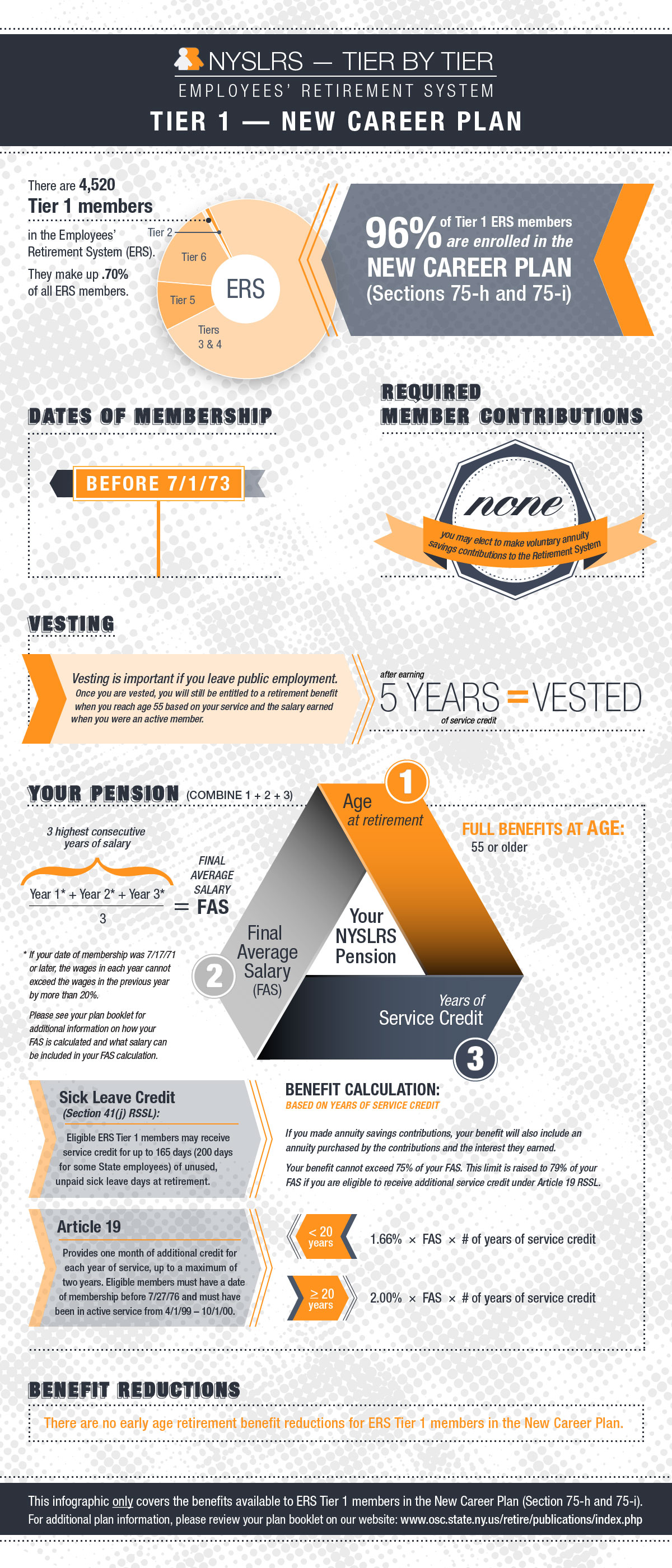

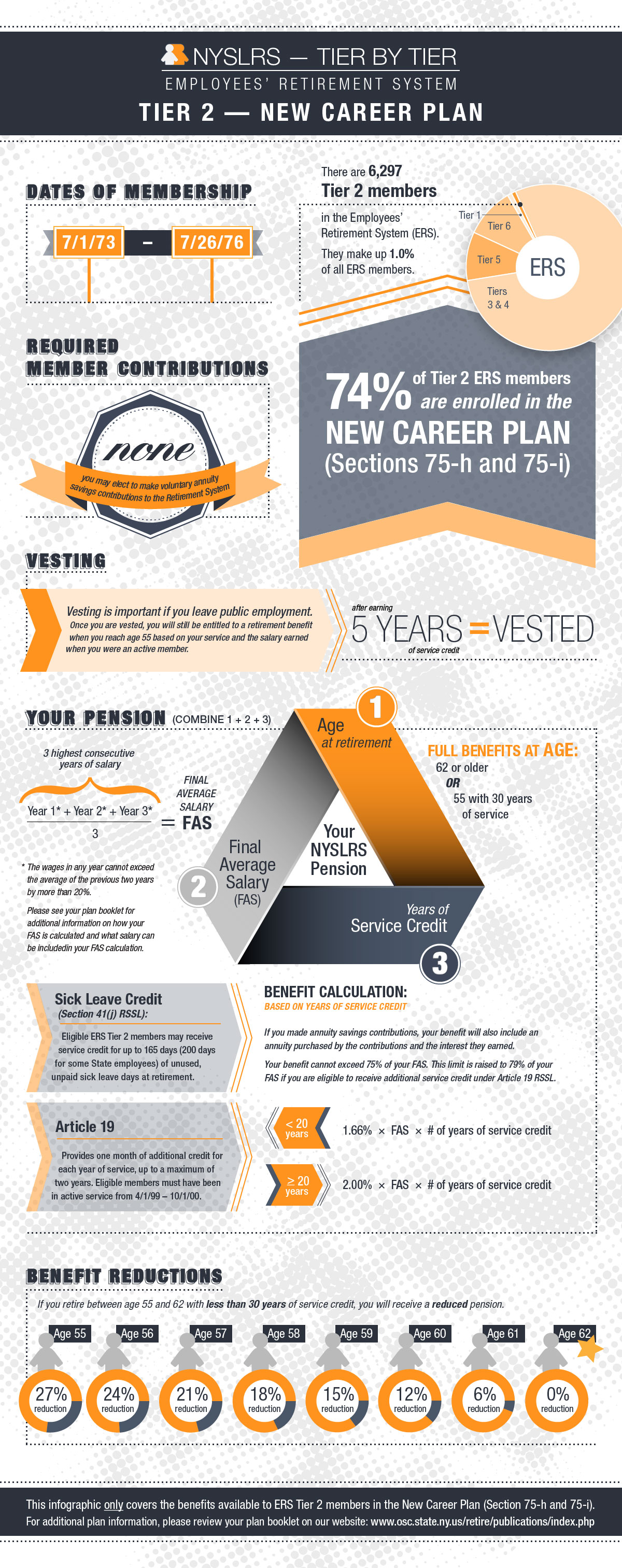

Did you become a member of the Employees’ Retirement System (ERS) before July 1, 1973? If you’re still working in public service, you’re one of the 3,508 active members in Tier 1. If you joined after July 1, 1973 but before July 27, 1976, then you’re one of 4,127 active members in Tier 2.

Most ERS Tier 1 and Tier 2 members are in the New Career Plan (Section 75-h or 75-i). Currently, 96 percent of active Tier 1 members and almost 95 percent of active Tier 2 members are covered by this plan. Here’s a quick look at the benefits in the New Career Plan:

Benefit Eligibility

Tier 1

- Members must be at least age 55 to be eligible to collect a retirement benefit.

- There are no minimum service requirements — they may collect full benefits at age 55.

Tier 2

- Members must have five years of service and be at least age 55 to be eligible to collect a retirement benefit.

- The full benefit age is 62.

- Almost 95 percent of active Tier 2 members are covered by the New Career Plan (Section 75-h or 75-i).

Final Average Salary

Final average salary (FAS) is the average of the wages earned in the three highest consecutive years of employment. For Tier 1 members who joined NYSLRS June 17, 1971 or later, each year used in the FAS calculation is limited to no more than 20 percent above the previous year’s earnings. For Tier 2 members, each year of earnings is limited to no more than 20 percent above the average of the previous two years’ earnings.

Benefit Calculations

- For Tier 1 and 2 members, the benefit is 1.66 percent of the FAS for each year of service if the member retires with less than 20 years. If the member retires with 20 or more years of service, the benefit is 2 percent of the FAS for each year of service.

- Tier 1 members and Tier 2 members with 30 or more years of service can retire as early as age 55 with no reduction in benefits.

- Both Tier 1 and Tier 2 members who worked continuously from April 1, 1999 through October 1, 2000 receive an extra month of service credit for each year of credited service they have at retirement, up to a maximum of 24 additional months.

If you have questions about the New Career Plan, please read the Tier 1 plan publication or the Tier 2 plan publication. You can find other plan publications on our website.