Financial security doesn’t just happen; it takes planning and time. You know you can count on your NYSLRS pension in retirement. But, if you want to improve your chances of a financially secure retirement, your plan should include retirement savings. It’s important to start saving early so your money has time to grow.

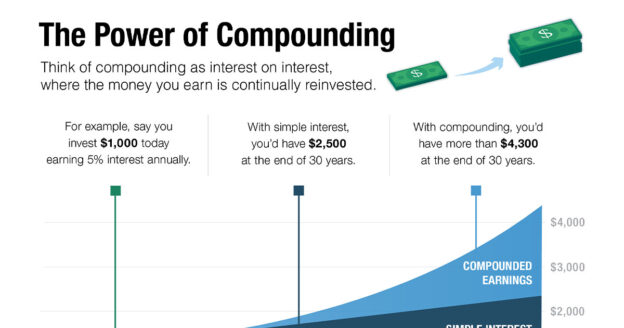

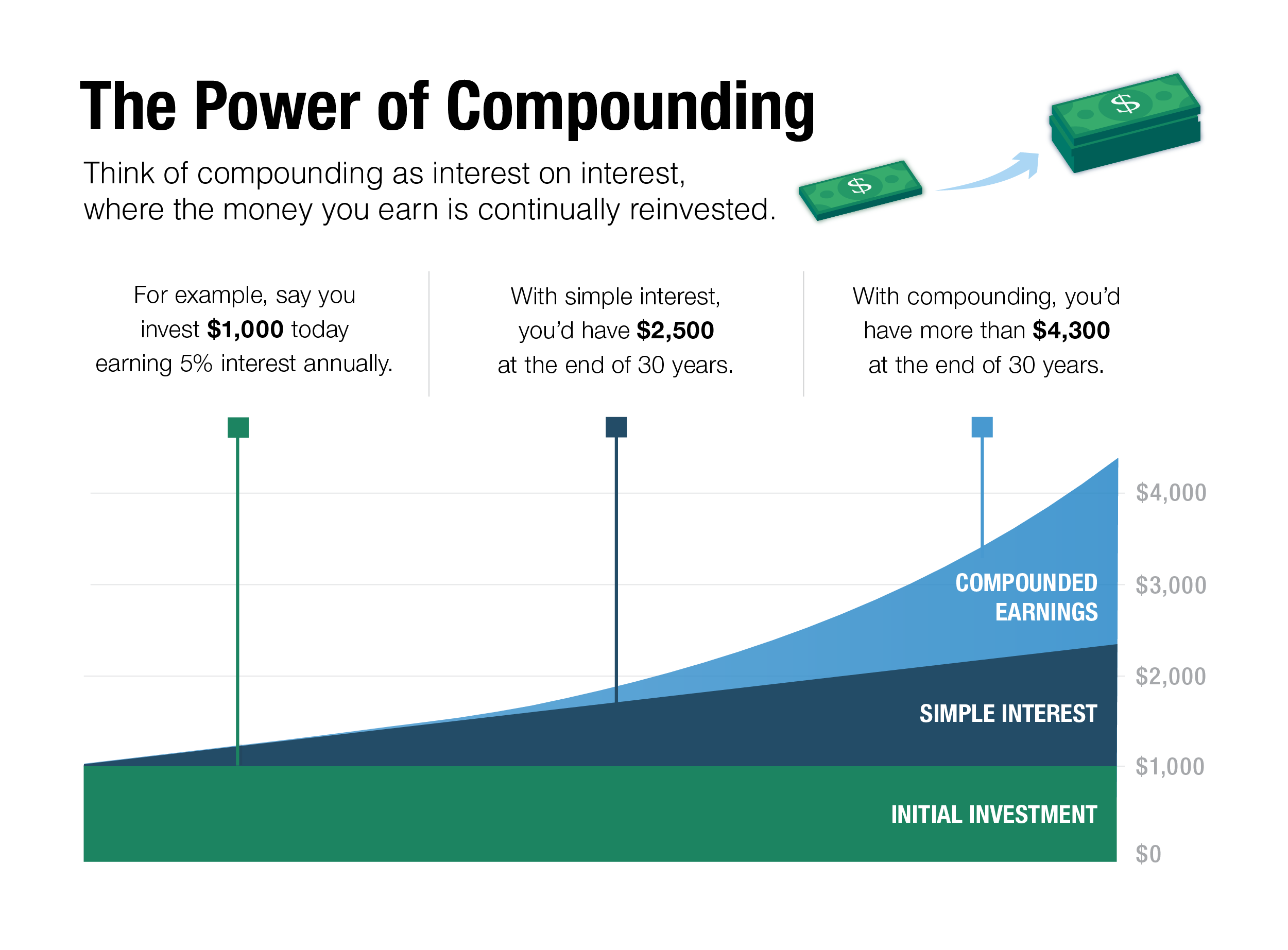

When you invest your savings in an individual retirement account (IRA) or a 401(k)-style retirement savings plan, you earn a return on your investment, and those returns are compounded. That means your money increases in value by earning returns on both the original amount and your accumulated profits. This is different than earning simple interest. Let’s see how they both work.

How Simple Interest Works

In banking, simple interest is a certain percentage you are paid on the money you put into your account. With simple interest, the amount of interest you earn is based on the original (or principal) amount of the deposit.

Let’s say you open a certificate of deposit (CD), which pays 5 percent simple interest if you agree to keep your money in the CD for a year. If you deposit $1,000 in January, you’ll have $1,050 at the end of the year. That’s $50 more than you started with, so you might decide to keep your money there for another year. With simple interest, the interest you earn the second year and every year after would still be based on the principal amount of $1,000—no compounding.

How Compounding Works

With compounding, your initial investment is reinvested along with your earnings. If you earn the same 5 percent, with compounding, it’s applied to the full balance of your account. So, you would still have that $1,050 at the end of the first year, but by the end of the second year you’d have $1,102.50 in your account instead of $1,100.

In this example, that’s just a difference of $2.50, but, over time, compounding can mean a difference of hundreds or thousands of dollars.

If you’re already building retirement savings, think about giving your savings a boost. If you haven’t started saving yet, right now is the best time to start. The New York State Deferred Compensation Plan (NYSDCP) is available to New York State employees and some municipal employees. Once you’ve signed up, your retirement savings—which may be tax-deferred depending on the plan you choose—will be automatically deducted from your paycheck. Remember, the sooner you start saving, the more time your money has to grow.

