If you’re planning to retire soon, it’s a good idea to take inventory of any debt you owe. Paying down your debt can give you flexibility to enjoy the type of retirement you want.

NYSLRS Loan Debt

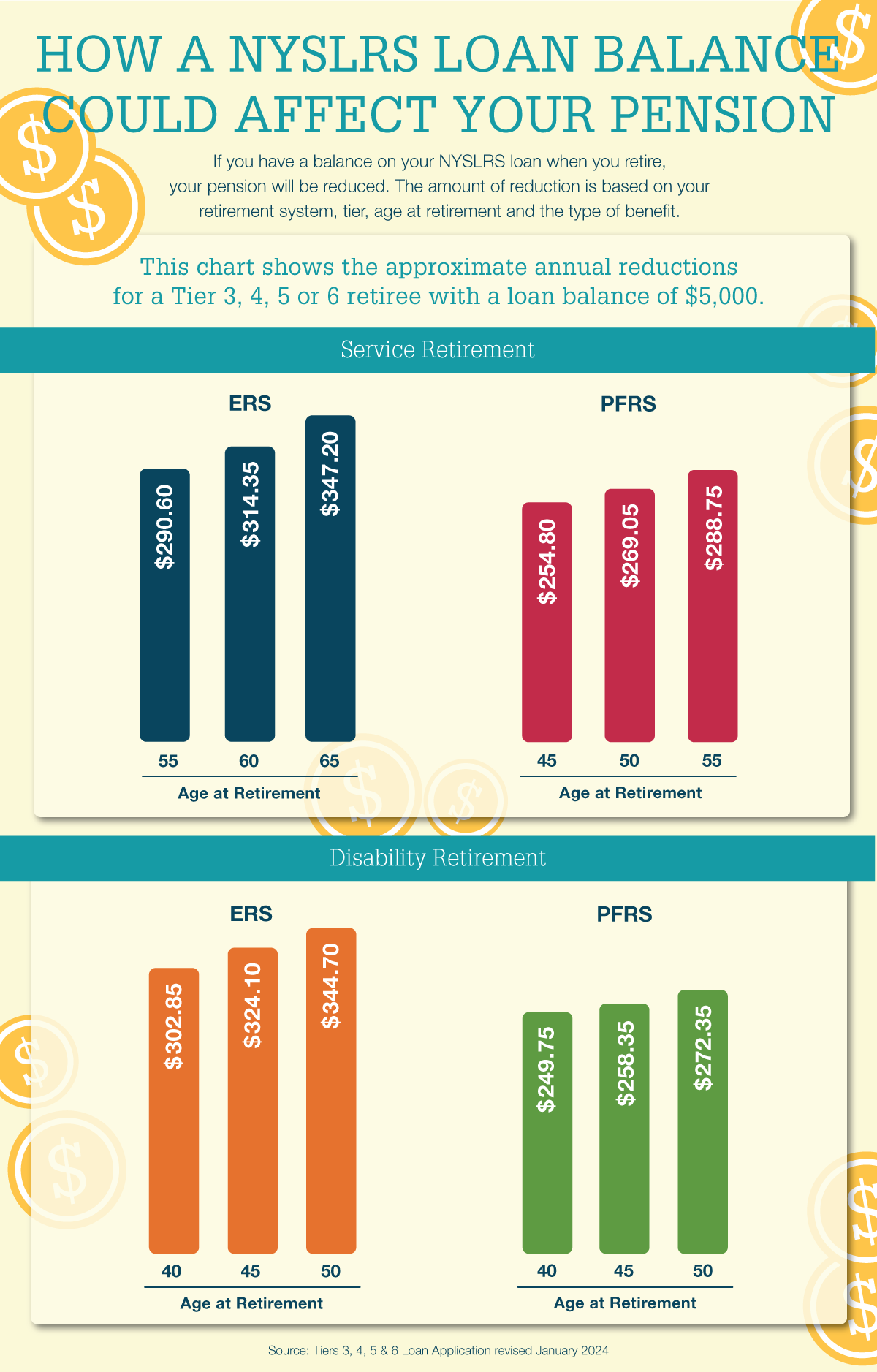

If you have an outstanding NYSLRS loan balance when you retire, it will reduce your pension. The amount of the reduction is based on:

- Your retirement system—Employees’ Retirement System (ERS) or Police and Fire Retirement System (PFRS);

- Your tier;

- Your age at retirement; and

- Whether you retire with a service retirement benefit or a disability retirement benefit.

