Your NYSLRS pension will provide you with a monthly benefit for the rest of your life. When you apply for retirement, you’ll have the option to choose the maximum amount payable or a reduced benefit in exchange for possibly continuing payments to a beneficiary upon your death. In this post, we’ll explore the Joint Allowance and Pop-Up/Joint Allowance pension payment options which provide a lifetime benefit for a single beneficiary.

Joint Allowance Pension Payment Options

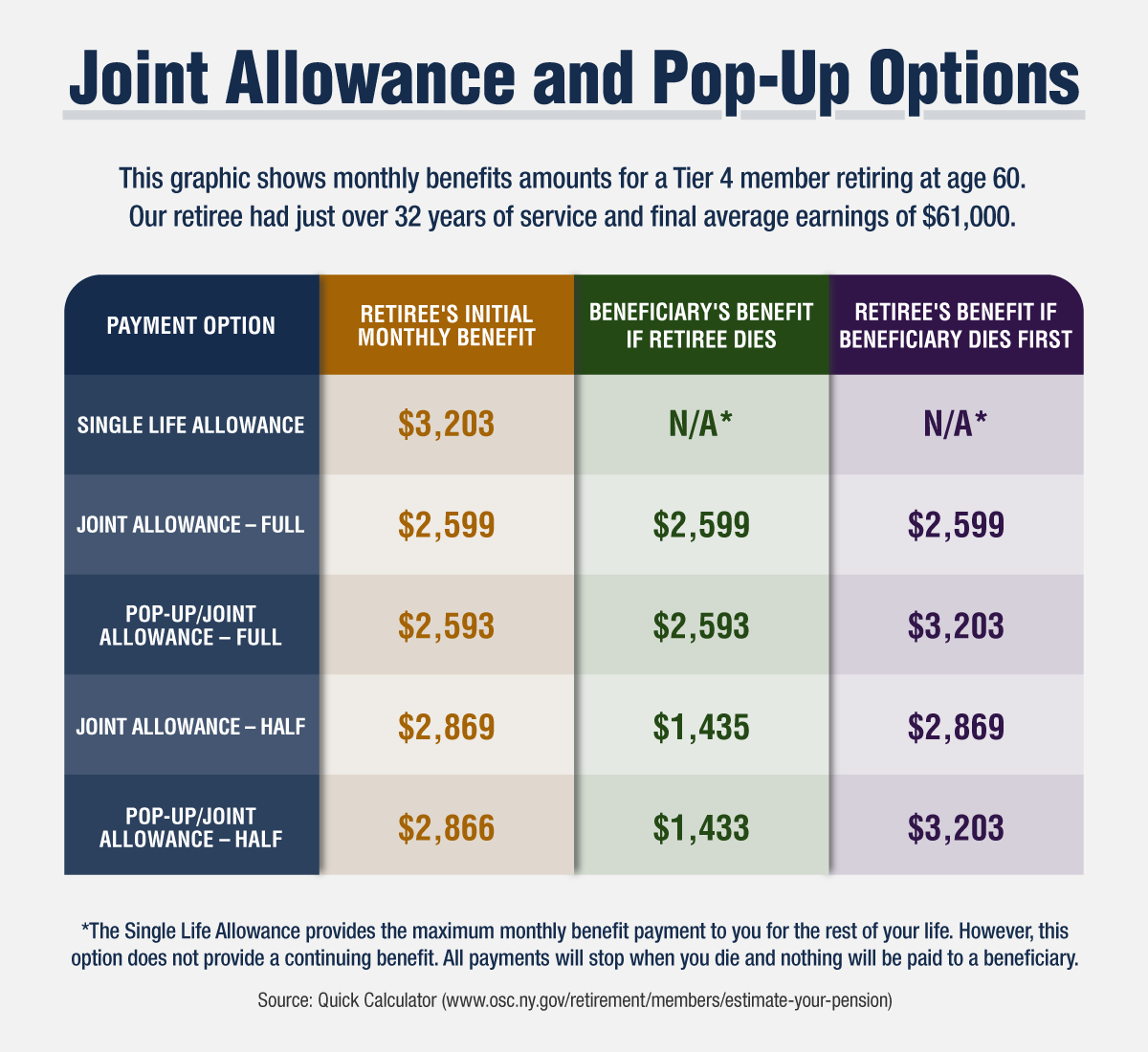

In exchange for a permanent reduction in your monthly pension payment, the Joint Allowance options provide a lifetime benefit to a beneficiary after you die.

You can select either:

- Full: Your beneficiary will receive the same monthly pension payment as you were receiving for life.

- Half: Your beneficiary will receive half of the monthly pension payment you were receiving for life.

- Partial: Your beneficiary will receive either 75, 50, or 25 percent of the monthly pension payment you were receiving for life.

You can only choose one beneficiary under a Joint Allowance option, and you cannot change your beneficiary after you retire—regardless of the circumstances. If your beneficiary dies before you, all payments will stop when you die.

Pension payment amounts are based on the birth dates of both you and your beneficiary. Because life expectancy is a factor, the reduction to your pension payment amount will be more if you select a child or grandchild than a spouse of a similar age as you.

If you designate your spouse as your beneficiary, they would be eligible to receive 50% of your cost-of-living adjustment.

Pop-Up/Joint Allowance Pension Payment Options

The Pop-Up/Joint Allowance options have all the same terms of the Joint Allowance options with added security—if your beneficiary dies before you, your monthly pension payment will “pop up” or increase to the amount you would have been receiving had you chosen the Single Life Allowance option at retirement. (Note: This only affects future payments. You would not be entitled to retroactive payments.) Therefore, the Pop-up/Joint Allowance options reduce your monthly pension payment a little more than a comparable Joint Allowance option.

Other Pension Payment Options

The Single Life Allowance provides the maximum monthly pension payment to you for the rest of your life. However, this option does not provide a continuing benefit. All payments will stop when you die, and nothing will be paid to a beneficiary.

Some pension payment options provide a limited benefit for multiple beneficiaries.

Things to Consider

When choosing your pension payment option, you may want to consider both your spouse’s and your:

- Financial needs (for instance, whether you have a mortgage, unpaid loans or other monthly payments).

- Other sources of retirement income (for example, Social Security or savings).

- Options for continuing benefits (for example, whether your retirement plan includes a death benefit or if you have life insurance).

- Age and health at retirement.

You only have 30 days after the last day of your retirement month to change your option. After that date, you cannot change your option for any reason.

Estimate Your Pension in Retirement Online

Most members can use Retirement Online to create a pension estimate based on the most up-to-date salary and service information we have on file. You can enter different retirement dates, beneficiaries and pension payment options to see how they affect your potential benefit.

- Sign in to Retirement Online.

- Look under My Account Summary section.

- Click Estimate my Pension Benefit button.

When you’re done, print your pension estimate or save it for future reference.

If I receive a monthly benefit from a deceased retiree’s pension as a beneficiary, what taxes are withheld (if any), or what is the combined withholding rate suggested for me to set aside? Does the monthly benefit check need to be claimed on my IRS or NYS income taxes?

NYSLRS is required to withhold federal income tax from your pension benefit at the Internal Revenue Service’s (IRS) designated default withholding status of “single with no adjustments” unless you inform us otherwise. The amount withheld is based on the information you provide to us on a W-4P Form (Withholding Certificate for Pension or Annuity Payments). You can change your withholding at any time. To check your current withholding, sign in to Retirement Online and view your pension pay stub.

The IRS Tax Withholding Estimator may help you estimate the federal income tax you want withheld from your pension. When using the tool, be sure to have your most recent tax return, pension pay stubs and other income information available—your results will be based on the information you enter.

For more information—including how to update your withholding—visit our Taxes and Your Pension page.

I received an email from NYSLRS that I will receive 20+ years of service credit.

However, my pension estimate falls short of this.

I have sent multiple letters to NYSLRS, without any direct response.

Your message is important to us, and we have sent you a private message in response.

i’m 63y/o as of 12/2025. my most recent statement says I reached full retirement at age 62 as of 3/2025. Do I have to start taking my pension as of age 62, or like Medicare will my monthly pension amount be greater if I delay taking my pension at an older age (if so to what age max can I delay to?), or will it always be the same $ amount as of age 62 as of 3/2025 even if I delay taking it? If the pension amount is fixed as of full retirement age of 62y/o in 3/2025, is there anyway to recover the monthly pension payments I have thus far missed, and how do I start receiving my monthly pension check?

If you’ve reached full retirement age, you can apply for and receive your NYSLRS pension without an early age reduction. Your pension will be based on your retirement system, tier, retirement plan, service credit and final average earnings. Find your retirement plan publication for comprehensive information about your benefits and how your pension will be calculated.

We recommend you use Retirement Online to create a pension estimate based on the most up-to-date salary and service information we have on file. You can enter different retirement dates, beneficiaries and pension payment options to see how they affect your potential benefit.

We also recommend you contact our customer service representatives for account-specific questions. You can call them at 866-805-0990 (press 2, then follow the prompts). You can also message them using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Your date of retirement is up to you, but you must apply at least 15 days but no more than 90 days before your chosen retirement date. For most members, you will receive your first pension payment at the end of the month following the month you retire. Visit our website for information on how to apply to retire online.

Hello,

If my grandmother who had legal guardianship over me passed away and had chosen pop up/ joint allowance full, would anything change if i end up getting married or have kids? Will i lose that allowance?

If you were designated as the beneficiary of your grandmother’s NYSLRS pension, upon her death, you would receive the same Pop-Up/Joint Allowance—Full percentage of your grandmother’s monthly pension payment for the rest of your life. It would not be affected by your marriage or by having children. The payments would end upon your death.

I am trying to find out when my account will be updated at how many years i have in the system. it shows 11/30/2025. when is the next update? thank you

For account-specific questions, please call our customer service representatives at 866-805-0990 (press 2, then follow the prompts). You can also message them using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

I left employment with NY State. How do I transfer my current pension amount to an investment account?

If you left public employment with less than ten years of service credit, you can end your NYSLRS membership and request a refund of your contributions. Withdrawing your contributions terminates your NYSLRS membership and you would become ineligible for any Retirement System benefits.

To withdraw your membership:

You can choose to have all or part of your withdrawal payment made as a direct rollover to an Individual Retirement Account (IRA), or to another eligible retirement plan that accepts rollovers.

Visit our website for more information about withdrawing your membership.

If you have account-specific questions, you can message our customer service representatives using our secure contact form. Filling out the secure form allows NYSLRS to safely contact you about your personal account information.

Approximately how much in percentage is my pension amount taxed?

Most NYSLRS pensions are subject to federal income tax. The amount withheld is based on the information you provide to us on a W-4P Form (Withholding Certificate for Pension or Annuity Payments).

NYSLRS pensions are not subject to New York State or local income tax.

I just received my first retirement check. I am confused as to what the Monthly Service Annuity NT is that was subtracted from my earnings. What is this fee?

For questions about your pension deductions, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Where on the website does it state the date my pension gets sent? I can’t find it anywhere. Thank you for your help.

If you recently retired, for most members, you will receive your first pension payment at the end of the month following the month you retire. For example, if you retired any time in the month of August, your first payment will be at the end of September (payment for August and September). If you have not submitted proof of your date of birth, your payments may be delayed.

For retirees who have direct deposit, your pension payment is deposited directly into your bank account on the last business day of each month. Our Pension Payment Calendar lists the schedule of direct deposit dates by month.

Hello, I would like to know how the monthly estimation of the pension is affected by changes in yearly earnings in the Retirement fund portfolio due to changes in the return of the allocation in Stocks? Once retired, do the monthly payments are affected by changes in the market?

