As a NYSLRS member, you are enrolled in something increasingly rare these days: a defined benefit plan. If you are vested and retire from NYSLRS, you will receive monthly pension payments for the rest of your life based on your years of service and earnings. Your NYSLRS pension can provide a significant part of your retirement income, but it’s a good idea to supplement your pension and Social Security with a retirement savings account.

Additional retirement savings can give you flexibility to travel, continue your education, pursue a hobby or start a business. It can be a resource in case of an emergency or act as a hedge against inflation.

Your Retirement Savings Goal

How much you save is a personal decision. You can estimate your pension in Retirement Online to get an idea of the income it will provide in retirement. Use a retirement savings calculator to see how much a retirement savings plan could yield over time. Test the results with different savings amounts.

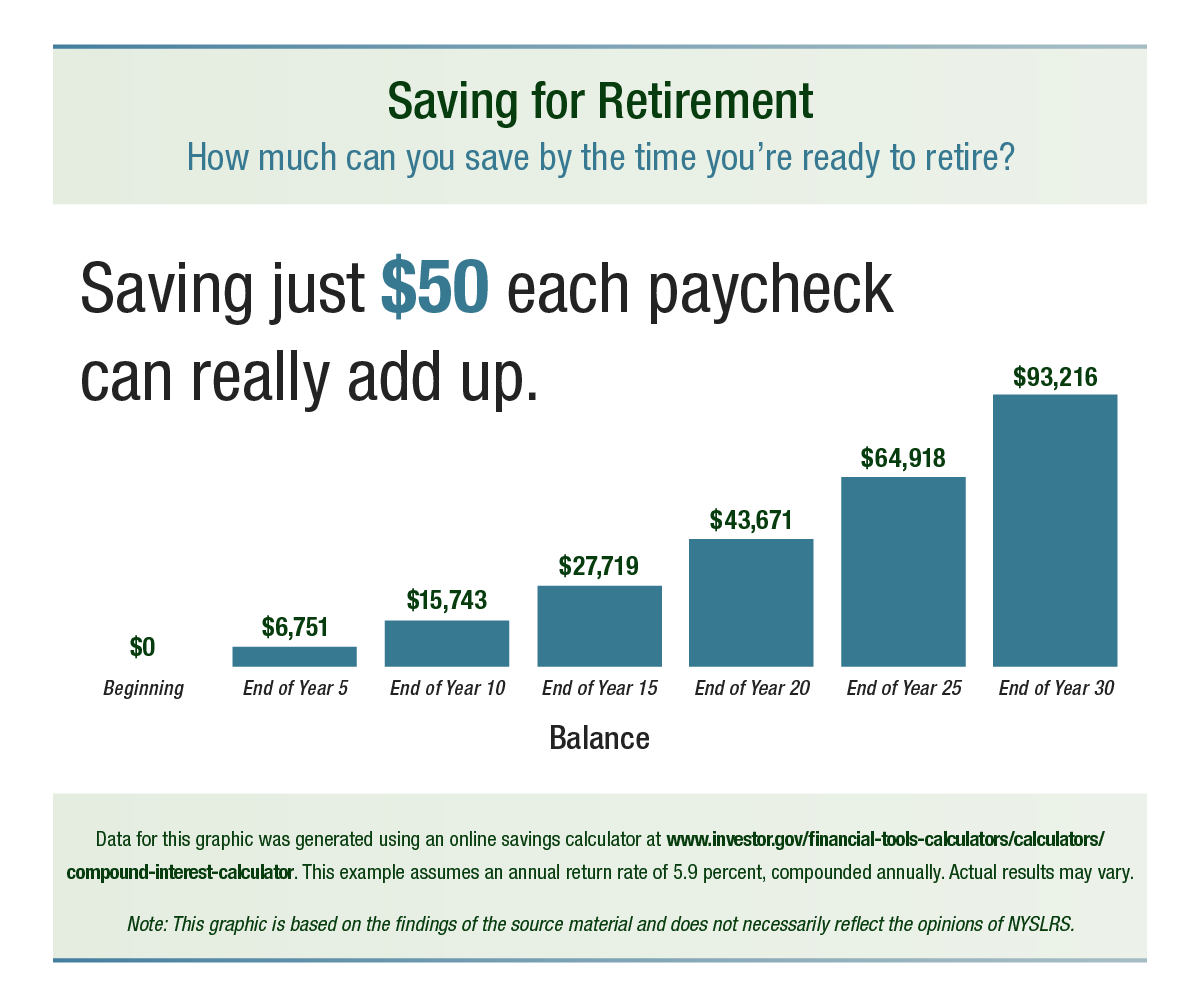

Below you can see the potential savings of someone who invests 50 dollars every two weeks for 30 years. While the stock market can be turbulent in the short term, in the long term, it returns on average about 10 percent a year as measured by the S&P 500 index.

