If you’re already building your retirement savings, you already understand how those savings, along with Social Security, work together with your pension to help provide financial stability in retirement. Financial advisors call this the “three-legged stool.”

But why not take it a step further and give your retirement savings a boost? Even a small increase could make a big difference over time, while having minimal impact on your take-home pay.

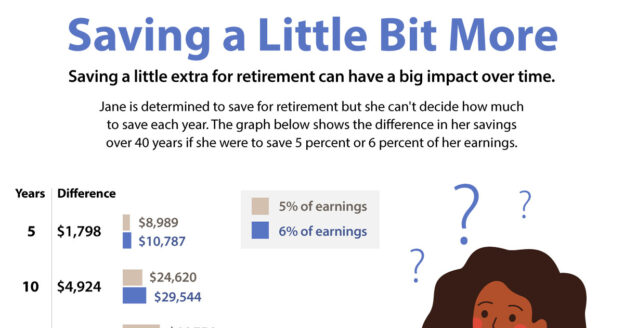

How much of a difference would it make? You can check it out yourself using this online calculator and your own salary and savings information. Calculate the impact of your current savings, then try the same calculation with an additional 1 percent of your earnings. For example, if you’re saving 5 percent of your pay, see what saving 6 percent would do by the time you expect to retire.

Impact on Your Paycheck

Fortunately, adding a small amount to your retirement savings won’t have a substantial impact on your paycheck. For example, if you’re making $60,000 a year, 1 percent is only $600. That’s just $50 a month or, if you are paid every other week, about $23 per payday.

The impact on your take-home pay would be even less if you save in a tax-deferred plan because you won’t have to pay income tax on those earnings until after you retire. The New York State Deferred Compensation Plan’s paycheck impact calculator can help you estimate how increased savings would affect your paycheck. (You don’t have to have a Deferred Compensation account to use their calculator. The New York State Deferred Compensation Plan is not affiliated with NYSLRS.)

When to Increase Retirement Savings?

The sooner you boost your savings, the better off you’ll be. But if you’re not ready to increase your savings right now, then try this: Schedule your increase to coincide with your next raise. That way, you may not even miss the money.

