To receive this benefit, you must retire directly from public service or within a year of leaving. The additional service credit for your unused, unpaid sick leave, up to a certain limit, will be added to your total years of service when calculating your pension benefit. However, it cannot be used to:

Qualify for vesting. For example, if you have four years and ten months of service credit and you need five years to be vested, your sick leave credit cannot be used to reach the five years.

Qualify for a better retirement benefit calculation. For example, if you have 19 ½ years of service credit but your pension calculation will improve substantially if you have 20 years, your sick leave credit cannot be used to reach the 20-year calculation.

Meet the service credit requirement for a special 20- or 25-year plan.

Increase your pension beyond the maximum allowed under your retirement plan.

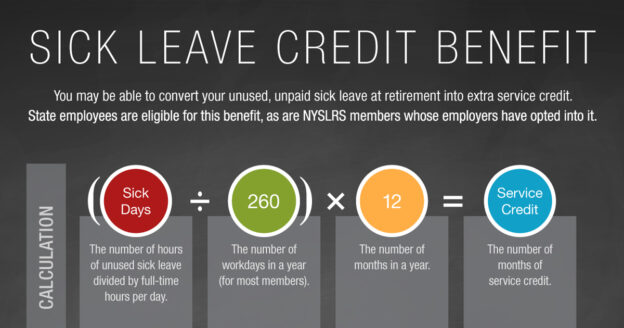

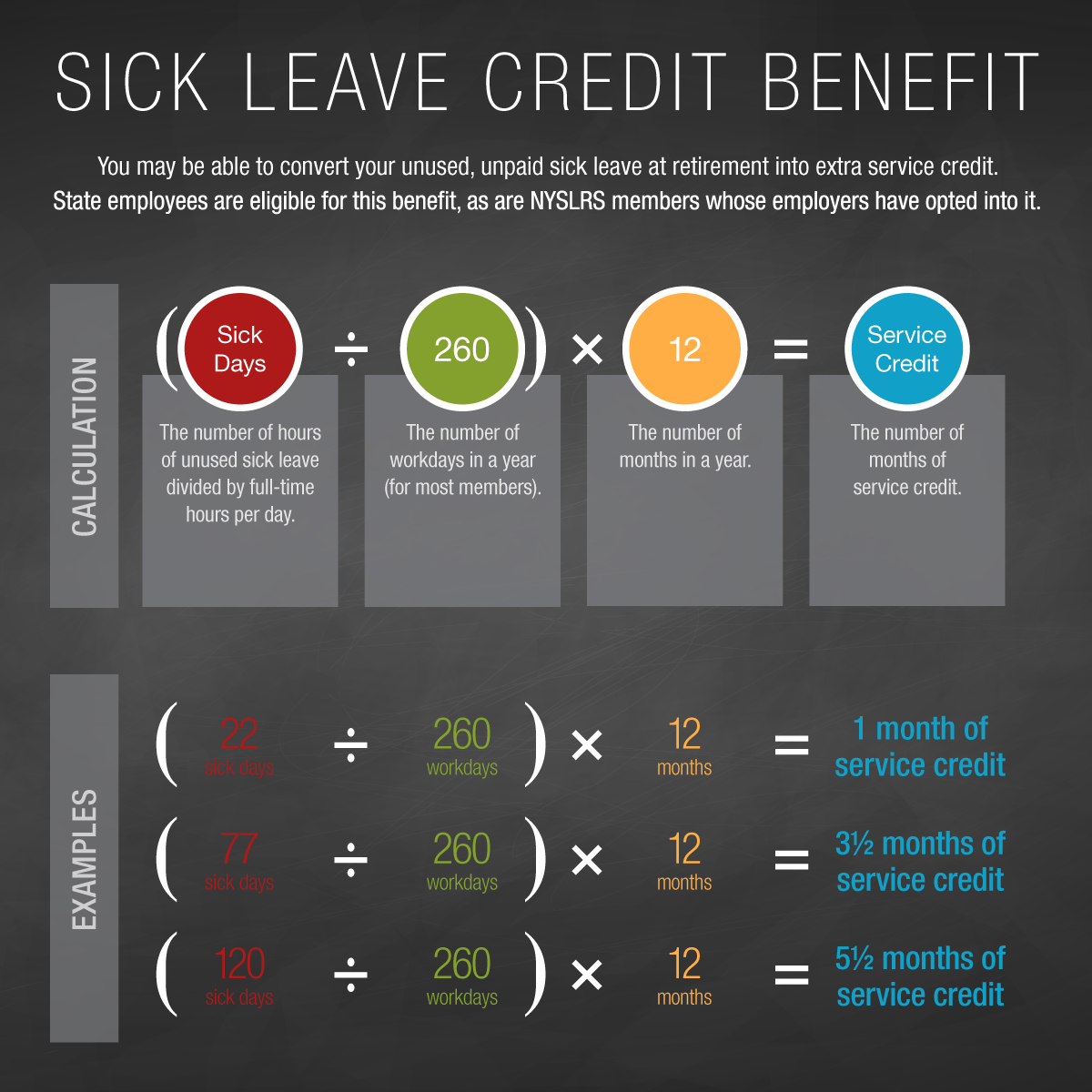

The additional service credit is based on your total hours of unused, unpaid sick leave and the number of hours in your employer’s standard workday.

For More Information

For comprehensive information about your retirement benefits and how your pension will be calculated, find your retirement plan publication. And as you approach retirement, read our Preparing for Retirement blog post for guidance, including topics to consider and actions to take as you plan.