It is important to understand:

- The reduction does not go toward repaying the outstanding loan balance—it’s a permanent reduction to your pension.

- At least part of the loan balance at retirement will be subject to federal income taxes.

When you apply for retirement in Retirement Online and have an outstanding NYSLRS loan balance, the system will provide a specific pension reduction amount for you. The loan applications on our Forms page also list general pension reduction information.

If you are close to retirement, be sure to check your loan balance. If it looks like you won’t repay your loan before you retire, you can increase your loan payments, make additional lump sum payments or both (see the Change Your Payroll Deductions or Make Lump Sum Payments section of our Loans: Applying and Repaying page).

ERS members may repay a loan after retiring. They must pay the full balance that was due at retirement in a single lump sum payment. Once they repay the loan, their pension will increase to the amount it would have been without the loan reduction. It will not increase retroactively back to the date of retirement.

Other Debt to Check

Credit Cards

Another priority should be paying off credit cards before retirement. Credit card statements include a warning telling you how long it will take—and how much it will cost—to pay off your balance making only minimum payments.

If you have more than one credit card balance, many financial advisors recommend paying as much as you can on the card with the highest interest rate, while still making at least the minimum payments on your lower-interest cards. Once you’ve paid off your highest-interest card, focus on the one with the next-highest rate, and so on. Other advisors say it might be better to pay off the card with the smallest balance first. The idea there is to gain a sense of accomplishment, and make the process seem less daunting.

Mortgages

Advice varies on whether you should try to pay off your mortgage before you retire. It would eliminate a major expenditure and let you spend your retirement income on other things. On the other hand, if your mortgage interest rate is relatively low, you may want to focus on paying off other high-interest debt or boosting your retirement savings. What works best for you will depend on your situation.

