Recognizing Firefighters

It’s National Fire Prevention Week this week and, while attention is properly focused on promoting fire prevention, we also think it’s a great time to recognize all the firefighters who are members of the New York State and Local Retirement System (NYSLRS).

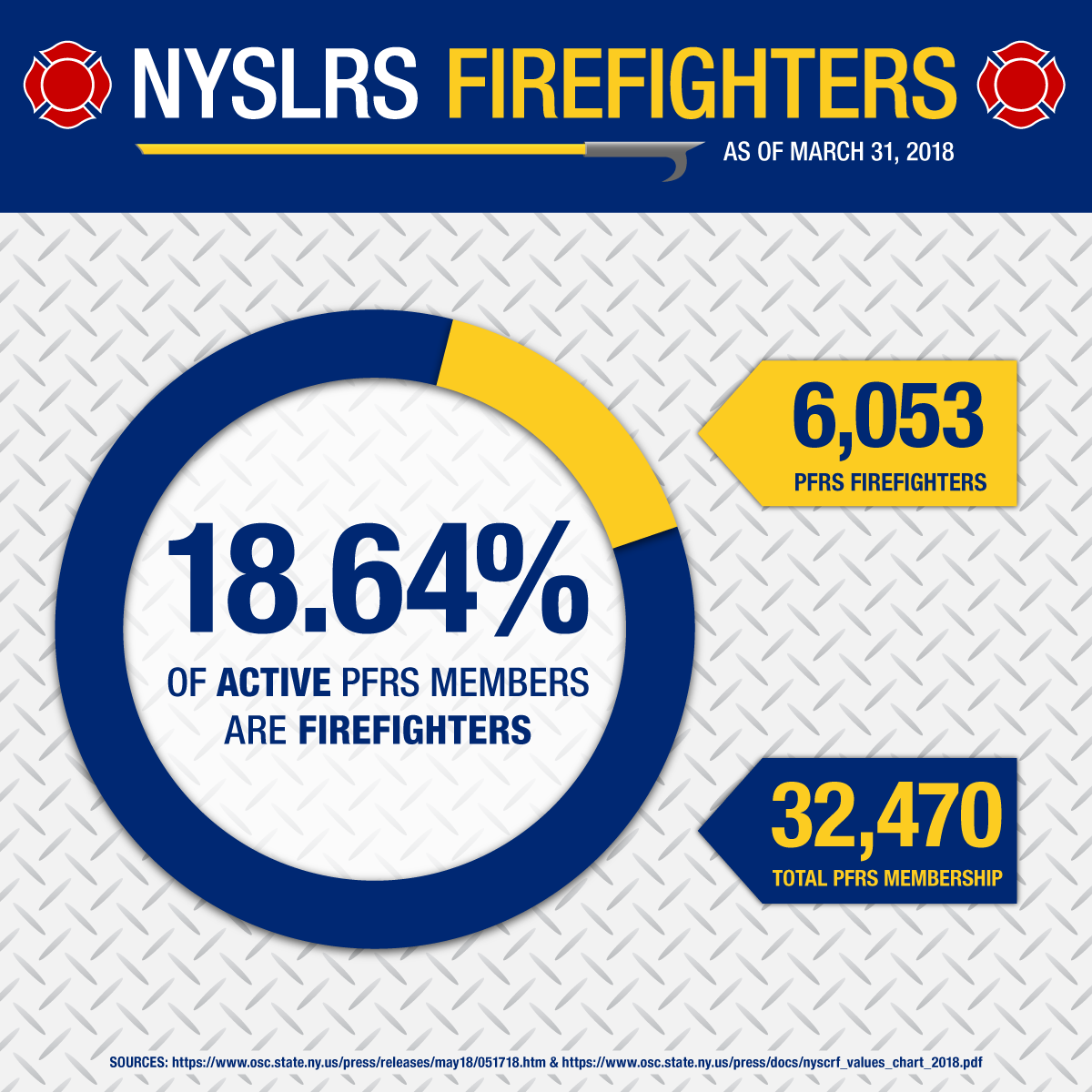

Of the 533,415 members in NYSLRS, 32,470 are in the Police and Fire Retirement System (PFRS). More than 6,000 of these brave men and women are firefighters.

NYSLRS Membership and Firefighters

All firefighters working for participating employers are PFRS members. With that membership comes a variety of benefits, including certain death and disability benefits as well as a pension. As firefighters and other PFRS members progress through their careers they become eligible for these benefits. For example, from day one, PFRS members are covered by job-related death and disability benefits. However, with ten years of service credit, most members are also eligible for a non-job-related disability benefit.

In addition, most PFRS employers offer their employees special retirement plans. A special plan lets members retire after completing 20 or 25 years of credited service in specific job titles rather than reaching a certain age. Most firefighters — and, in fact, nearly 80 percent of all PFRS members (25,784) — are enrolled in a set of special 20- and 25-year plans. Whether members need 20 or 25 years depends on their retirement plan.

Firefighters are Heroes

To the members of the New York State Professional Fire Fighters Association, the Firemen’s Association of the State of New York and the New York State Association of Fire Chiefs; to the county fire marshals, supervising fire marshals, fire marshals, assistant fire marshals, assistant chief fire marshals and chief fire marshals: Thank you for your service to New York and its citizens. We are grateful for the valuable service you provide all of us.