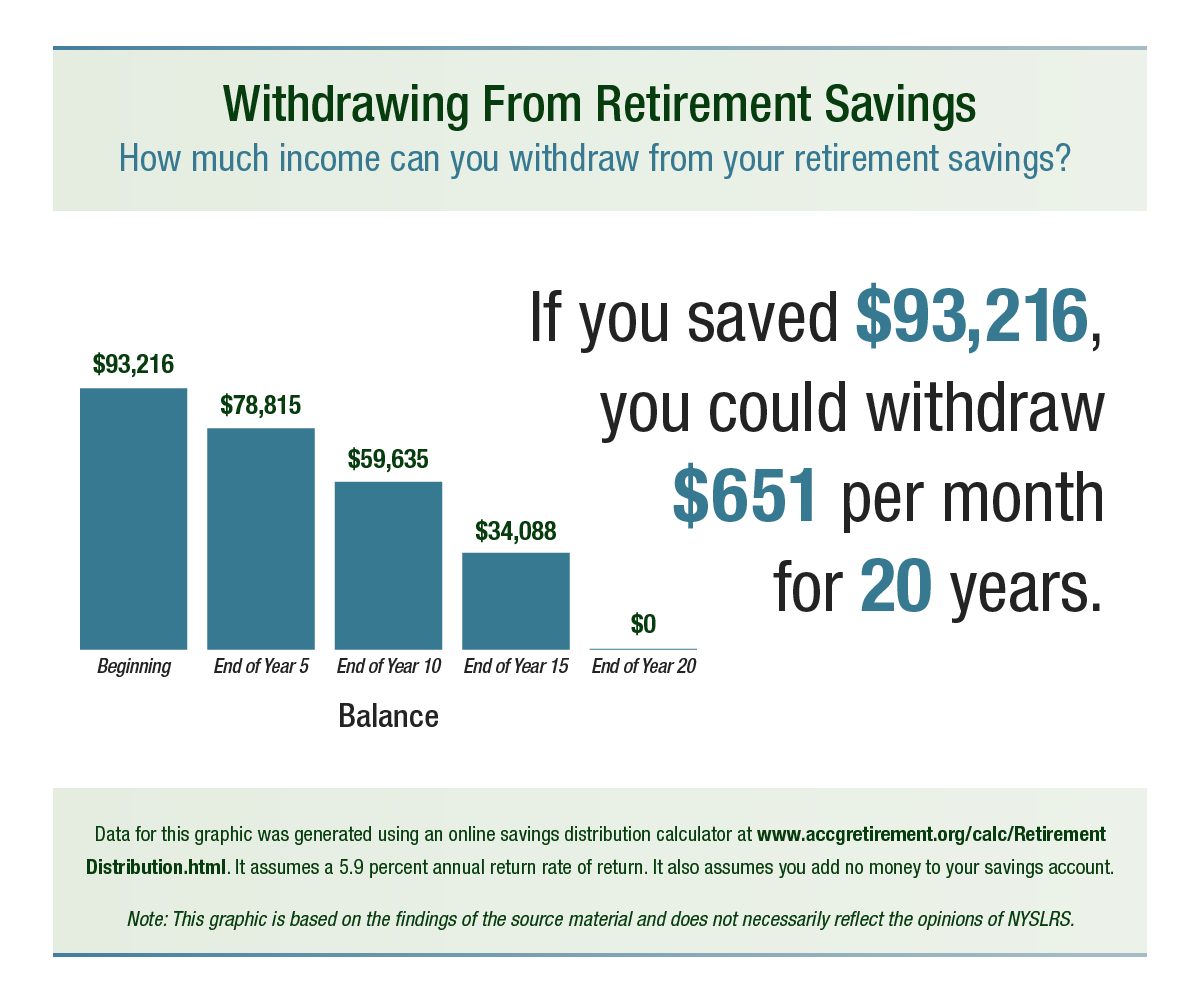

As you get closer to retirement, you should develop a plan to withdraw money from your savings. That will give you a better idea of the income you might expect from your nest egg and a sense of how long it will last.

Here is one possible withdrawal strategy, which provides retirement income for 20 years. Please note, if your retirement is far in the future, the money you withdraw may not have the same value that it would have today.

If you find you’ll need to save more to meet your goal, you can make adjustments to help ensure you’ll have enough savings in retirement.

Note: Generally, whatever your withdrawal strategy, federal law will eventually require you withdraw a certain amount each year from any tax-deferred retirement plan account. These are called required minimum distributions.

New York State Deferred Compensation Plan

One way State employees and many municipal employees can save for retirement is through the New York State Deferred Compensation Plan (NYSDCP). Once you’ve signed up, your retirement savings—which may be tax-deferred depending on the plan you choose—will be automatically deducted from your paycheck.

Check with your employer’s human resources or personnel office to see whether they participate in NYSDCP or if they offer other savings options. (NYSDCP is not affiliated with NYSLRS.)

Read More About Retirement Savings

When it comes to saving for retirement, there’s a lot to consider. You can find more information in these posts:

How can I sign up for a savings account to supplement my pension?

Is there a minimum amount?

Do I have to stay in NYS to collect?

State employees and some municipal and school employees are eligible to participate in the retirement savings program administered by the New York State Deferred Compensation Plan. You can ask your employer if you are eligible to participate.

For specific questions about retirement investments, you may want to consult a financial adviser.

Is deferred comp considered income for calculating the rate in Tier 6, that I pay into the NYSLRS?

Also, is deferrred comp considered income for calculating my highest 3 years salary, for retirement benefit amount?

