When you’re ready, Retirement Online makes applying for retirement fast and convenient. There are no forms to mail in and nothing to have notarized. When you apply online, you’ll be able to:

- See estimates of your pension for the payment options available to you.

- Upload documents while applying or after submitting your application.

- Submit changes to your application quickly and easily if needed.

For more information, visit our Preparing and Applying for Retirement page.

Use Retirement Online to Apply for Retirement

To get started:

- Sign in to Retirement Online.

- Look under My Account Summary.

- Click Apply for Retirement button.

Choose Your Retirement Date

Your date of retirement is up to you! Keep in mind:

- You must apply at least 15 days but no more than 90 days before your chosen retirement date.

- You must stop working and be off your employer’s payroll on your retirement date (your last day on payroll must be no later than the day before your retirement date).

- Your date of retirement can be a weekend or holiday (for example, if your last day of work is a Friday your retirement date can be Saturday).

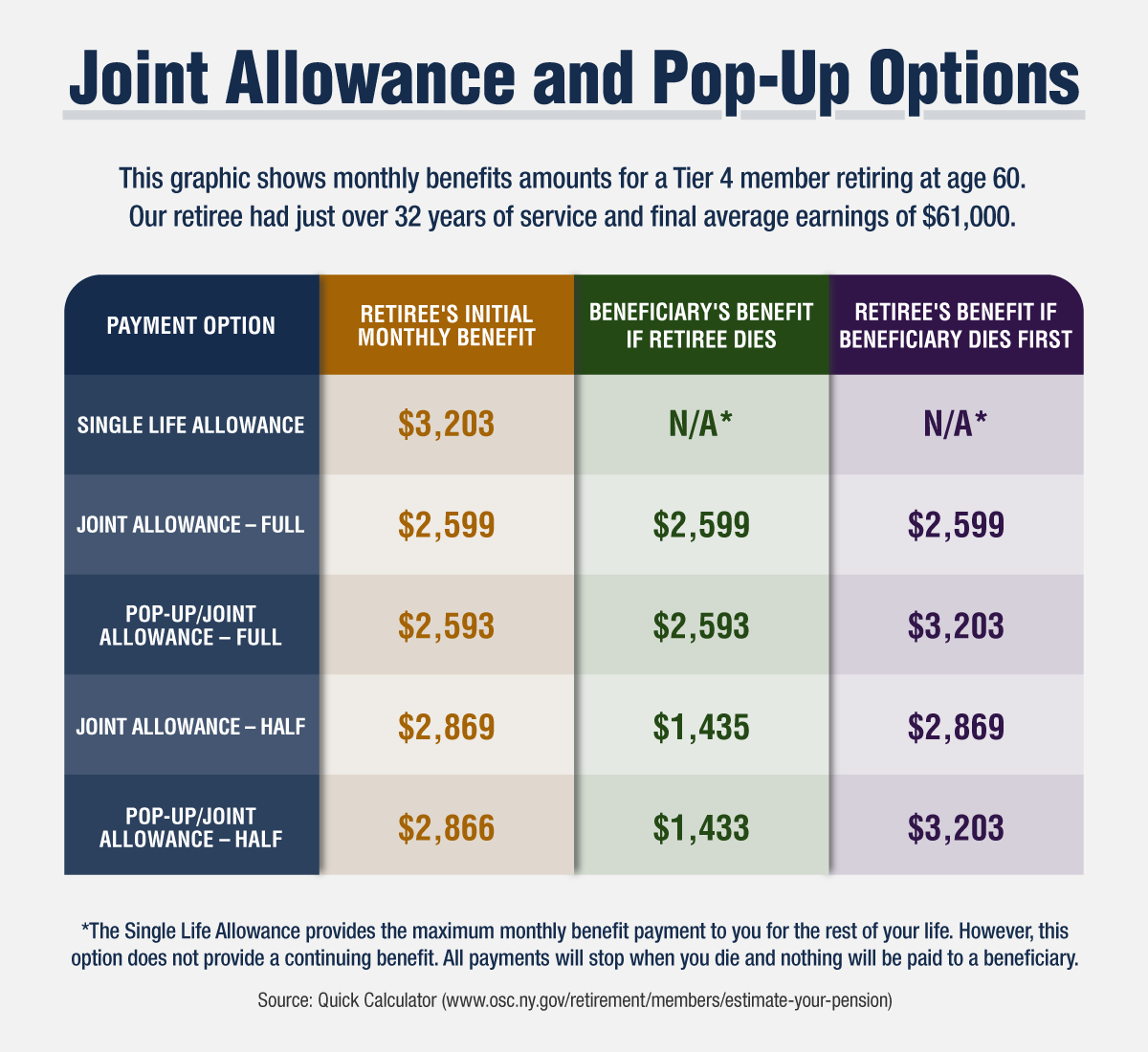

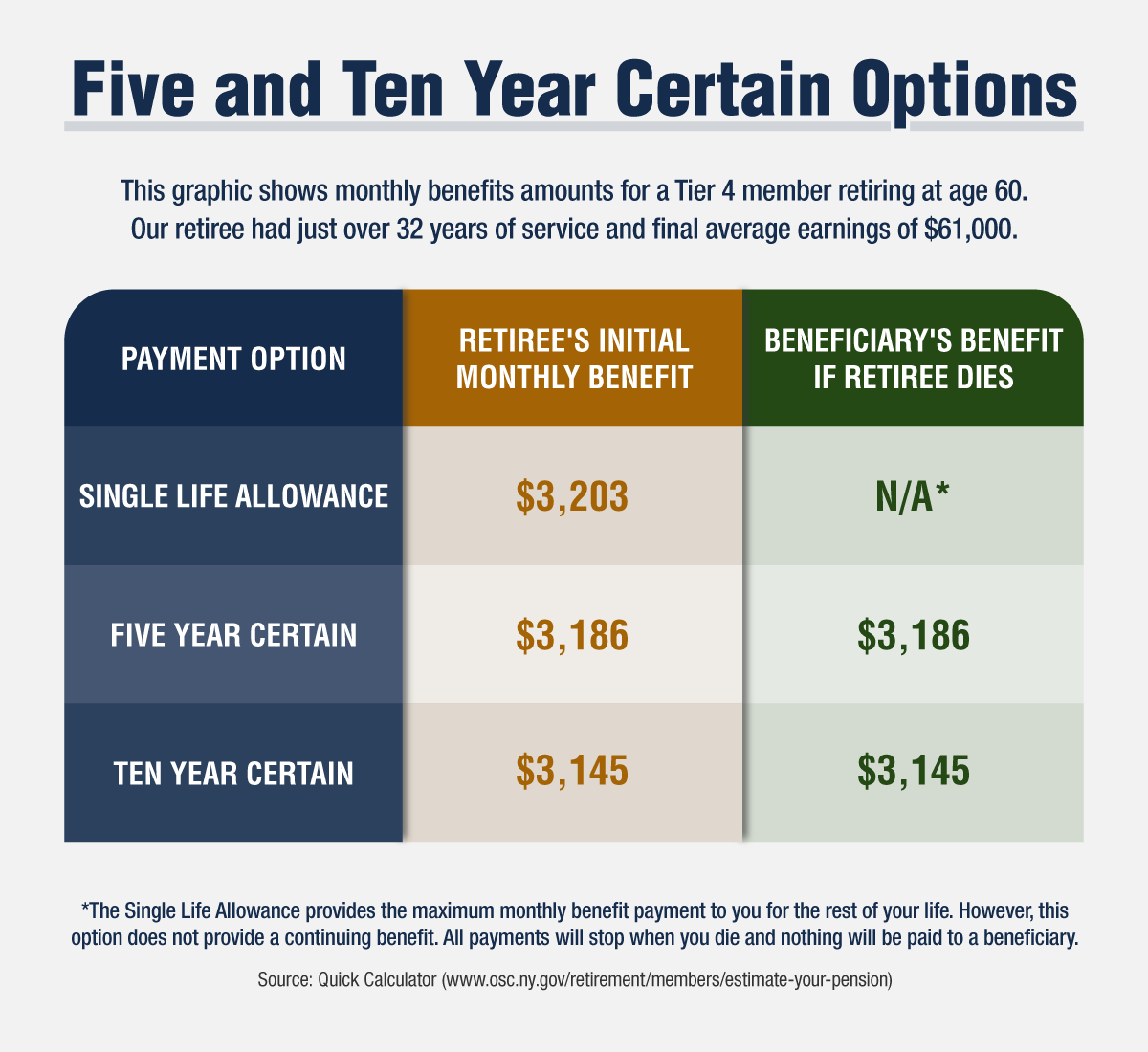

Select Your Pension Payment Option

You can choose from several pension payment options, all of which provide you with monthly pension payments for the rest of your life. The Single Life Allowance provides the maximum amount, but upon your death, payments will stop—there will be no continuing payments to a beneficiary, even if you die soon after retiring. Or, you can choose to receive a reduced monthly pension payment to provide for:

- A lifetime benefit to a single beneficiary after you die; or