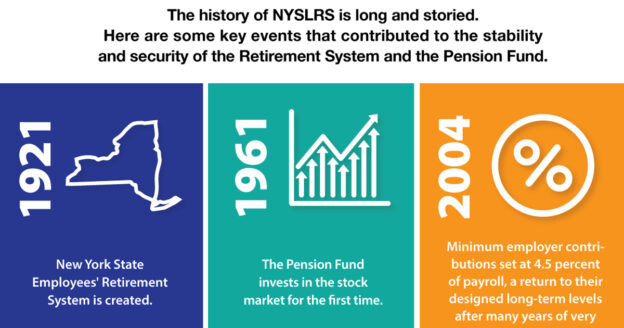

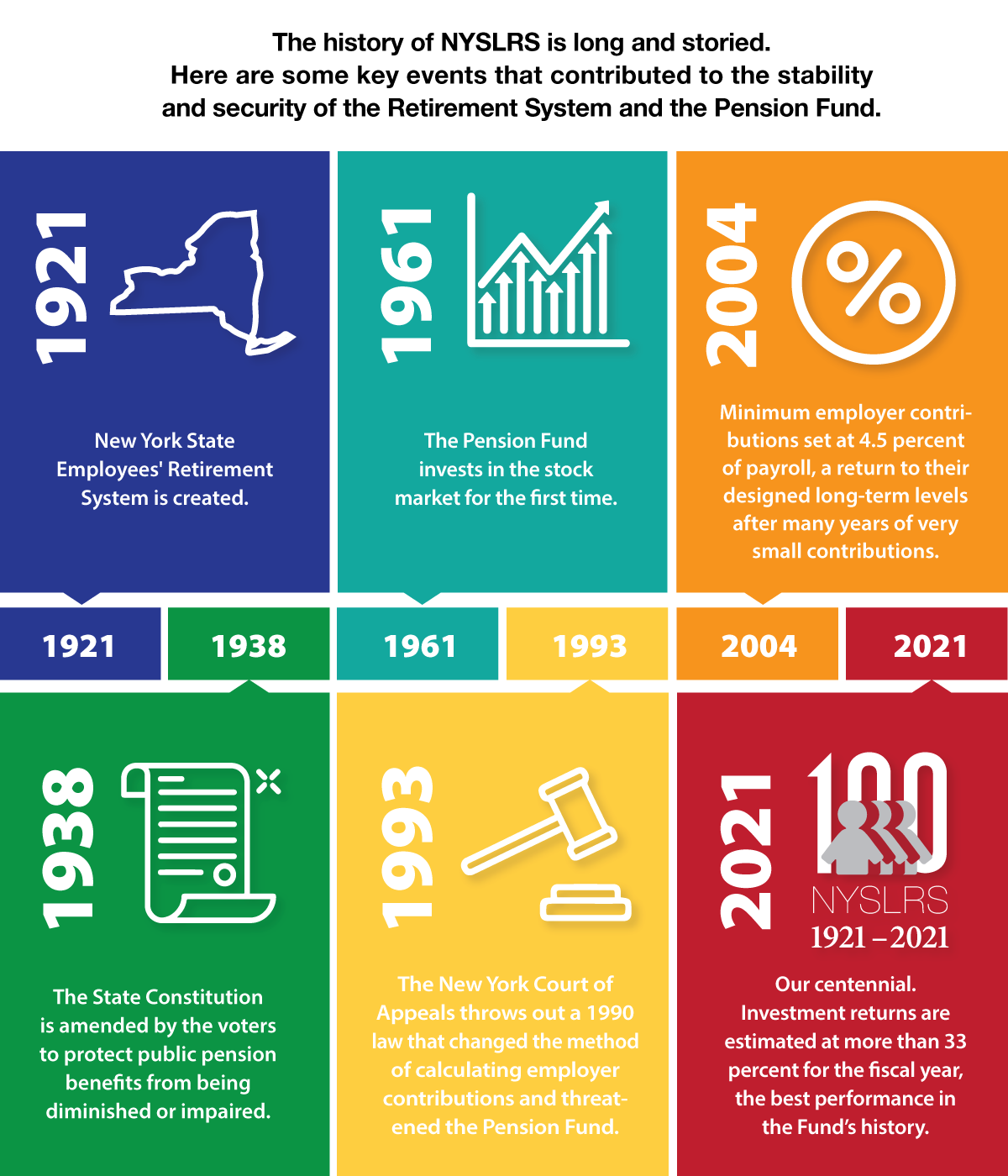

A century after its creation, the New York State and Local Retirement System (NYSLRS) is widely recognized as one of the best-managed and best-funded public pension systems in the nation. Comptroller DiNapoli recently announced that the New York State Common Retirement Fund (Fund), which holds and invests the assets of NYSLRS, had an estimated value of $268.3 billion as of June 30, 2021. The security and stability of NYSLRS and the Fund are due, in large part, to the stewardship of Comptroller DiNapoli, as well as a long line of State Comptrollers that came before him. The System has also been bolstered by some key events along the way.

In the Beginning

NYSLRS’ security and stability were built in at the start. In 1918, the State Legislature created the Commission on Pensions and charged it with recommending a pension system for State workers.

After surveying pension plans in New York and other states, the Pension Commission recognized the need to calculate the cost of the pension plan through actuarial calculations, which take into account such things as employees’ salaries and how long they are expected to be retired. They also saw the need to make provisions to cover those costs through contributions and other income. They recommended a plan supported by the contributions of employers (New York State and, eventually, local governments) and employees. The improved actuarial calculations the System uses today helps to ensure that member contributions and employer annual contributions are sufficient to keep the System adequately funded.

The Pension Commission also recommended a service retirement benefit be made available to workers who reached a certain age, based on average earnings and years of service. Though they didn’t use the term, their pension plan was very similar to the defined-benefit plan NYSLRS members have now.

Unlike the 401k-style defined-contribution plans common in the private sector today, a defined-benefit plan provides a guaranteed, lifetime benefit. With a defined-benefit plan, you don’t have to worry about your money running out during retirement, and your employer has an excellent tool for recruiting and retaining workers.

