When it comes to understanding your finances, a good place to start is by calculating your net worth.

Net worth is the total value of everything you own, minus the money you owe. It is a measure of your wealth and an indicator of your financial condition. It can also provide you with valuable insight as you start developing your financial plan for retirement.

How to Calculate Net Worth

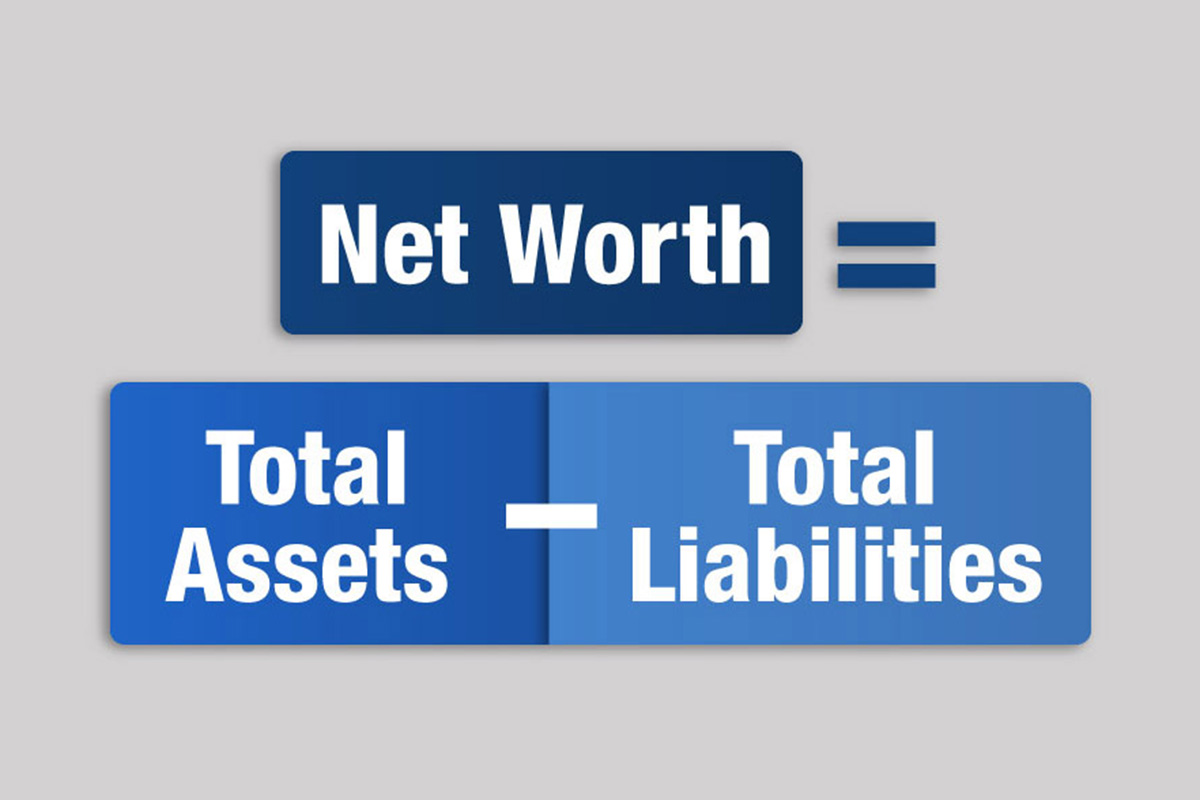

The formula for calculating your net worth is simple:

Assets and Liabilities

Your assets are items of value that you own, including:

- Your house

- Other real estate (a vacation home, rental property)

- Money in checking and saving accounts

- Retirement savings, such as a 401(k) or Deferred Compensation account

- Stocks, bonds and other investments

- Your car and other vehicles

- Jewelry, furniture and household items

Your liabilities are your debts. Your mortgage, credit card debts and loan balances factor into your total liabilities.

If you owe more than the value of your total assets, you have a negative net worth. A negative net worth may not necessarily mean you’re in financial trouble — it just means that at the moment you have more debts than assets.

If you’re just beginning your career and still have student loans, you may find yourself in negative territory. But your net worth is likely to increase over time as you pay down debts and save money.

Knowing Your Net Worth Can Help You Get a Handle on Your Finances

Your net worth shows your current financial status. When you know where you stand, you’ll be better prepared to make decisions about spending, saving and investing, which will help you achieve your short- and long-term financial goals. Your net worth can show you where you’re doing well and where there’s room for improvement. For example, it may indicate a need to curb your spending or reduce your credit card debt.

Your net worth is likely to change over time, so it’s a good idea to calculate it periodically. With this updated financial information, you’ll be able to track trends and make adjustments if necessary.

To learn more about net worth and what it means, you may wish to read What’s Your Net Worth Telling You?