Your NYSLRS pension is a good reason to be optimistic about your finances in retirement. Once you retire, your pension will provide monthly payments for the rest of your life. But there is more to a financially secure retirement than having a pension.

Think of retirement security as a three-legged stool. Each leg is a source of income to help support you when your working days are done. It’s important to understand all your potential sources of income to effectively plan for the future and boost your retirement confidence.

Leg 1: Your NYSLRS Pension

NYSLRS pensions are defined benefit plans, also known as traditional pension plans. When you retire, you will receive a monthly pension payment for the rest of your life. Your pension will be calculated using a preset formula based on your earnings and years of service—it will not be based on the individual contributions you paid into the system. Unlike workers who rely on 401(k)-style retirement plans, you won’t have to worry about this income running out.

Most members can estimate their pension in Retirement Online. But, if you’re a long way from retirement, it may be better to think in terms of earnings replacement. Financial advisers estimate you’ll need to replace 70 to 80 percent of your income to retire with confidence. Your pension can help get you there. For example, if you retire with 30 years of service, your NYSLRS pension could replace more than half of your earnings. (Pension benefits depend on your tier and retirement plan. Find your retirement plan publication for comprehensive information about your retirement benefits and how your pension will be calculated.)

Leg 3: Retirement Savings Can Boost Your Confidence

A lifetime pension and Social Security income will be substantial financial assets, but it’s still important to save for retirement. Healthy retirement savings will give you more flexibility to do the things you want to do in retirement. It can also help in case of an emergency and act as a hedge against inflation.

Your personal savings is the factor you have the most control over. You decide when to start, how much to save and how to invest your money. The key is to start saving early so your money has time to grow, even if you can only afford to save a small amount in the beginning.

Eligible employees might consider saving with the New York State Deferred Compensation Plan (NYSDCP). Money gets deducted from your paycheck, so you won’t even have to think about it. NYSDCP is not affiliated with NYSLRS, but New York State employees and some municipal employees can participate. If you’re a municipal employee, ask your employer whether you’re eligible for NYSDCP or another retirement savings plan.

Striving to maintain a good credit score is just as important in retirement as it is during your working years. You may be retired, but financial necessities continue. You may need to get a car loan or refinance a mortgage, and good credit ensures you can borrow money at a decent interest rate. In fact, bad credit could prevent you from renting an apartment, or you may be required to pay higher insurance premiums. Fortunately, it seems maintaining good credit is just a matter of continuing what you’ve already been doing.

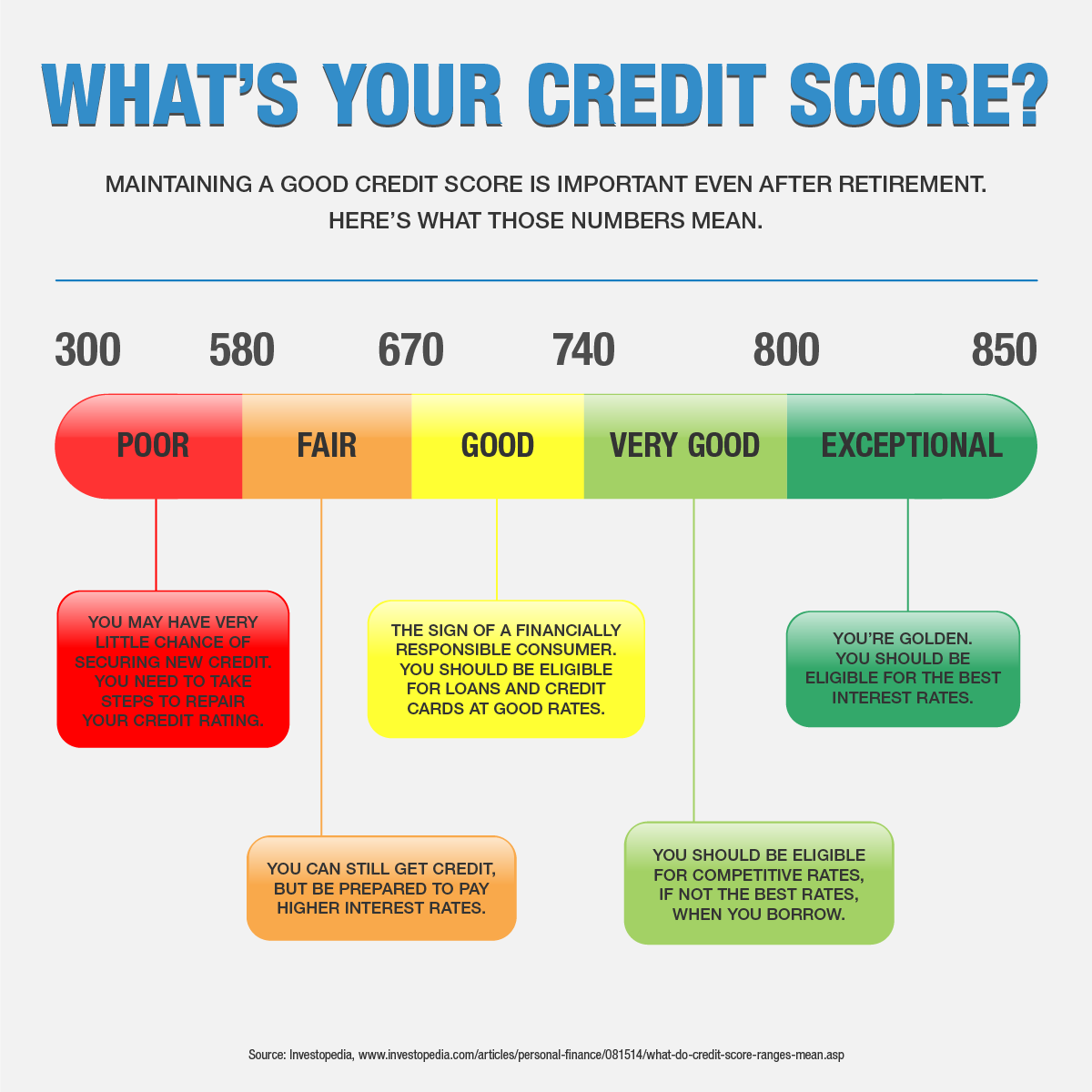

What is a Credit Score?

Your credit score is a three-digit number used by lenders to judge how likely you are to pay back money you’re loaned. It’s based on your past payment history and other interactions with lenders. These three digits affect you more than you might realize.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance. They are also used to determine the interest rate and credit limit you receive.”

How to Maintain a Good Credit Score

The best way to maintain your credit score is to borrow responsibly and manage debt effectively. That means:

Pay your bills on time. Pay more than the minimum payments if you can. Your payment history accounts for about a third of your credit score.

Avoid using all or most of your available credit. The ratio of debt to available credit is another factor in your credit. If all your credit cards have balances near the limit, your credit score will suffer.

Keep longstanding credit lines open. These accounts show your long history of being responsible with credit and help to boost your score.

Don’t accumulate excessive debt. You especially want to avoid opening several lines of credit in a short amount of time.

Things like age and salary are not part of the credit score equation, so being retired does not hurt your score. However, lenders do take income into account when you apply for a loan, so you may find it harder to borrow after retirement, even if you have good credit.

Check Your Credit Reports Annually

Even if you’re doing everything right, misinformation in the files of credit rating companies could hurt your credit. So, check your credits scores regularly.

Under federal law, the three nationwide credit reporting companies are required to provide a free credit report once every 12 months. But you must request it. You can request your credit report online at AnnualCreditReport.com or by calling 877-322-8228. AnnualCreditReport.com is a website maintained by the three major credit reporting agencies—Equifax, Experian and TransUnion. It is the only free credit report site authorized by the federal government. Beware of impostor sites.

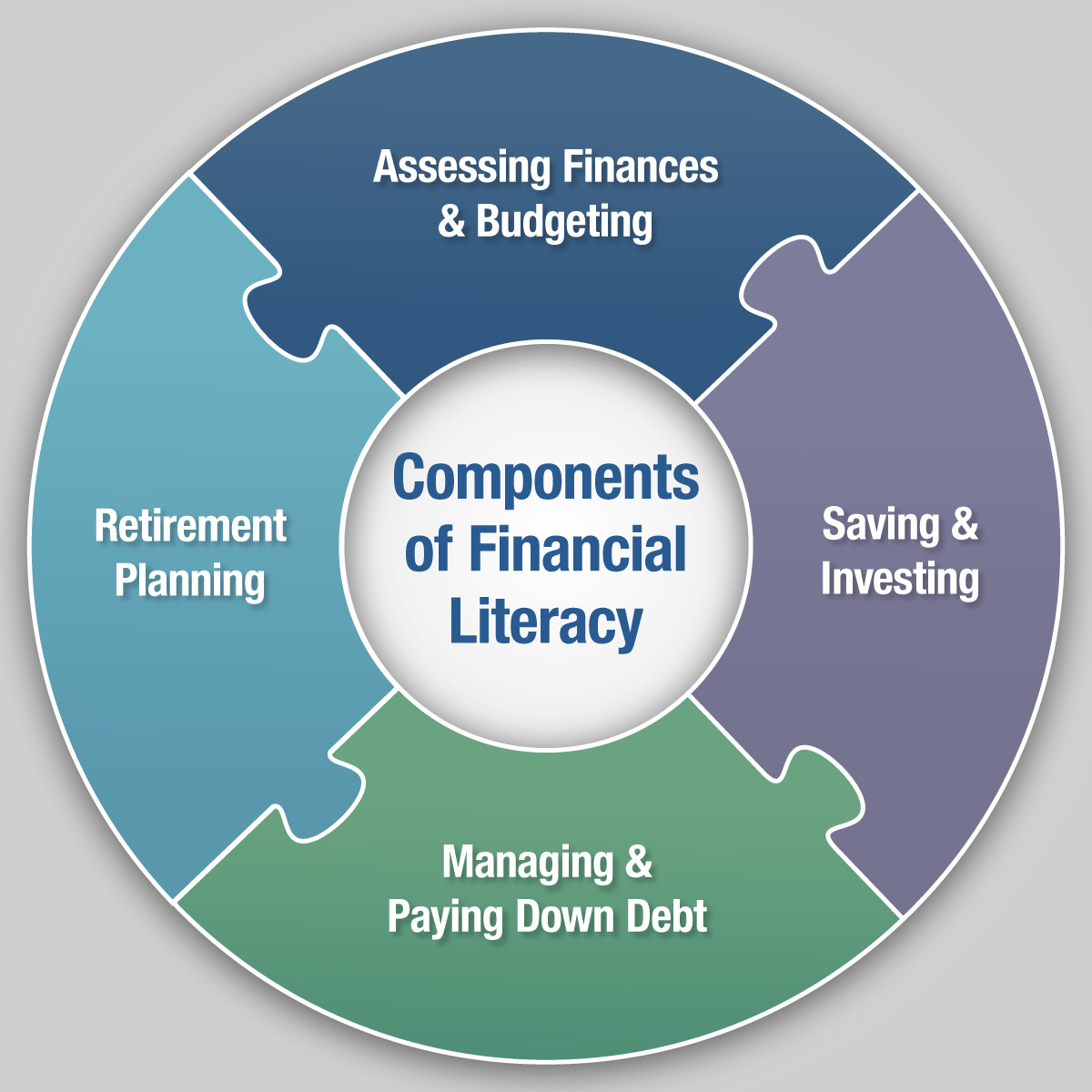

April is National Financial Literacy Month, a time dedicated to helping people make informed financial decisions and manage money effectively. Financial literacy means understanding and applying various skills of personal finance management, including budgeting, planning, saving and investing.

Financial literacy is essential for effective retirement planning. When you understand your NYSLRS benefits, your other sources of retirement income and your current financial situation, you’ll be in a better position to plan for retirement.

Key Components for Financial Literacy

Assessing Finances and Budgeting

Whatever your goals, wherever you are in life, a clear-eyed assessment of your finances and effective budgeting are necessary. The 50/30/20 budget rule is one framework that can help you with both. It’s a popular way to start and stick to a budget that can work whether you’re just out of school looking at your first paycheck or retired and trying to make your savings last.

Divide Your Expenses

The idea is to divide your expenses into three categories: needs, wants and savings.

Needs are things you have to pay and can’t avoid—for example, housing costs, food, healthcare, childcare and utilities.

Wants are optional expenses. They may be fun or convenient, but they aren’t essential—for example, dining out, shopping, entertainment and vacations.

Savings& Managing Debt can help you grow your retirement assets (see more under Retirement Planning and Saving and Investing below) or build an emergency fund. This category also includes paying down debt—such as student loans or credit card balances—beyond minimum payments.

Budget Your Spending

Then, you allocate your after-tax income, with 50 percent going to needs, 30 percent to wants and 20 percent to savings. As you budget, make sure you include expenses that occur periodically, such as car and life insurance, and property and school taxes.

Managing debt is an important aspect of financial literacy. Throughout your life, you’ll need to maintain good credit, borrow responsibly and repay your debt diligently.

Credit Scores

Your credit score is a three-digit number used by lenders to judge how likely you are to pay back money you’re loaned. It’s based on your past payment history and other interactions with lenders. These three digits affect you more than you might realize.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance. They are also used to determine the interest rate and credit limit you receive.”

Even if you’re doing everything right, misinformation in the files of credit rating companies can hurt your credit. So, check your credits scores regularly. You can do it online at AnnualCreditReport, the free-credit-report site authorized by the federal government and maintained by the three major credit reporting agencies.

Responsible Borrowing

The best way to maintain your credit score is to borrow responsibly and manage debt effectively. That means:

Pay your bills on time; pay more than the minimum payments if you can.

Avoid using all or most of your available credit.

Keep longstanding credit lines open (like a credit card you’ve had for many years).

Avoid accumulating excessive debt—especially opening several lines of credit in a short amount of time.

If you have more than one credit card balance, many financial advisors recommend paying as much as you can on the card with the highest interest rate, while still making at least the minimum payments on your lower-interest cards.

Debt is not necessarily bad, but if you’re planning to retire soon, paying it down can give you more flexibility to enjoy the type of retirement you want.

Retirement Planning

Retirement is a big step. In many ways, confidence in a comfortable retirement is the reason saving and building financial literacy throughout our lives is so important.

Understand Your Sources of Income in Retirement

As a NYSLRS member, you are enrolled in something increasingly rare these days: a defined benefit plan. If you are vested and retire from NYSLRS, you will receive a monthly pension payment for the rest of your life based on your years of service and earnings.

However, your pension is just one of three main sources of income in retirement. Think of retirement security as a three-legged stool. Each leg is a source of income, and you need all three for a stable retirement.

Your NYSLRS pension is a guaranteed lifetime benefit. Find your retirement plan publication for comprehensive information about your pension and the other benefits you are entitled to receive. Most NYSLRS members can estimate their pension benefit in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit.

Your Social Security benefit is another source of income to help support you in retirement. At Social Security’s full retirement age, your benefit can replace a significant portion of your pre-retirement income, depending on how much you earned while working. You can estimate your benefit on the Social Security Administration website.

In addition to your NYSLRS and Social Security benefits, retirement savings can be an important financial asset when you retire. Savings can give you flexibility to travel, continue your education, pursue a hobby or start a business. It can be a resource in case of an emergency, act as a hedge against inflation and boost your retirement confidence.

Determine How Much You’ll Need in Retirement

Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement.

Use our Monthly Income & Expenses Worksheets to help you track your current spending habits and project your future needs. Remember to account for non-monthly expenses, such as car insurance, property taxes and school taxes.

If you’re already building your retirement savings, think about giving your savings a boost. Even a small increase could make a big difference over time.

For New York State employees and many other NYSLRS members, there’s an easy way to get started. If you work for a participating employer, you can join the New York State Deferred Compensation Plan. If you don’t work for New York State, check with your employer to see if you are eligible. If you are not eligible, your employer may be able to direct you to an alternative retirement savings program.

