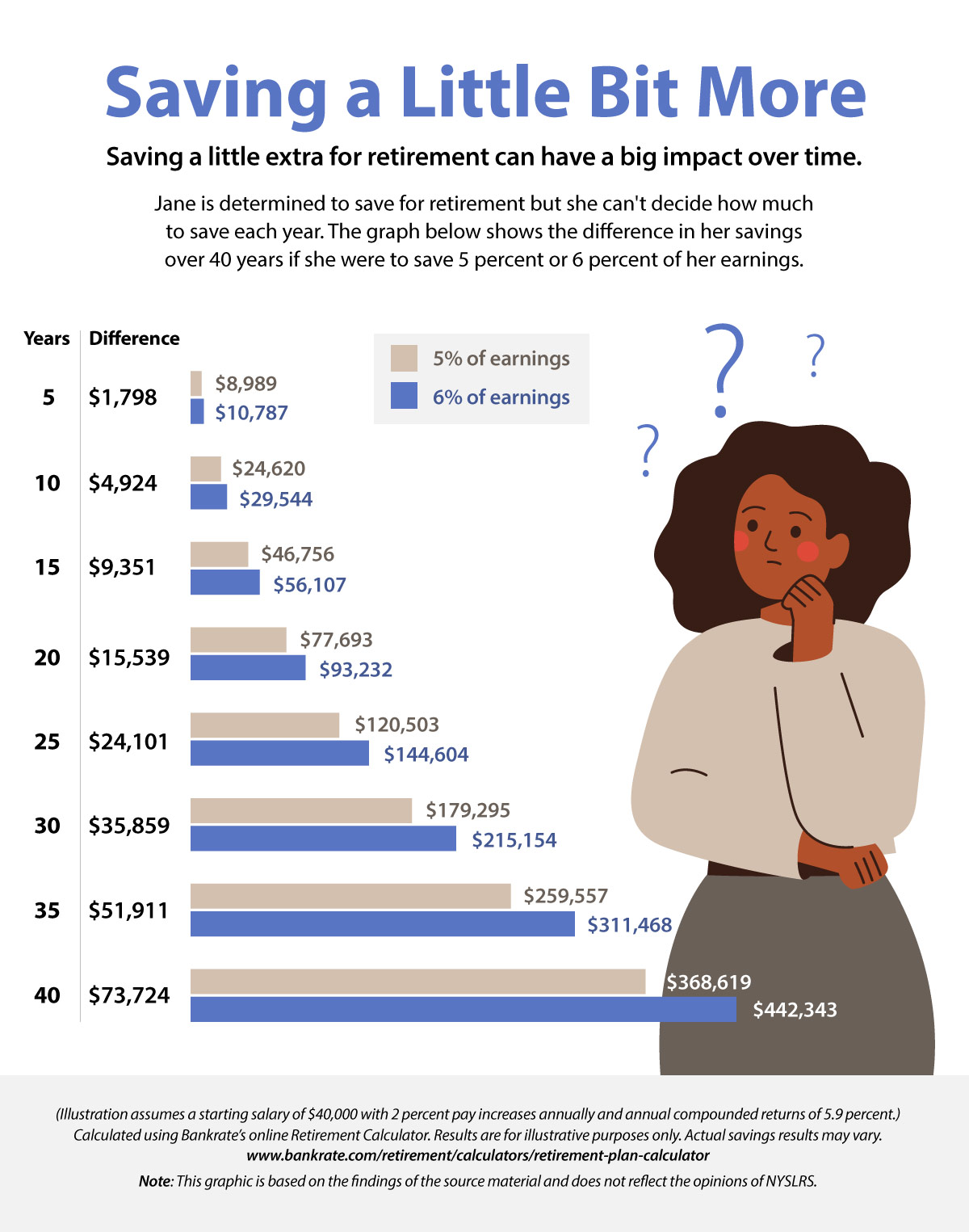

You can enroll in a deferred compensation plan anytime—whether you’re close to retirement or you just started working. Usually, the sooner you start saving, the better prepared you’ll be for retirement.