April is National Financial Literacy Month, a time dedicated to helping people make informed financial decisions and manage money effectively. Financial literacy means understanding and applying various skills of personal finance management, including budgeting, planning, saving and investing.

Financial literacy is essential for effective retirement planning. When you understand your NYSLRS benefits, your other sources of retirement income and your current financial situation, you’ll be in a better position to plan for retirement.

Key Components for Financial Literacy

Assessing Finances and Budgeting

Whatever your goals, wherever you are in life, a clear-eyed assessment of your finances and effective budgeting are necessary. The 50/30/20 budget rule is one framework that can help you with both. It’s a popular way to start and stick to a budget that can work whether you’re just out of school looking at your first paycheck or retired and trying to make your savings last.

Divide Your Expenses

The idea is to divide your expenses into three categories: needs, wants and savings.

Needs are things you have to pay and can’t avoid—for example, housing costs, food, healthcare, childcare and utilities.

Wants are optional expenses. They may be fun or convenient, but they aren’t essential—for example, dining out, shopping, entertainment and vacations.

Savings & Managing Debt can help you grow your retirement assets (see more under Retirement Planning and Saving and Investing below) or build an emergency fund. This category also includes paying down debt—such as student loans or credit card balances—beyond minimum payments.

Budget Your Spending

Then, you allocate your after-tax income, with 50 percent going to needs, 30 percent to wants and 20 percent to savings. As you budget, make sure you include expenses that occur periodically, such as car and life insurance, and property and school taxes.

For more information, read The 50/30/20 Budget Rule Explained With Examples. If you decide to employ the rule, you can use a 50/30/20 budget calculator.

Managing Debt

Managing debt is an important aspect of financial literacy. Throughout your life, you’ll need to maintain good credit, borrow responsibly and repay your debt diligently.

