When you joined the New York State and Local Retirement System (NYSLRS), you were assigned to a tier based on the date of your membership. There are six tiers in the Employees’ Retirement System (ERS) and five in the Police and Fire Retirement System (PFRS) – so there are many different ways to determine benefits for our members. Our series, NYSLRS – One Tier at a Time, walks through each tier and gives you a quick look at the benefits members are eligible for before and at retirement.

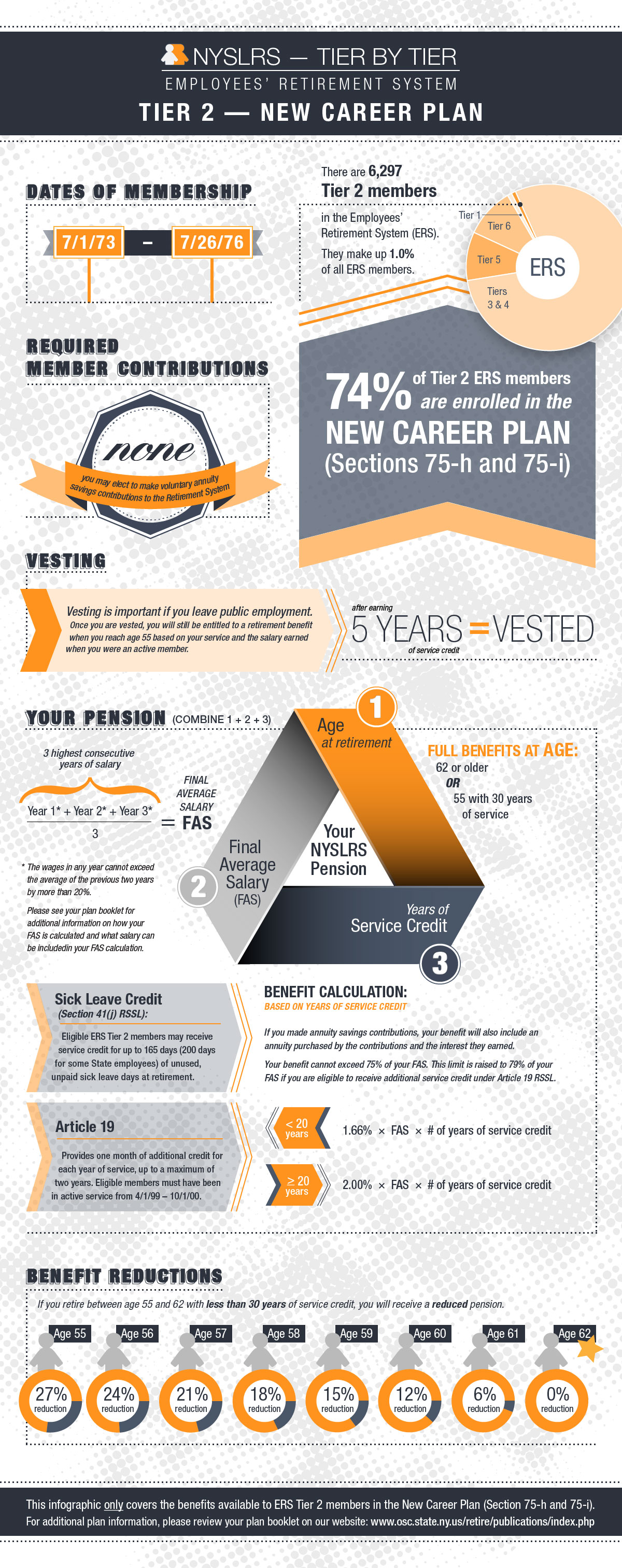

NYSLRS created Tier 2 on July 1, 1973, marking the first time NYSLRS created any new member group. Today’s post looks at one of the major Tier 2 retirement plans in ERS. ERS Tier 2 as a whole represents less than one percent of NYSLRS’ total membership.

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

- New Career Plan for ERS Tier 2 Members (VO1509)

- Career Plan for ERS Tier 2 Members (VO1508)

- State Correction Officers and Security Hospital Treatment Assistants Plan for ERS Tier 2 Members (VO1525)

- Sheriffs, Undersheriffs and Deputy Sheriffs Special Plan for ERS Tier 2 Members (VO1840)

- Non-Contributory Plan with Guaranteed Benefits for ERS Tier 2 Members (ZO1507)

- Non-Contributory Plan for ERS Tier 2 Members (ZO1506)

- Basic Plan for ERS Tier 2 Members (ZO1505)

- Legislative & Executive Retirement Plan for Tier 2 Members (VO1861)

Be on the lookout for more NYSLRS – One Tier at a Time posts. Next time, we’ll take a look at another ERS tier. Want to learn more about the different NYSLRS retirement tiers? Check out some earlier posts in the series:

Filing Forms with the Comptroller

Filing Forms with the Comptroller