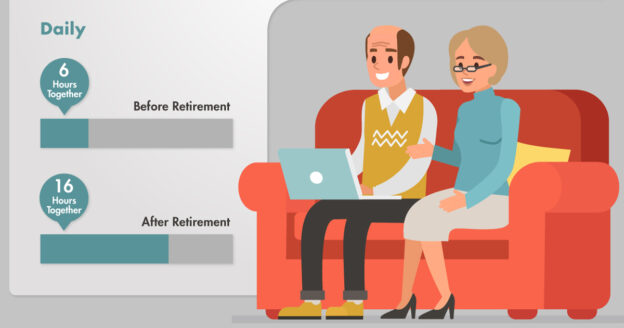

Could retirement bring you too much free time? When people think about retirement planning, they usually think about money. Will you have enough to maintain a comfortable lifestyle for a retirement that could last decades? But regardless of your finances, there is one thing you’re likely to have a lot more of after you retire: time. Figuring out how you’ll spend that time should also be part of your retirement planning process.

Counting the Hours

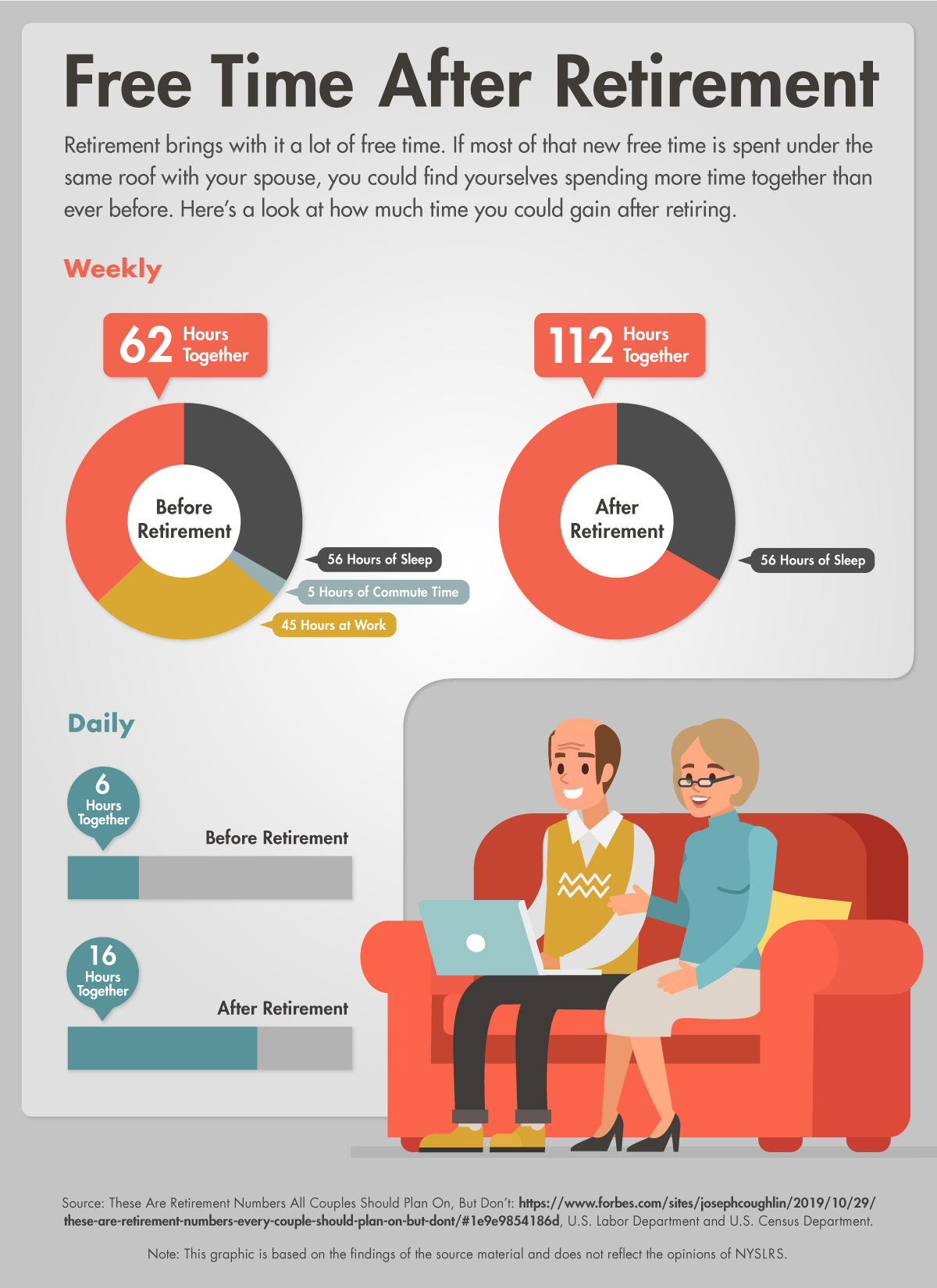

According to the U.S. Labor Department, the average American worker spends about nine hours a day at work. Add another hour a day commuting time, and that’s ten hours a day or 50 hours each week.

All those hours you spent working, and traveling to and from work, will instantly become free time. While that may sound great to many people, all that extra time can have downsides.

If not put to good use, that extra time can lead to boredom and even depression. What’s more, if you’re married and you and your spouse are both retired, you may find yourselves wondering how to spend that time together.

Make a Plan for Free Time

For many couples, having extra time together is a dream come true. However, some couples find themselves getting in each other’s way, and that can sometimes lead to problems.

But there are ways to cope. For example, finding activities outside the home, both together and separately, can help. As with most things, you’ll be better off if you recognize there may be a problem, discuss it with your spouse, and come up with a plan.

There are more thoughts on the subject, and some good advice, in this article: 10 Tips to Help Your Marriage Survive Retirement.

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.