NYSLRS benefits are defined benefit plans, which are calculated based on a preset formula and provide a specified payment amount at retirement. At retirement, you will receive a lifetime pension based on your years of service and earnings rather than market performance. For more information, visit our What is a Defined Benefit Plan? webpage.

I was divorced on my fifth year of joining the retirement system and my ex will get half of the amount from 5 years and prior.

My ex tells me that she does not want the benefit but would rather I pay for a burial fund for her instead.

How can we go about making these changes?

For help with your divorce questions, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

If I were to retire in the middle of October 2025, when would I get my first retirement check?

NYSLRS pension benefits are paid monthly.

For most members, you will receive your first pension payment at the end of the month following the month you retire. For example, if you retire any time in the month of October, your first payment will be at the end of November (payment for October and November).

My mom passed away recently. I received one letter stating that as beneficiary, my mom retired a single life allowance option 0 with a lump sum payment. I completed forms and paperwork and certified mailed it to NYS with receipt date. However I received another letter dated the same as the first but I received it yesterday stating my mom retired as joint allowance full option 2 with joint allowance (100/75/50/25%) underneath that statement. The letter also stated to disregard previous letters however the previous letter was dated on same date. I called and someone called me back after putting me on hold for 15 min and call hung up. Then i called again and waited this time for 85 min and then the call went blank. I need to know which letter is correct. I can’t seem to get in touch with anyone. I have also emailed as well, but no reponse

Please accept our condolences. We’d like to help resolve your issue. Your message is important to us, and we have sent you a private email in response.

What happens if your spouse divorces you after retirement and you have selected pop up?

If you designated your spouse as the beneficiary of your Pop-Up Joint Allowance at retirement, you cannot change your pension payment option or beneficiary after a divorce. If your beneficiary dies before you, you can send a photocopy of their death certificate, and we will increase your benefit to the Single Life Allowance amount.

If you have account-specific questions, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

I AM PLANNING ON GETTING MY RETIREMENT THE END OF SEPT OF THIS YEAR 2025. 2 PART QUESTION I LIVE OUT OF STATE AND PLAN ON MAILING MY PAPER WORK AND DOCUMENTS . SEPT 26 TH IS MY 55TH BIRTHDAY WHICH IS MY ELIGILBILITY TO COLLECT. FROM OUT OF STATE WHEN SHOULD I MAIL IN MY PAPERWORK AND DOCUMENTS .?? 2ND QUESTION IS HAVING EVERYTHING MAILED IN A TIMELY MATTER . AND MY BIRHDAY IS SEPT 26. ABOUT HOW LONG OR ROUGHLY WHEN WOULD FIRST CHECK COME?

You must submit your application 15-90 days before your retirement date. If you mail your application to us, we recommend you use certified mail, return receipt requested.

Most members will receive their first pension payment at the end of the month following their retirement month. So, if you retire in September, you’d likely receive your first check at the end of October.

You may want to consider applying for retirement in Retirement Online. When you file online, there are no forms to mail in and nothing to have notarized.

You may also want to schedule a pre-retirement consultation to speak with one of our representatives, who can review your benefits and answer any questions you may have.

What exactly is the pop-up/joint allowance?

I have seen it on my annual statements, but never knew I needed to opt-in.

My retirement is a few years away, so is this something I need to do STAT?

Thanks!

A Pop-Up/Joint Allowance is one of the pension payment options NYSLRS retirees can choose when they retire. In exchange for a permanent reduction in your monthly pension payment, Joint Allowance options provide a lifetime benefit to a beneficiary after you die.

Pop-Up/Joint Allowance options work the same as regular Joint Allowance options. However, if your beneficiary dies before you, your monthly pension payment will “pop up” or increase to the amount you would have been receiving had you chosen the maximum monthly pension benefit (Single Life Allowance option) at retirement.

The projections in your Member Annual Statement are based on your account information as of March 31, the end of the State fiscal year.

Most NYSLRS members can create their own pension estimates based on the latest account information we have on file using Retirement Online. You can enter different retirement dates, payment options and beneficiaries to see how those choices would affect your benefit.

To get started:

If you have questions about your benefit projections, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

I sent an email over 10 days ago and I have been trying to call NYSLRS for 2 weeks. I can’t get ahold of anyone. My question is:

My spouse and Pension Payment Option/Survivors Beneficiary died 11/26/2013. I recently noticed that she is still on the account and that my payments are still based on POP-UP JOINT ALLOWANCE-FULL. I am sure that I notified NYSLRS when she passed. I am wondering why my payments are not SINGLE LIFE ALLOWANCE. I know that there is a difference in payments that I have not been receiving. Will I receive the difference in payments retroactively when this correction is made?

We’re sorry for the trouble. Your message is important to us, and we have sent you a private message in response.

I have the same problem! My spouse died a few months ago. I reported his death and received acknowledgement and requested my pension pop up. I still see the half popup on my file and my pension hasn’t increased!

We would like to extend our condolences on the loss of your spouse. Your message is important to us, and we have sent you an email in response.

How can I choose the Pop-Up/Joint Allowance-Full option now and what re the percentage choices?

My spouse is my primary beneficiary, but I still have several years until retirement. If I die before I retire will my spouse get a one-time payout? Or will she get a monthly pension payment for the rest of her life?

Most members who die while they’re still working will leave their beneficiaries what’s called an ordinary death benefit—a one-time, lump sum payment that’s usually equal to one year of your earnings per year of service, up to a maximum of three years. If you’ve named your spouse as your primary beneficiary, this is the benefit she would currently receive, not a pension benefit.

You choose your pension payment option at retirement. If you select a Pop-Up/Joint Allowance option, you could again name your spouse as your beneficiary, and she would receive a lifetime benefit when you die. The most common percentages are 100, 75, 50, or 25 percent.

You can find more information about the ordinary death benefit and other death benefits in our Know Your Benefits: Death Benefits blog post.

You may want to Estimate Your Pension in Retirement Online to get an idea of the benefit your spouse might receive under different payment options once you retire. These estimates are based on the most up-to-date account information we have on file for you.

For account-specific questions, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Both my husband and I work at the same high school. He will be drawing on his pension June 1st. His pension benefit is hirer than mine as his salary was higher. My question is, if he does a pop-up/joint allowance for me do I still get both his pension and mine as I am his pension beneficiary?

I understand that in Social Security I would take the higher benefit for spouse? Since we both earned pensions, and as long as my husband’s has me as his pop up/joint allowance, I would get both his and mine upon his death? Is this correct? This is a big question for us in regards to getting life insurance.

If you and your husband will each collect your own pension from NYSLRS, it will not affect the amount you would receive as the beneficiary of his NYSLRS pension.

We recommend you use Retirement Online to create a custom pension estimate for you and your husband. Most Tier 2, 3, 4, 5 and 6 members can use Retirement Online to create NYSLRS pension estimates based on the salary and service information we have on file for you.

• Sign in to Retirement Online.

• From Account Homepage, click Estimate my Pension Benefit button.

You can enter different retirement dates and beneficiaries to see how they affect your potential benefit. For additional information about pension estimates, please message our customer service representatives using our secure contact form. Filling out the secure form allows them to safely contact you about your personal account information.

Hello, I have a question about my retirement. If my spouse passes away before I do, what happens to her portion of the pension? Does it go back to me? or can I arrange it to go to my children?

Some pension payment options let a retiree choose a reduced benefit in exchange for continuing payments to a beneficiary upon their death. So, it depends on what payment option your spouse selected when she retired and who she named as beneficiary.

Once NYSLRS is informed of a retiree’s death and we receive the death certificate, we will send named beneficiaries or their certified representatives (guardians, powers of attorney, executors) information about death benefits and, if applicable, information about any continuing pension benefits and death benefits that may be payable. We will also send named beneficiaries the appropriate forms to complete.