- A limited benefit to one or more beneficiaries after you die.

Enter Federal Tax Withholding Information

Most NYSLRS pensions are subject to federal income tax, and NYSLRS is required to withhold federal income tax from your pension benefit at the default withholding status of “single with no adjustments” unless you inform us otherwise. Enter federal tax withholding information to adjust the amount withheld.

Note: NYSLRS pensions are not subject to New York State or local income tax. However, if you permanently move to another state, that state may tax your pension.

Sign Up for Direct Deposit

With direct deposit, your pension payment will be deposited directly into your bank account on the last business day of each month. It’s fast, convenient and secure. Save time and set up direct deposit pension payments when you apply for retirement by entering your bank account number and routing number.

If you have a joint account holder on your bank account, you’ll need to print and complete the Electronic Funds Transfer Direct Deposit Enrollment Application (RS6370) and have your joint account holder sign the form. It’s best to do this in advance so you can upload the completed form while adding your direct deposit information in Retirement Online. However, you can upload the completed form later.

Upload Proof of Date of Birth

You must submit proof of your date of birth before any pension benefits can be paid. If you select a pension payment option that provides a lifetime pension benefit to a beneficiary upon your death, you must submit proof of your beneficiary’s date of birth as well.

Upload one of the following acceptable documents:

- Birth certificate

- New York State driver’s license

- Passport or passport card