Constitutional Protection

In 1938, New York voters approved several amendments to the State Constitution, including Article 5, Section 7, which guarantees that a public pension benefit cannot be “diminished or impaired.” This constitutional language protects the interests of the Fund and its members and beneficiaries, ensuring that the money the Fund holds will be there to pay the pensions for all current and future retirees. The courts have upheld this constitutional provision to protect the Fund several times over the years.

For NYSLRS members and retirees, that means the retirement benefits you were promised when you started your public service career cannot be reduced or taken away.

Sound Investments

Sound investments are crucial to the health of the Fund, but in some cases changes in the law were needed to give Fund managers the flexibility to make the best investments. In 1961, the Fund was allowed to invest in the stock market, opening up the door for growth opportunities. Roughly half of the Fund’s assets are currently invested in stocks.

In 2005, the Legislature expanded the types of investments the Fund could make, allowing the Fund to increase investments in real estate, international stocks and other sectors that had been providing high returns.

Today, under Comptroller DiNapoli’s leadership, the Fund’s investment returns cover the majority of the cost of retirement benefits. After suffering a drop in value at the beginning of the COVID pandemic, the Fund had its best year in history, with estimated investment returns of 33.55 percent for fiscal year 2021.

NYSLRS is well-positioned to face the challenges of the future and provide retirement security for more than 1.1 million members, retirees and beneficiaries.

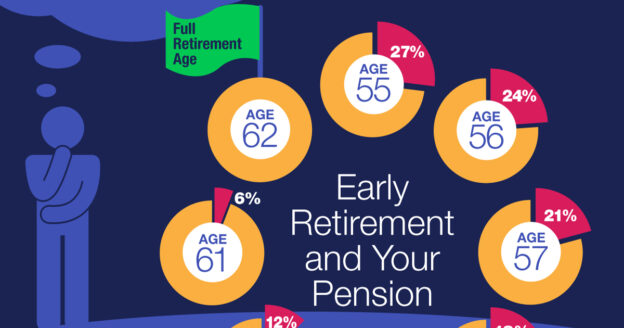

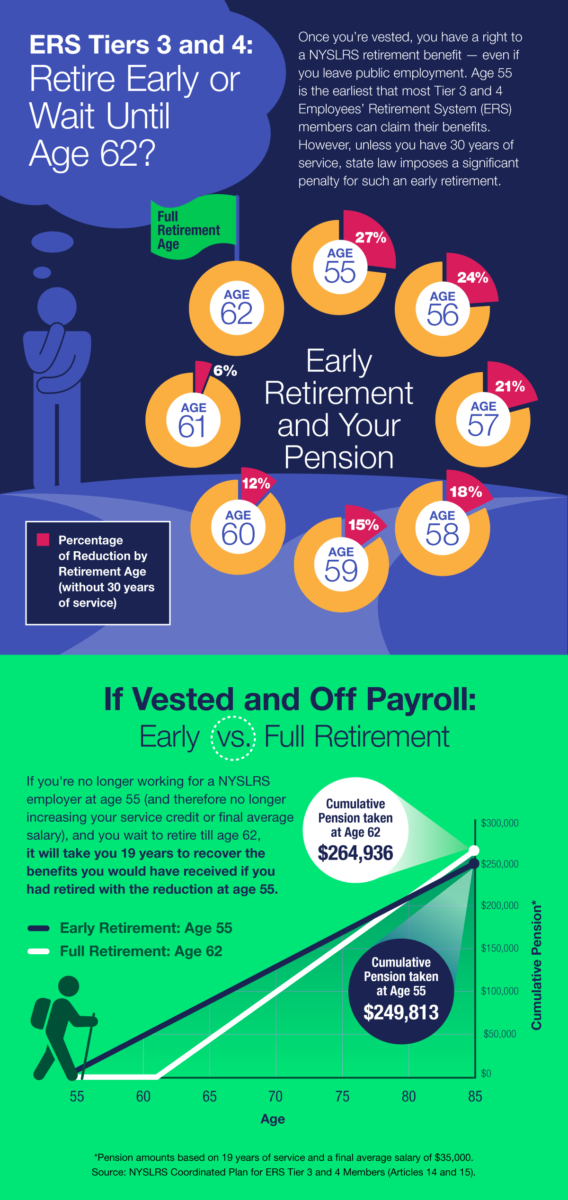

Tier 3 and 4 members in the Article 15 retirement plan qualify for retirement benefits after they’ve earned five years of credited service. Once you’re vested, you have a right to a NYSLRS retirement benefit — even if you leave public employment. Though your pension is guaranteed, the amount of your pension depends on several factors, including when you retire. Here is some information that can help you determine the right time to retire.

Three Reasons to Keep Working

Tier 3 and 4 members can claim their benefits as early as age 55, but they’ll face a significant penalty for early retirement – up to a 27 percent reduction in their pension. Early retirement reductions are prorated by month, so the penalty is reduced as you get closer to full retirement age. At 62, you can retire with full benefits. (Tier 3 and 4 Employees’ Retirement System (ERS) members who are in the Article 15 retirement plan and can retire between the ages of 55 and 62 without penalty once they have 30 years of service credit.)

Your final average earnings (FAE) are a significant factor in the calculation of your pension benefit. Since working longer usually means a higher FAE, continued public employment can increase your pension.

The other part of your retirement calculation is your service credit. More service credit can earn you a larger pension benefit, and, after 20 years, it also gets you a better pension formula. For Tier 3 and 4 members, if you retire with less than 20 years of service, the formula is FAE × 1.66% × years of service. Between 20 and 30 years, the formula becomes FAE × 2.00% × years of service. After 30 years of service, your pension benefit continues to increase at a rate of 1.5 percent of FAE for each year of service.

If You’re Not Working, Here’s Something to Consider

Everyone’s situation is unique. For example, if you’re vested and no longer work for a public employer, and you don’t think you will again, taking your pension at 55 might make sense. When you do the math, full benefits at age 62 will take 19 years to match the money you’d have received retiring at age 55 — even with the reduction.

An Online Tool to Help You Make Your Decision

Most members can use Retirement Online to estimate their pensions.

A Retirement Online estimate is based on the most up-to-date information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit, which could help you determine the right time to retire. When you’re done, you can print your pension estimate or save it for future reference.

If you are unable to use our online pension calculator, please contact us to request a pension estimate.

This post has focused on Tier 3 and 4 members. To see how retirement age affects members in other tiers, visit our About Benefit Reductions page.

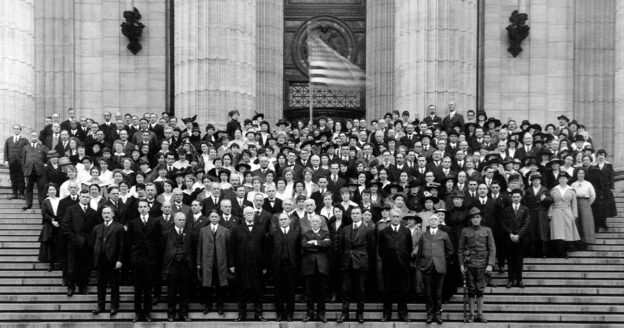

On January 3, 1921, NYSLRS began helping New York’s public employees achieve financial security in retirement. Now – 100 years later – we continue to fulfill that promise.

NYSLRS’ Origins

In 1920, Governor Al Smith signed legislation establishing the New York State Employees’ Retirement System.

In 1920, the State Commission on Pensions presented Governor Al Smith a report they’d been working on for two years. The report showed that though there were already pension plans covering 8,300 banking department employees, teachers, State hospital workers, Supreme Court and other certain judiciary employees and prison employees, 10,175 State employees were not covered. To help ensure the financial security of public employees during their retirement years, the Commission recommended that a system be established to pay benefits to State employees – and the Commission wanted a system that would always have enough money on hand to pay benefits.

On May 11, 1920, Governor Smith signed legislation creating the New York State Employees’ Retirement System. By June 30 1921, 43 retirees were drawing pensions. The total amount of their annual pensions was $17,420.16. The first disability pension benefit of $256 per year was also paid.