What is the interest rate for borrowing from my account and are there any other fees for doing so?

Your member contributions are calculated on your full gross salary before any deductions, such as deferred compensation. For more information about what earnings qualify for the calculation of your Tier 6 contributions, read our How Your Tier 6 Contribution Rate Can Change blog post.

The specific types of earnings included in your Final Average Earnings calculation depend on your retirement plan and tier. You can find more information on our Final Average Earnings page.

The current interest rate for borrowing against your contributions is 5 percent. For Tier 3-6 members, loans are subject to a service charge (currently $45) which will be deducted from the loan at the time it is issued.

For account-specific information about any of this, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

What would you suggest for someone that never signed up first deferred comp? I’m 59, worked in my job for 25 years and would like to retire in 3 years. Should I have large amount deducted from pay now, or is it too late for me?

We recommend contacting your financial adviser to discuss retirement planning for your specific situation.

You may also want to check out the “How much should I save from each check?” section of the NYSDCP Get ready to enroll page. It has calculators to see how different contributions amounts could grow over time and how your contributions would affect your paycheck.

Hi Lisa,

I retired at 69 1/2 years old. I started my deferred comp when I was 65. My point is, it’s never too late to open an account. Along with your retirement and social security, you will have another source to supplement retirement years. Good luck

LarryB

I just retired and I’d like to know whether I can add my annual leave and my comp time to my deferred compensation. I’ve called and the answer I’ve gotten is to call payroll. I’ve called payroll and they say call deferred . It would help someone actually knows since I’ve been contributing $980 a check for about 30 years and have over $1,000,000 invested.

That’s correct. NYSLRS does not administer the New York State Deferred Compensation Plan. Please contact them at 800-422-8463 or visit their website.