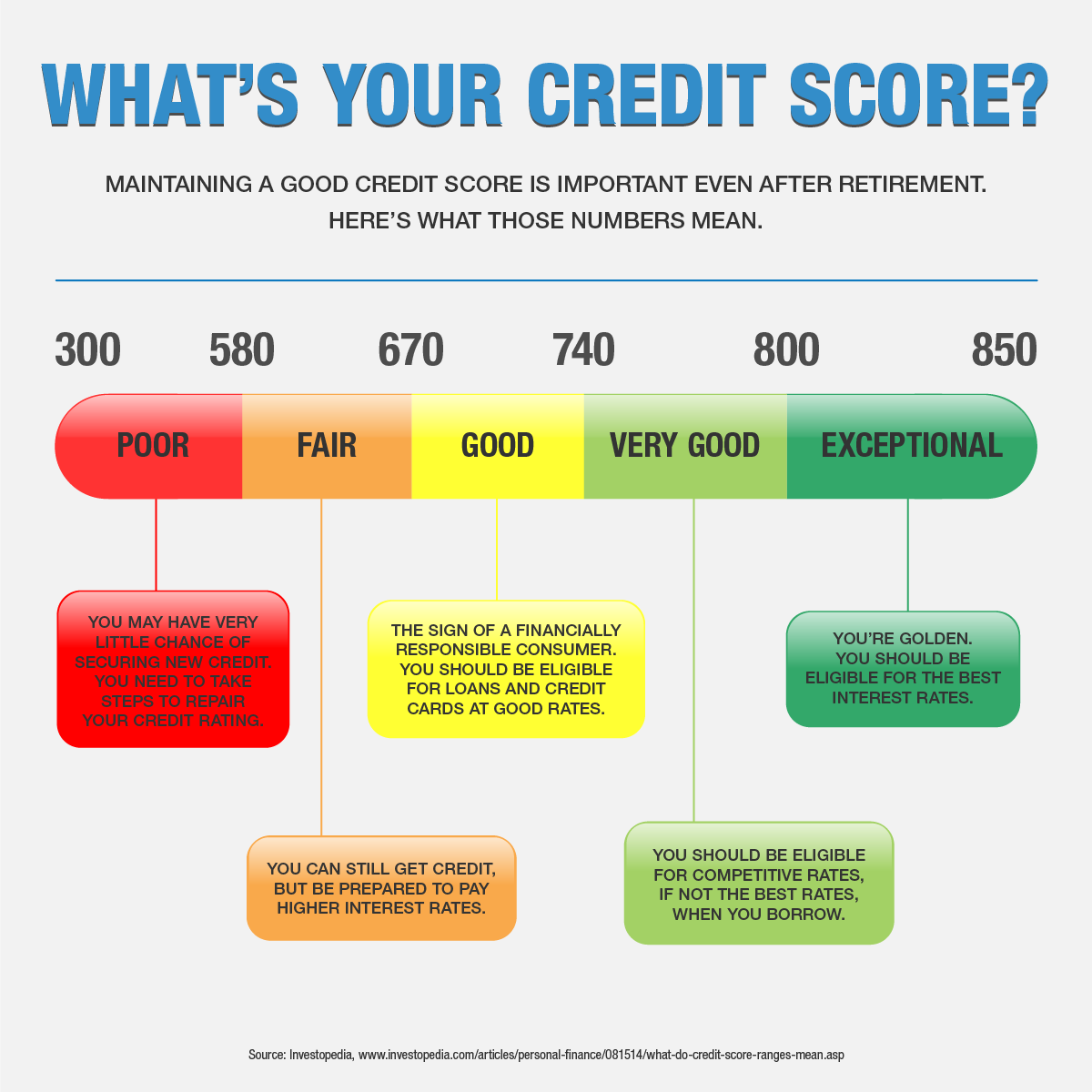

Credit Scores

Your credit score is a three-digit number used by lenders to judge how likely you are to pay back money you’re loaned. It’s based on your past payment history and other interactions with lenders. These three digits affect you more than you might realize.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance. They are also used to determine the interest rate and credit limit you receive.”

Even if you’re doing everything right, misinformation in the files of credit rating companies can hurt your credit. So, check your credits scores regularly. You can do it online at AnnualCreditReport, the free-credit-report site authorized by the federal government and maintained by the three major credit reporting agencies.

Responsible Borrowing

The best way to maintain your credit score is to borrow responsibly and manage debt effectively. That means:

- Pay your bills on time; pay more than the minimum payments if you can.

- Avoid using all or most of your available credit.

- Keep longstanding credit lines open (like a credit card you’ve had for many years).

- Avoid accumulating excessive debt—especially opening several lines of credit in a short amount of time.

Pay Down Your Debt

It’s a good idea to take inventory of any debt you owe and have a plan for paying it off.

If you have more than one credit card balance, many financial advisors recommend paying as much as you can on the card with the highest interest rate, while still making at least the minimum payments on your lower-interest cards.

Debt is not necessarily bad, but if you’re planning to retire soon, paying it down can give you more flexibility to enjoy the type of retirement you want.

Retirement Planning

Retirement is a big step. In many ways, confidence in a comfortable retirement is the reason saving and building financial literacy throughout our lives is so important.

Understand Your Sources of Income in Retirement

As a NYSLRS member, you are enrolled in something increasingly rare these days: a defined benefit plan. If you are vested and retire from NYSLRS, you will receive a monthly pension payment for the rest of your life based on your years of service and earnings.

However, your pension is just one of three main sources of income in retirement. Think of retirement security as a three-legged stool. Each leg is a source of income, and you need all three for a stable retirement.

- Your NYSLRS pension is a guaranteed lifetime benefit. Find your retirement plan publication for comprehensive information about your pension and the other benefits you are entitled to receive.

Most NYSLRS members can estimate their pension benefit in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit. - Your Social Security benefit is another source of income to help support you in retirement. At Social Security’s full retirement age, your benefit can replace a significant portion of your pre-retirement income, depending on how much you earned while working. You can estimate your benefit on the Social Security Administration website.

- In addition to your NYSLRS and Social Security benefits, retirement savings can be an important financial asset when you retire. Savings can give you flexibility to travel, continue your education, pursue a hobby or start a business. It can be a resource in case of an emergency, act as a hedge against inflation and boost your retirement confidence.

Determine How Much You’ll Need in Retirement

Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement.

Use our Monthly Income & Expenses Worksheets to help you track your current spending habits and project your future needs. Remember to account for non-monthly expenses, such as car insurance, property taxes and school taxes.

Saving and Investing

If you aren’t saving already, right now is the best time to start. If your retirement is a long way off, that means you’ll have more time for your savings to grow. But even if you’re close to retirement, it is never too late to start saving.

If you’re already building your retirement savings, think about giving your savings a boost. Even a small increase could make a big difference over time.

For New York State employees and many other NYSLRS members, there’s an easy way to get started. If you work for a participating employer, you can join the New York State Deferred Compensation Plan. If you don’t work for New York State, check with your employer to see if you are eligible. If you are not eligible, your employer may be able to direct you to an alternative retirement savings program.