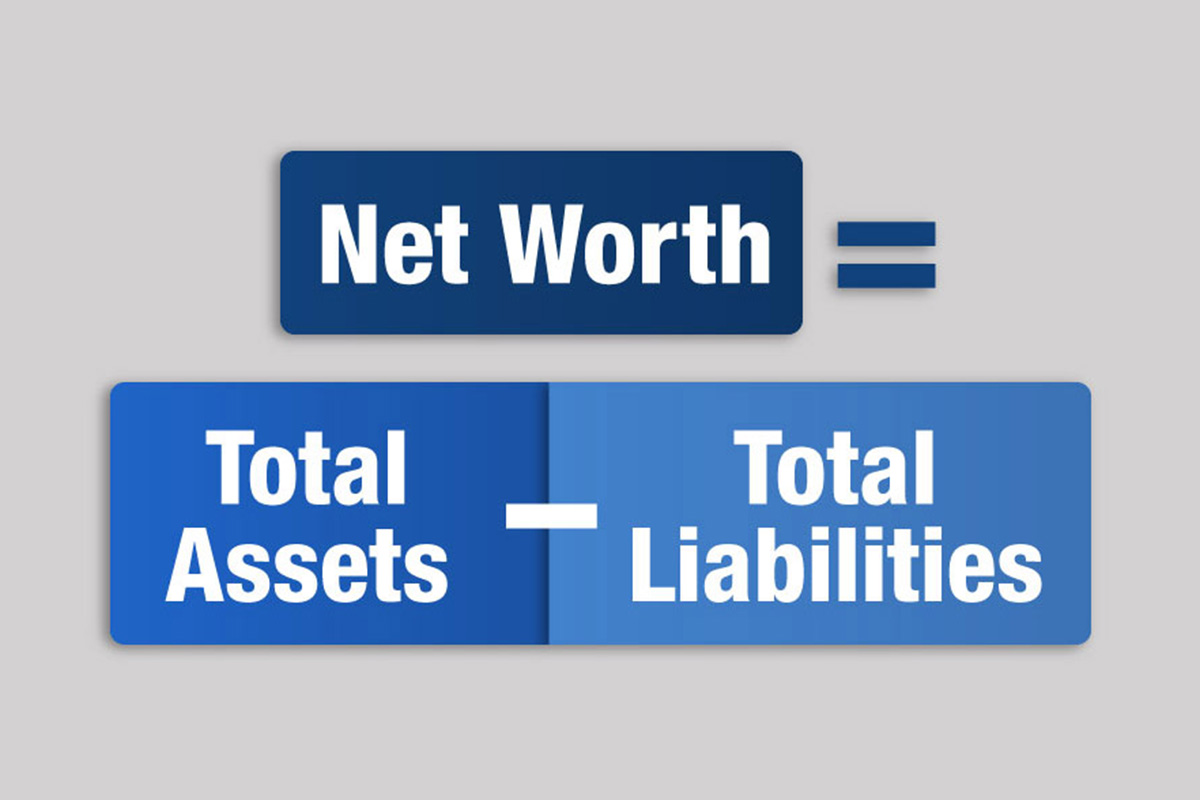

When it comes to understanding your finances, a good place to start is by calculating your net worth.

Net worth is the total value of everything you own, minus the money you owe. It is a measure of your wealth and an indicator of your financial condition. It can also provide you with valuable insight as you start developing your financial plan for retirement.

How to Calculate Net Worth

The formula for calculating your net worth is simple:

Assets and Liabilities

Your assets are items of value that you own, including:

Your house

Other real estate (a vacation home, rental property)

Money in checking and saving accounts

Retirement savings, such as a 401(k) or Deferred Compensation account

Stocks, bonds and other investments

Your car and other vehicles

Jewelry, furniture and household items

Your liabilities are your debts. Your mortgage, credit card debts and loan balances factor into your total liabilities.

If you owe more than the value of your total assets, you have a negative net worth. A negative net worth may not necessarily mean you’re in financial trouble — it just means that at the moment you have more debts than assets.

If you’re just beginning your career and still have student loans, you may find yourself in negative territory. But your net worth is likely to increase over time as you pay down debts and save money.

Knowing Your Net Worth Can Help You Get a Handle on Your Finances

Your net worth shows your current financial status. When you know where you stand, you’ll be better prepared to make decisions about spending, saving and investing, which will help you achieve your short- and long-term financial goals. Your net worth can show you where you’re doing well and where there’s room for improvement. For example, it may indicate a need to curb your spending or reduce your credit card debt.

Your net worth is likely to change over time, so it’s a good idea to calculate it periodically. With this updated financial information, you’ll be able to track trends and make adjustments if necessary.

NYSLRS pensions are

NYSLRS pensions are