Retirement is a big step, and we want to make sure you’re ready when the time comes. Read on for guidance on preparing for retirement, including topics to consider as you plan and actions to take.

Understand Your NYSLRS Pension

Your NYSLRS pension will be based on your tier, service credit, final average earnings and your retirement plan. For most members, age is also an important factor in your NYSLRS benefits.

Service credit is one of the major factors in calculating your pension benefit, so it’s important to make sure you get credit for all your public service. You may be able to request additional service credit if you:

Worked for your current or another public employer before joining NYSLRS; or

Served in the U.S. Armed Forces and received an honorable discharge from active military duty.

Or you may be able to:

Transfer service: If you are still a member of another New York State public retirement system.

Reinstate service: If you withdrew your membership in NYSLRS or another New York State public retirement system.

You must submit your request before retirement, and you should do it as early in your career as possible. NYSLRS will need time to request records from your previous employer or retirement system, and requesting early also gives you time to pay for additional or reinstated service. Also, the sooner you purchase your credit, the less it will generally cost.

Pay Off Service Credit Purchases

If you requested additional service credit for previous public employment or military service and you received a cost letter, make sure you’re on track to pay off your service credit purchase before you retire.

You won’t receive credit for optional service that is not paid off when you retire.

If you are in the process of paying for mandatory service credit (for example, from a reinstated membership or if insufficient contributions were made to NYSLRS) and it’s not paid off by your date of retirement, your pension will be permanently reduced.

Sign in to Retirement Online to check your service credit purchase balance, make a lump sum payment or increase your payroll deduction amount.

Pay Off Your NYSLRS Loan

It’s important to understand the implications of retiring with an outstanding loan. Your pension will be permanently reduced, and in most cases, you’ll need to report at least some portion of the loan balance as income to the Internal Revenue Service (IRS). If you retire before age 59½, the IRS may also charge an additional 10% penalty.

To ensure you’re on track to pay off your loan before you retire, sign in to Retirement Online to check your balance, make a lump sum payment or increase your payroll deduction amount.

Estimate Your Pension

Finding out how much you can expect to receive is a critical step in preparing for retirement. Most members can estimate their pension using Retirement Online in just a few quick and easy steps.

Retirement Online uses your current earnings and service information to calculate your estimate, including your final average earnings (FAE) and the amounts for the pension payment options available to you. You can fine-tune your estimate or see how different choices would affect your benefit.

Remember, the amounts are estimates, not a guarantee of what you’ll receive when you retire.

Understand How Divorce May Affect Your Pension

In New York State, pensions and retirement benefits earned during the marriage may be marital property and can be divided when a marriage ends. Divorce can affect your pension and other retirement benefits in the following ways:

Your ex-spouse may be entitled to a portion of your pension.

You may be required to name your ex-spouse as the beneficiary of any death benefit.

You may be required to choose a pension payment option that provides a continuing benefit to your ex-spouse when you die.

Your ex-spouse may be entitled to a portion of your cost-of-living adjustment (COLA).

Any division of pension and retirement benefits must be stated in the form of a Domestic Relations Order (DRO)—a court order issued after a final judgment of divorce which specifies how benefits should be split.

It’s important to complete and submit your DRO to NYSLRS well before you apply for retirement to avoid changes or delays in your pension payments.

Check Your Eligibility for the Sick Leave Benefit

To be eligible for the Sick Leave Benefit, your employer must have adopted Section 41(j) of the Retirement and Social Security Law (RSSL) for ERS members or 341(j) of the RSSL for PFRS members. If your employer has chosen to offer this benefit, you may receive service credit for unused, unpaid sick leave at retirement.

To check if this benefit is available to you, ask your employer or sign in to Retirement Online and look for Sick Leave Eligibility.

To receive this benefit, you must retire directly from public service or within a year of leaving. The additional service credit for your unused, unpaid sick leave, up to a certain limit, will be added to your total years of service when calculating your pension benefit. However, it cannot be used to:

Qualify for vesting. For example, if you have four years and ten months of service credit and you need five years to be vested, your sick leave credit cannot be used to reach the five years.

Qualify for a better retirement benefit calculation. For example, if you have 19 ½ years of service credit but your pension calculation will improve substantially if you have 20 years, your sick leave credit cannot be used to reach the 20-year calculation.

Meet the service credit requirement for a special 20- or 25-year plan.

Increase your pension beyond the maximum allowed under your retirement plan.

Review Your Health Insurance Coverage

NYSLRS does not administer health insurance programs. When you’re nearing retirement, you should check with your employer’s human resources or personnel office or your health benefits administrator to determine your eligibility for health insurance coverage during retirement. If your former employer instructs us to do so, we will deduct health insurance premiums from your monthly pension payment, but NYSLRS cannot answer questions about coverage or changes in premium amounts.

If you are eligible to use your unused, unpaid sick leave to offset the cost of NYSHIP, payment towards your health insurance coverage will not affect your eligibility for the Sick Leave Benefit.

Schedule a Pre-Retirement Consultation

Before you apply for retirement, you may want to consider scheduling a pre-retirement consultation where you can speak with one of our representatives to review your benefits and ask any questions you may have.

Ready to Apply for Retirement?

When you’re ready, Retirement Online makes it fast and convenient to apply for retirement. There are no forms to mail in and nothing to have notarized. You’ll see an estimate of your pension, including the amounts for the pension payment options available to you. You’ll also be able to upload documents while applying or after submitting your application. And if you need to update your application, you can quickly and easily submit changes. But before applying, visit our Preparing and Applying for Retirement page for an overview of the retirement application so you know what to expect and what information you’ll need to submit.