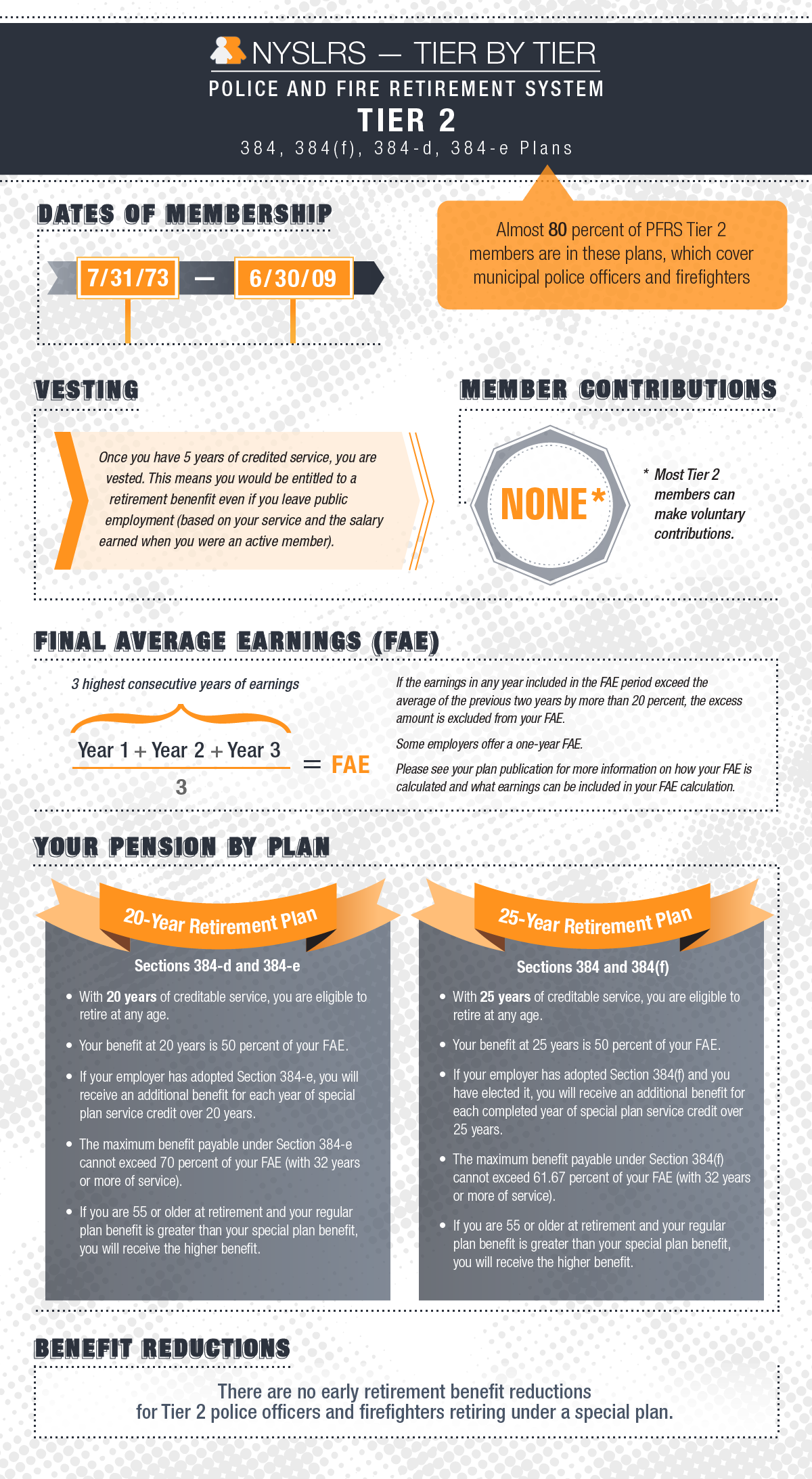

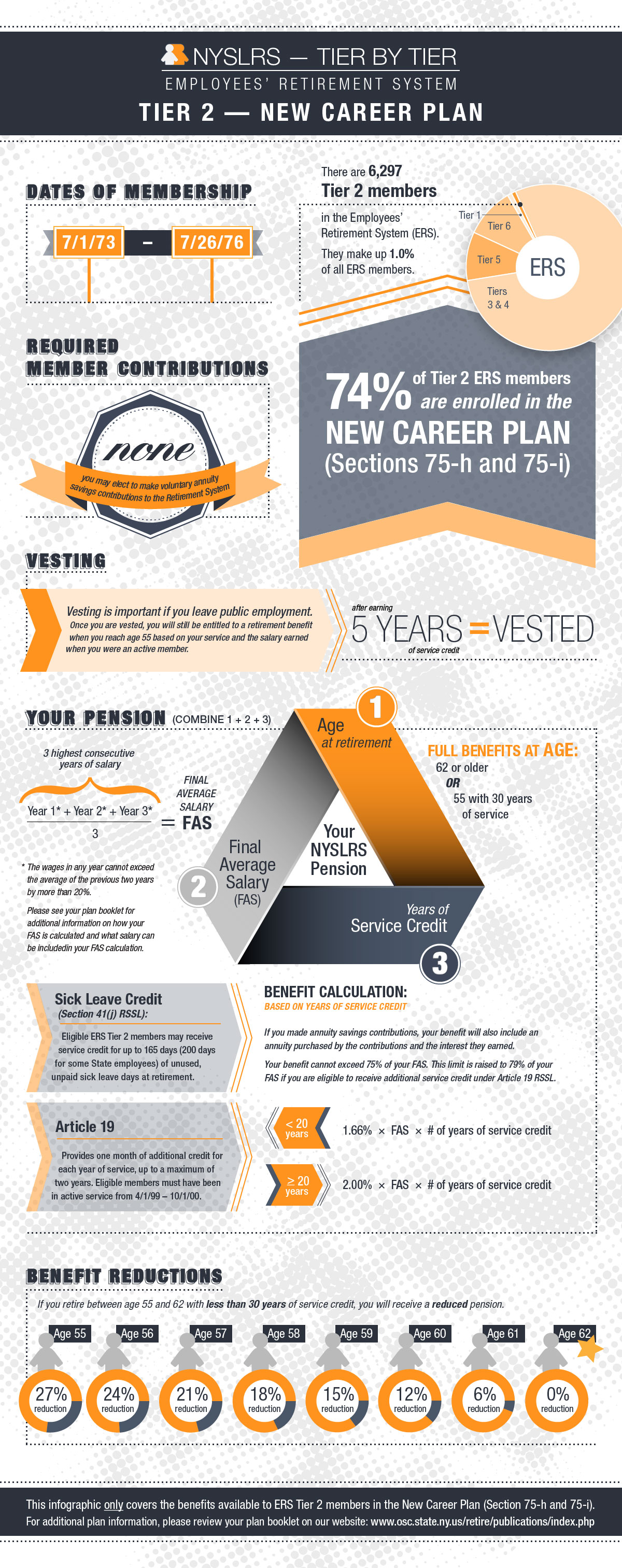

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits: