When you join the New York State and Local Retirement System (NYSLRS), you’re assigned a tier based on the date of your membership. There are six tiers in the Employees’ Retirement System (ERS) and five in the Police and Fire Retirement System (PFRS). Each tier has a different benefit structure established by New York State legislation.

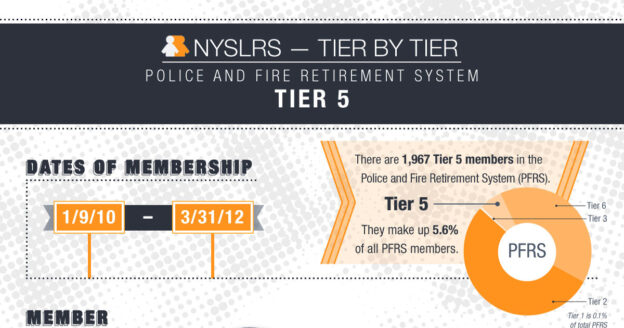

Our series, NYSLRS — One Tier at a Time, walks through each tier to give you a quick look at the benefits in both ERS and PFRS. Today’s post looks at PFRS Tier 5. Anyone who joined PFRS from January 9, 2010 through March 31, 2012 is in Tier 5. There were 1,967 PFRS Tier 5 members as of March 31, 2021, making up 5.6 percent of PFRS membership.

About Special Plans

Under a regular plan, you need to reach certain age and service requirements to receive your NYSLRS pension. If you’re covered by a special plan, there is no age requirement, and you can receive your pension after completing 20 or 25 years of service.

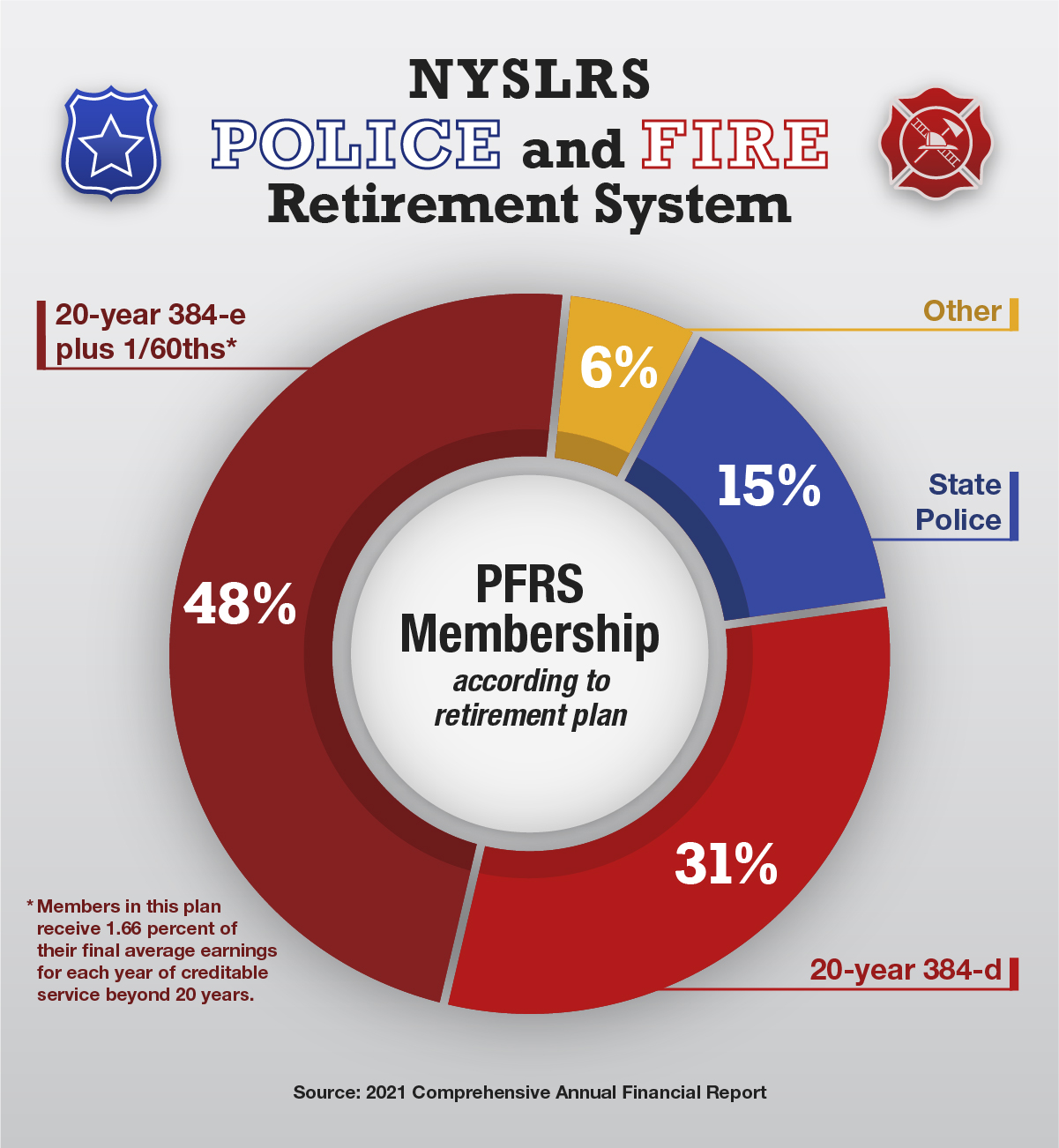

Nearly 80 percent of PFRS members are in plans covered under Sections 384, 384-d, 384-e or 384-f of the Retirement and Social Security Law. Read our Police and Fire Retirement System blog post for information about different PFRS plans.

Check out the graphic below for the basic retirement information for PFRS Tier 5.

If you’re a PFRS Tier 5 member, you can find detailed information about your benefits in the retirement plan booklets listed below:

- Special 20- and 25-Year Plans (Sections 384, 384-d and 384-e)

- State Police Plan (Section 381-b)

- Regional State Park Police Plan (Section 383-a)

- En-Con Police Officers Plan (Section 383-b)

- State University Police Plan (Section 383-d)

- Forest Rangers Plan (Section 383-c)

- New Career Plan (Sections 375-h and 375-i)

- Career Plan (Sections 375-f and 375-g)

- Non-Contributory Plan With Guaranteed Benefits (Section 375-e)

- Police and Fire Plan (Sections 375-b and 375-c)

- Basic Plan with Increased-Take-Home-Pay (ITHP) (Section 370-a, 371-a & 375)

For special plans under miscellaneous titles, please visit our Publications page.

Check out other posts in the PFRS series:

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines