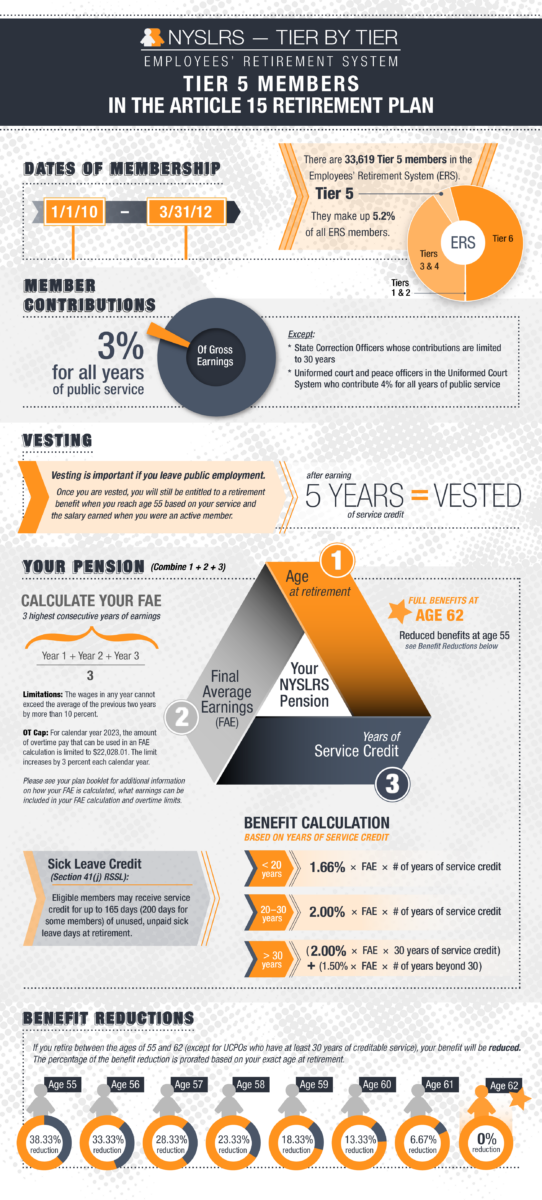

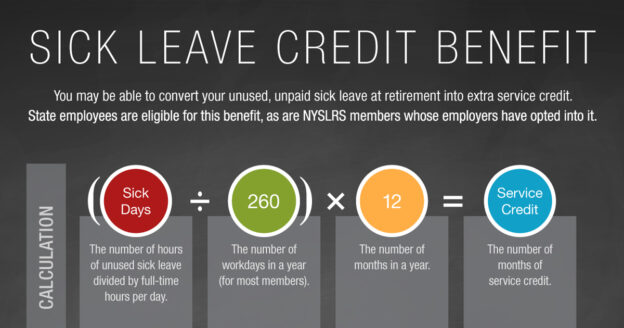

If you retire with unused, unpaid sick leave, you may be able to use it toward your NYSLRS pension.

- Most eligible ERS Tier 2, 3, 4 and 5 members can receive credit for up to 165 days (7.5 months).

- Most eligible ERS Tier 6 members can receive credit for up to 100 days (4.5 months).

- Most eligible PFRS members can receive credit for up to 165 days (7.5 months).

- State employees in certain negotiating units can receive credit for up to 200 days (approximately 9 months).

Eligibility for the Sick Leave Benefit

To be eligible for the Sick Leave Benefit, your employer must have adopted the following section of the Retirement and Social Security Law (RSSL):

- Section 41(j) of the RSSL for ERS members.

- Section 341(j) of the RSSL for PFRS members.

To check if this benefit is available to you, ask your employer or:

- Sign in to Retirement Online.

- Look under My Account Summary.

- Then, look for Sick Leave Eligibility.

How the Sick Leave Benefit Works

To receive this benefit, you must retire directly from public service or within a year of leaving. The additional service credit for your unused, unpaid sick leave, up to a certain limit, will be added to your total years of service when calculating your pension benefit. However, it cannot be used to:

- Qualify for vesting. For example, if you have four years and ten months of service credit and you need five years to be vested, your sick leave credit cannot be used to reach the five years.

- Qualify for a better retirement benefit calculation. For example, if you have 19 ½ years of service credit but your pension calculation will improve substantially if you have 20 years, your sick leave credit cannot be used to reach the 20-year calculation.

- Meet the service credit requirement for a special 20- or 25-year plan.

- Increase your pension beyond the maximum allowed under your retirement plan.

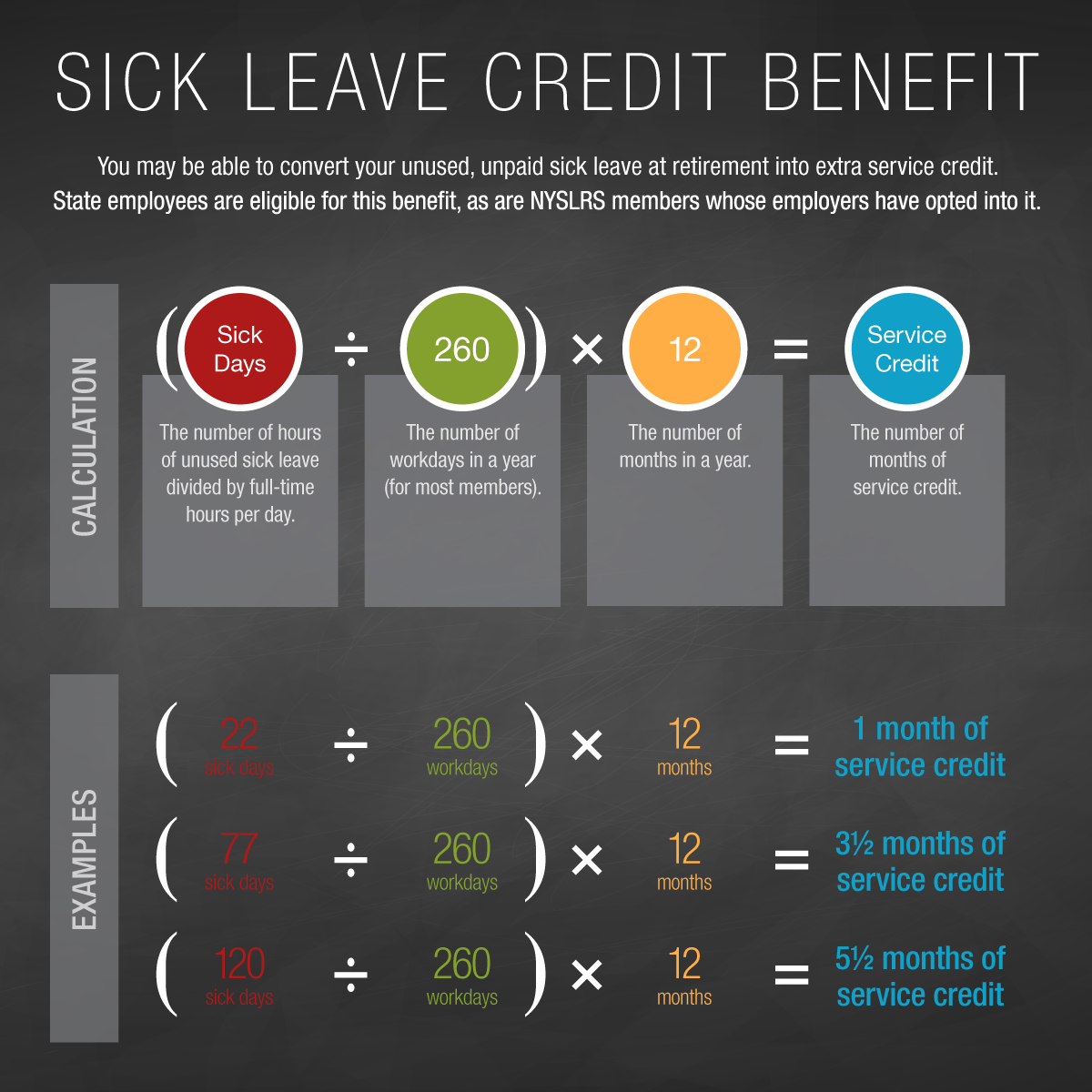

The additional service credit is based on your total hours of unused, unpaid sick leave and the number of hours in your employer’s standard workday.

For More Information

For comprehensive information about your retirement benefits and how your pension will be calculated, find your retirement plan publication. And as you approach retirement, read our Preparing for Retirement blog post for guidance, including topics to consider and actions to take as you plan.