- Marriage certificate, if it shows your age on a given date or the date of birth

- Baptismal certificate

- Certificate of Release or Discharge from Active Duty (DD-214)

- Naturalization papers

If you don’t have one of these documents available when you apply online, you can submit them later. However, if your submission is not timely, your first payment may be delayed.

Pay Off Outstanding Loans and Service Credit Purchases

If you haven’t done so already:

- Pay off your NYSLRS loan.

- Pay off service credit purchases.

Review Your Employment History and Service Credit

You’ll see which employers reported service credit for you. Review your employment history and add any missing public employment.

You can request additional service credit for previous employment or military service, or you can request a transfer or tier reinstatement when you apply to retire. However, remember it’s best to make these requests well before you apply.

One Exception—Disability Retirement

You may be eligible for a disability retirement benefit if you are permanently disabled and cannot perform your duties because of a physical or mental condition. Applications for disability retirement can’t be submitted in Retirement Online. If you are applying for a disability retirement, you must submit a paper application. Visit our Disability Benefits page for more information.

For Benefit Information, Read Your Retirement Plan Publication

Your service and disability retirement benefits and death benefits are based on your tier, retirement plan, service credit, and other factors. For comprehensive information about your retirement benefits and how your pension will be calculated, find your NYSLRS retirement plan publication.