October is National Retirement Security Month. It’s a time to consider the importance of saving and to think about potential sources of income in retirement. Financial security doesn’t just happen—it takes preparation and time. Even if retirement seems far off, it’s never too early to start planning.

NYSLRS and Retirement Security

Check out these blog posts to learn more about how your NYSLRS pension and other sources of retirement income can provide retirement security.

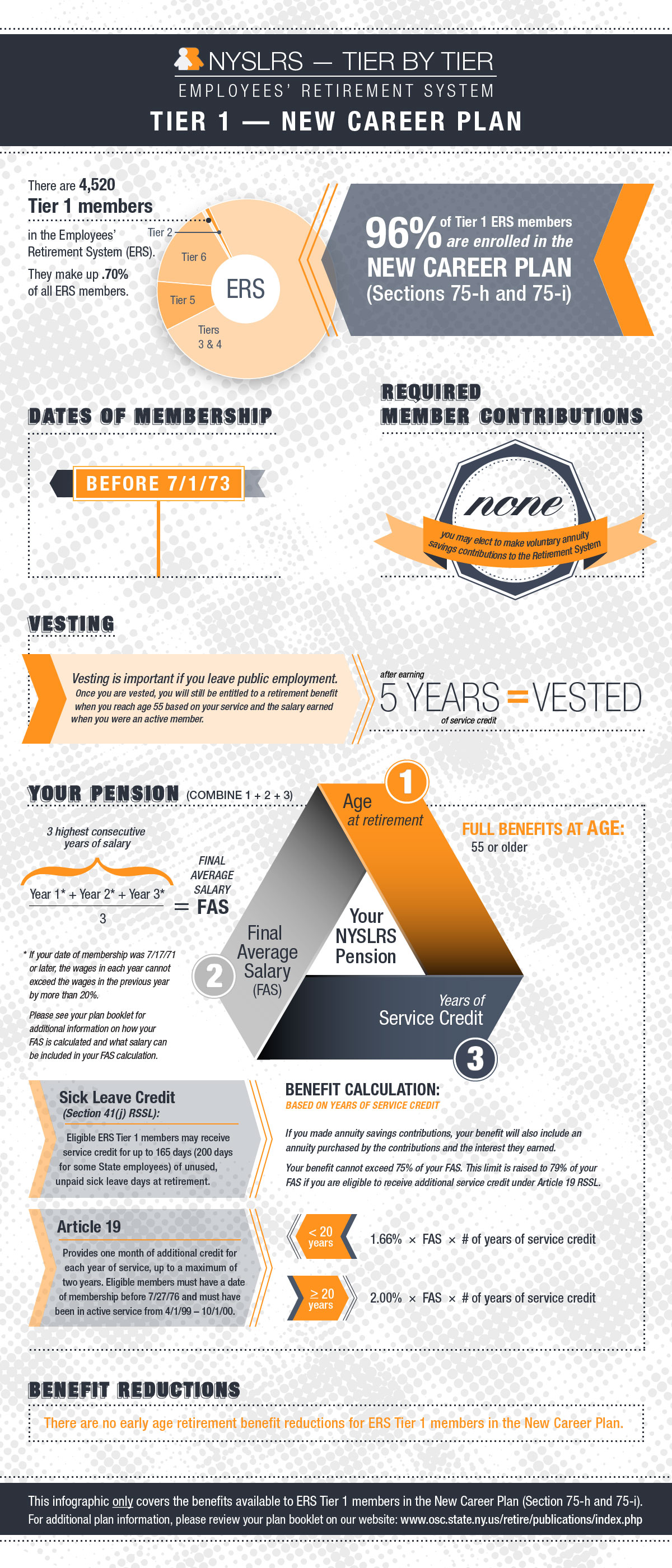

Your NYSLRS Pension—A Defined Benefit Plan

As a NYSLRS member, you are enrolled in a defined benefit plan, also known as a traditional pension plan. When you retire, you will receive a monthly pension payment for the rest of your life. Your pension will be calculated using a preset formula based on your earnings and years of service—it will not be based on the individual contributions you paid into the system.

The 3-Legged Stool Approach to Retirement Confidence

Your NYSLRS pension is a good reason to be optimistic about your finances in retirement. But there is more to a financially secure retirement than having a pension. Think of retirement security as a three-legged stool. Each leg is a source of income to help support you when your working days are done.

Compounding: Use Time to Grow Your Money More

If you want to improve your chances of a financially secure retirement, your plan should include retirement savings. It’s important to start saving early so your money has time to grow. When you invest your savings in an individual retirement account (IRA) or a 401(k)-style retirement savings plan, you earn a return on your investment, and those returns are compounded.

Deferred Compensation: Another Source of Retirement Income

For greater financial stability and flexibility, you may want to invest in a deferred compensation savings plan. The New York State Deferred compensation plans are voluntary retirement savings plans like a 401(k), created for New York State employees and employees of other participating public employers.

Debt and Retirement

As you get close to retirement, it’s a good idea to take inventory of any debt you owe. Paying down your debt—including any NYSLRS loans—will help avoid a pension reduction and can give you more flexibility in retirement.

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called