Still Fulfilling Our Promise After 100 Years

Today, there are more than one million members, retirees and beneficiaries in our system, and NYSLRS is one of the strongest and best funded retirement systems in the country. Last fiscal year, NYSLRS paid out $13.25 billion in retirement and death benefits.

Members of the Employees’ Retirement System gather on the steps of the State Education Department building in Albany, NY in 1921.

Our core mission for the last 100 years has been to provide our retirees with a secure pension through prudent asset management. This has been our promise since 1921 and will continue far into the future.

Sources: Report of the New York State Commission on Pensions, March 30, 1920; Chapter 741 of the Laws of 1920; and Report of the Actuary on the First Valuation of the Assets and Liabilities of the New York State Retirement System as of June 30, 1921.

The New York State and Local Retirement System (NYSLRS) consists of two retirement systems: the Employees’ Retirement System (ERS) and the Police and Fire Retirement System (PFRS). Your job title determines what system you’re in. In some cases, however, it’s possible to have a dual membership, to be a member of both systems.

How Does Dual Membership Work?

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines your tier in each membership.

Implications of Dual Membership

As a member of both systems, you’d have separate membership accounts. Let’s look again at our fire-fighting bus driver example. While working as a firefighter, you make any required contributions and earn service credit toward your PFRS pension only. The same is true for your work as a bus driver—your required contributions and earned service credit only go toward your ERS pension, not your PFRS pension.

There are other implications to dual membership. Assuming you’re vested in both memberships and meet the service credit and age requirements, you could retire and collect a pension from both systems. You’d need to file separate retirement applications for ERS and PFRS, and we’d calculate each pension separately. We’d calculate your ERS pension using the final average earnings (FAE) you earned as a bus driver and your PFRS pension using the FAE from your time as a firefighter.

And, since you’d have both an ERS pension and a PFRS pension, you would need to choose a beneficiary for each in the event of your death.

Questions?

You’ll want to make sure to know the details of your retirement plan in each system. If you have questions about dual membership, or want to discuss your particular situation when you decide to retire, please contact us.

Retirement comes too soon for some people. Poor health, an injury, family situations, layoffs and other unforeseen circumstances could force you into an unplanned retirement.

You may already have a plan based on the date you would like to retire, but do you have a backup plan if that date comes a few years earlier than expected?

Know Your Benefits

As a NYSLRS member, you’re entitled to benefits that may help. Most vested members can begin collecting a lifetime pension as early as age 55, though your benefit may be permanently reduced if you retire before full retirement age. (Full retirement age for NYSLRS members is either 62 or 63, depending on your tier. Full retirement age for Social Security benefits depends on your year of birth.)

Doing your homework is important. The more you understand the potential benefits available to you, the better you can estimate your income if you are forced to retire early. Unfortunately, the numbers you come up with may not be enough when dealing with an unplanned retirement.

But one potential source of income can make a big difference: retirement savings. Your savings could help you get by until you are eligible to collect your NYSLRS pension or another retirement benefit. If you are not saving for retirement, consider starting now. And if you are saving, consider increasing your savings. It could become a lifeline if the unexpected happens.

New York State employees and some municipal employees can also save for retirement through the New York State Deferred Compensation Plan. Ask your employer if you are eligible.

For more information about the benefits offered by your NYSLRS retirement plan, visit our website to read your plan publication.

NYSLRS manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.

Special plans are a little different. With special plans, NYSLRS members can receive a pension after completing 20 or 25 years of service. There is no age requirement; you can retire at any age once you have the full amount of required service credit. Both ERS and the Police and Fire Retirement System (PFRS) have special plans.

Special Plans for Special Services to the State

As of March 31, 2018, seven percent of active ERS members and 98 percent of active PFRS members are in special plans. These members fill roles such as:

Police officer;

Firefighter;

Correction officer;

Sheriffs undersheriff, and deputy sheriff; and

Security hospital treatment assistant.

Public employees in jobs like these face dangers and difficulties throughout their careers. They fight fires, patrol our neighborhoods, assist ill patients and more. We’d like to take this opportunity to thank them for the challenging, sometimes life-threatening work they do each day.

If you’d like to learn more about your retirement plan, please visit the Publications page of our website and review your plan publication. If you’re not sure which booklet covers your benefits, you can check your Member Annual Statement, ask your employer or send us an email using our secure contact form.

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called Required Minimum Distributions (RMDs), you could face significant penalties.

RMDs are never eligible for rollover into other retirement accounts. You must take out the money and pay the taxes.

Calculating the Distribution

The RMD amount must be calculated annually. It’s based on the account’s balance at the end of the previous calendar year and the life expectancy of you and your beneficiary. Check out AARP’s Required Minimum Distribution Calculator for an easy way to determine your required distributions. Many retirement plan administrators, including the New York State Deferred Compensation Plan, will inform you of your RMD amount, but it’s your responsibility to take the required distribution.

Potential Penalty

If you don’t take the required distribution, or if you withdraw less than the required amount, you may have to pay a 50 percent tax on the amount that was not distributed. (You must report the undistributed amount on your federal tax return and file IRS Form 5329.)

The IRS may waive the penalty if you can show that your failure was due to a “reasonable error” or that you have taken steps to correct the situation. You can find information about requesting a waiver on page 8 of the Form 5329 instructions.

What Accounts Require Minimum Distributions?

Most retirement accounts you’re familiar with require these annual withdrawals:

457(b) plans

IRAs (traditional, SEP and SIMPLE)

401(k) plans

403(b) plans

Profit-sharing plans

Money purchase plans

Since contributions to Roth IRAs have already been taxed, the IRS does not require distributions from Roth IRAs at any age.

As with most things investment-related, a lot depends on your particular circumstances. If you have questions, contact your financial advisor or your plan administrator.

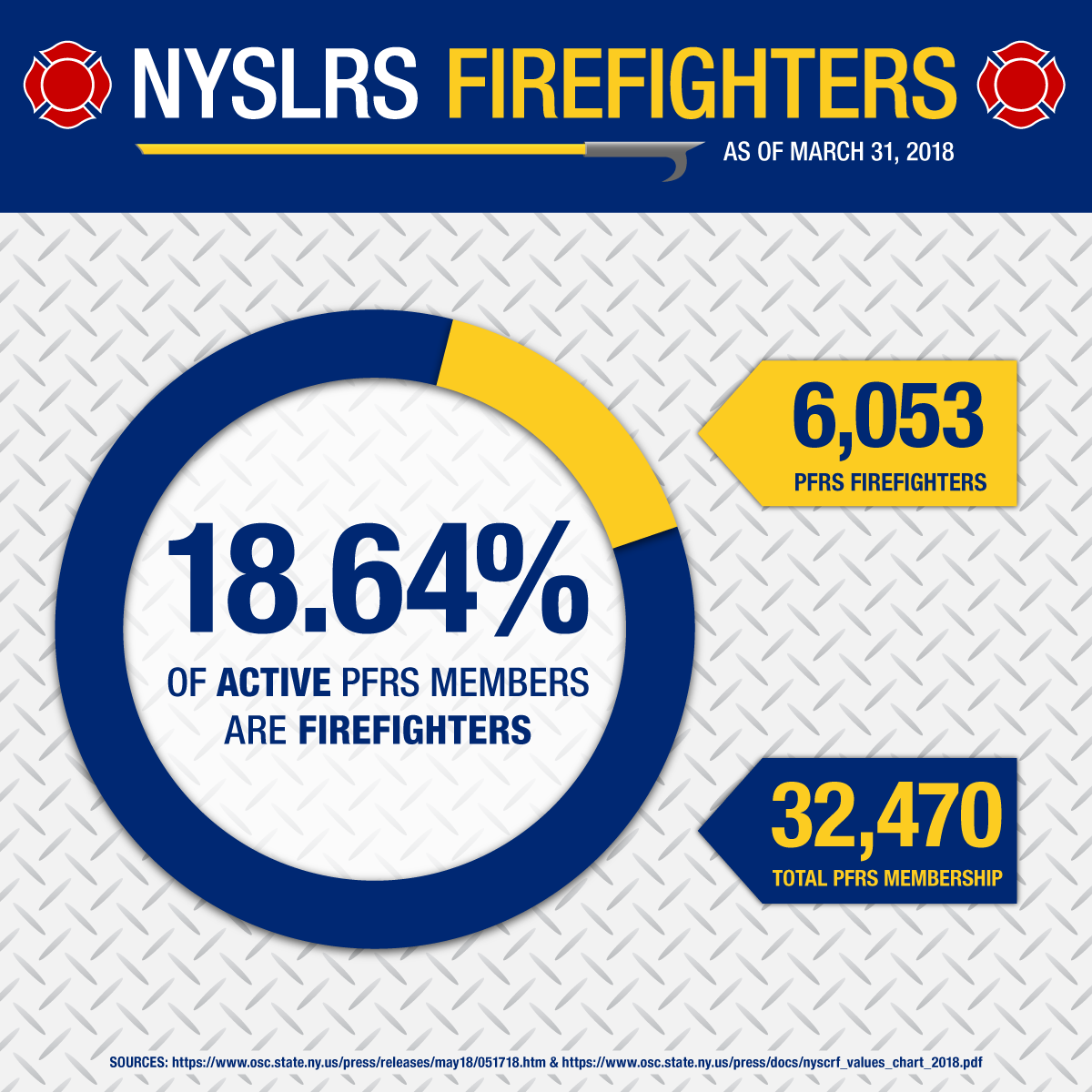

It’s National Fire Prevention Week this week and, while attention is properly focused on promoting fire prevention, we also think it’s a great time to recognize all the firefighters who are members of the New York State and Local Retirement System (NYSLRS).

Of the 533,415 members in NYSLRS, 32,470 are in the Police and Fire Retirement System (PFRS). More than 6,000 of these brave men and women are firefighters.

NYSLRS Membership and Firefighters

All firefighters working for participating employers are PFRS members. With that membership comes a variety of benefits, including certain death and disability benefits as well as a pension. As firefighters and other PFRS members progress through their careers they become eligible for these benefits. For example, from day one, PFRS members are covered by job-related death and disability benefits. However, with ten years of service credit, most members are also eligible for a non-job-related disability benefit.

In addition, most PFRS employers offer their employees special retirement plans. A special plan lets members retire after completing 20 or 25 years of credited service in specific job titles rather than reaching a certain age. Most firefighters — and, in fact, nearly 80 percent of all PFRS members (25,784) — are enrolled in a set of special 20- and 25-year plans. Whether members need 20 or 25 years depends on their retirement plan.

Just like starting your first job, getting married or having kids, retirement will change your life. Some changes are small, like sleeping in or shopping during regular business hours. Others, however, are significant and worth examining ahead of time… like how much you’ll be spending in retirement each month or each year.

An Employee Benefit Research Institute (EBRI) study offers some good news for prospective retirees. Household spending generally drops at the beginning of retirement — by 5.5 percent in the first two years, and by 12.5 percent in the third and fourth years. (Although, nearly 46 percent of households actually spend more in the first two years of retirement.)

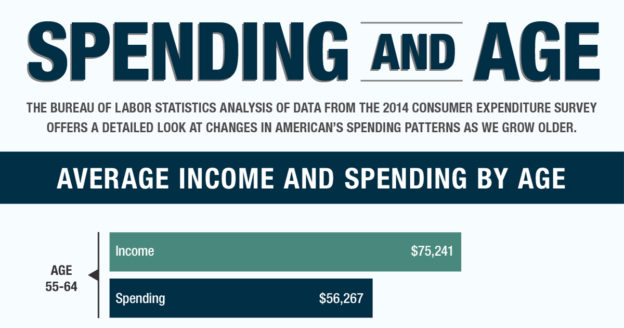

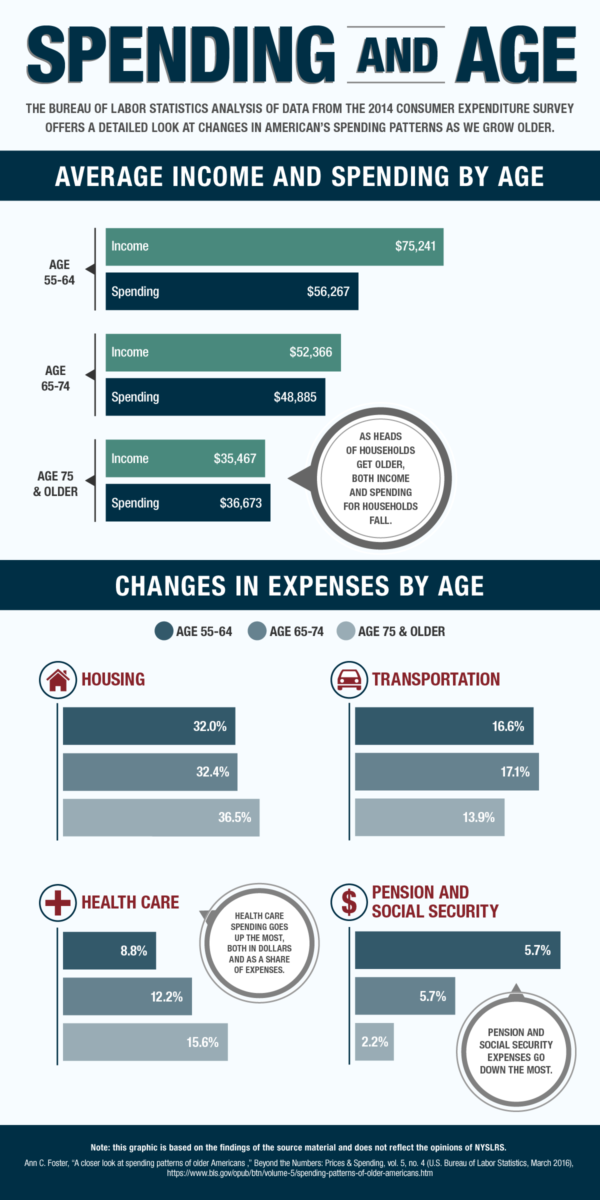

Analysis from the Bureau of Labor Statistics in the U.S. Department of Labor seems to support the research from EBRI. In “A closer look at spending patterns of older Americans,” the author analyzed data from the 2014 Consumer Expenditure Survey, and she also found a progressive drop in spending as age increases. (Income declines with age as well.)

While data supporting EBRI’s study is helpful, it turns out that the highlight of the Consumer Expenditure Survey results is a detailed look at how the things we spend our money on change as we grow older.

As interesting as that is, it’s just a general look at how older Americans are managing their money. What really matters is: How will you spend your money once you retire?

Prepare a Post-Retirement Budget

Like a fiduciary choir, financial advisors all sing the same refrain: Start young; save and invest regularly to meet your financial goals. If you do, the switch from saving to spending in retirement can be easy.

But, in order to make that transition, you need a budget.

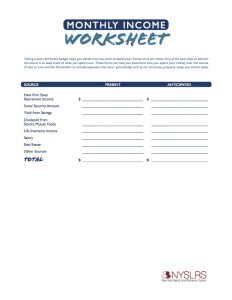

The first step toward a post-retirement budget is a review of what you spend now. For a few months, track how you spend your money. Don’t forget to include periodic costs, like car insurance payments or property taxes. By looking at your current spending patterns, you can get an idea of how you’ll spend money come retirement.

Then, consider your current monthly income, and estimate your post-retirement income. If your post-retirement income is less than your current income, you might want to plan to adjust your expenses or even consider changing your retirement date.

We have monthly expense and income worksheets to help with this exercise. You can print them out and start planning ahead for post-retirement spending.

Monthly Worksheets (PDF)

For those of you who carry smart phones, Forbes put together a list of popular apps for tracking your daily spending. All of them are free, though some do sell extra features. Many of them can automatically pull in information from your bank and credit card accounts, but if you’d rather avoid that exposure or if you use cash regularly, you may prefer an app that lets users enter transactions manually.

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called

If you have tax-deferred retirement savings (such as certain 457(b) plans offered by NYS Deferred Comp), you will eventually have to start withdrawing that money. After you turn 70½, you’ll be subject to a federal law requiring that you withdraw a certain amount from your account each year. If you don’t make the required withdrawals, called