Get Your Member Annual Statement Sooner and Help Us ‘Go Green’

You can get access to your Member Annual Statement sooner than printed copies are mailed by updating your delivery preference to email. When you choose to get your Statement online, it’ll save you time—and it’ll help us ‘go green’ by reducing paper waste.

Click update next to ‘Member Annual Statement by.’

Choose Email from dropdown.

Be sure the email address listed in your Retirement Online profile is current.

When your Statement is available, we’ll send an email notifying you to sign in to Retirement Online.

Note: If you choose email as your delivery preference, you will not receive a printed copy in the mail.

Update Your Contact Information

We distribute Member Annual Statements based on the mailing or email address we have on file, so you should make sure your information is current. Retirement Online is the fastest and most convenient way to review your contact information and update it if needed.

Click update next to mailing address, email address or phone number.

If you don’t already have an email address on file, please provide it so we contact you quickly with important information, such as a change to your benefits. Use a personal email address you will have access to after you retire, not a work email address.

If you don’t have an account or for help signing in to an existing account, check out our Retirement Online Tools and Tips blog post where you’ll find information to help you register, reset your password, unlock your account and more.

When you register for an account, you will be asked to identify yourself, confirm your Social Security number and verify your identity for security reasons. Then, you’ll be prompted to create your user ID and password following the guidelines shown. These requirements will help you create a password that won’t be easily guessed or broken, but the Social Security Administration offers some additional helpful tips, including:

Instead of just random characters, use longer, easy to remember phrases in your password.

Use different passwords for each account so a single stolen password doesn’t compromise multiple accounts.

Don’t use personal information like your birthday or a pet’s name in your password.

Select Security Questions and Remember Your Answers

After you sign in for the first time, you’ll need to choose security questions and submit answers. Make sure you remember your responses—you’ll need to answer these questions again if you forget your user ID, need to reset your password or get locked out of your account.

If you forget your login credentials, you can look up your user ID or reset your password. You’ll need to identify yourself and answer the security questions you set when you signed in for the first time.

To look up your user ID, click the Forgot ID link above the User ID field on the login page. For step-by-step instructions, read our Forgot User ID guide.

To reset your password, click the Forgot Password link above the Password field on the login page. For step-by-step instructions, read our Forgot Password guide.

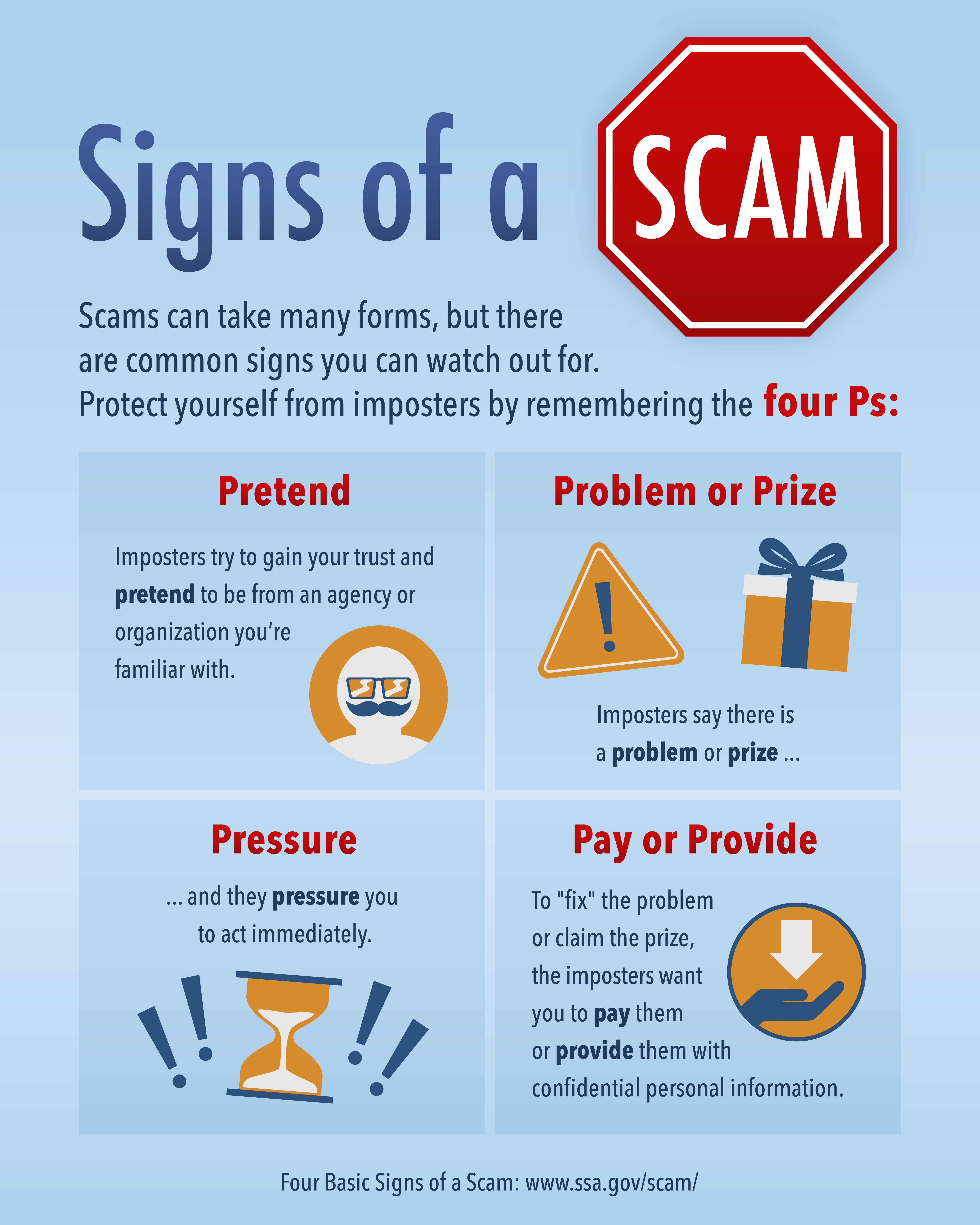

Your retirement account can be an attractive target for scammers who continue to find new ways to try to impersonate government agencies, such as NYSLRS or the Social Security Administration. Protect yourself from scams by learning to distinguish fake messages from official NYSLRS communications.

How Scams Work

Scammers pretend to be an agency or organization you already know to gain your trust. They use similar logos or imagery in correspondence. They may contact you from an email address that mimics—but isn’t identical to—those used by employees of the actual organization. Some can even make a real agency’s phone number appear on caller ID (known as spoofing).

Usually, once they contact you, they claim there is a problem (or a prize or a new benefit available) requiring your immediate attention. But here’s the catch: to fix the problem or receive the reward, the imposter needs you to pay them a fee or provide personal data, such as your Social Security number or bank account information. They may even threaten you with legal action, a suspension of your benefits or arrest if you fail to act.

If someone contacts you and you notice these signs of a scam, remain calm. Hang up the phone or delete the message if you feel like something is off. It’s the easiest way to avoid accidentally giving away personal information.

Scammers have also attempted to create a fake mobile app or website, which looks similar to Retirement Online, aimed to trick users and capture login credentials. Please be aware, we currently do not have a mobile app. Protect yourself from these scams by accessing Retirement Online from the NYSLRS website and avoid using search engines to find a link for the login page.

AI: A New Tool for Scams

You should also be aware of an emerging threat—artificial intelligence (AI), which allows computers to mimic certain human behaviors, such as speech and writing. Using AI, scammers can personalize phishing emails, making it harder to recognize a fraudulent communication. AI may even be able to impersonate the voice of a family member or friend, making you think they are in trouble or need money.

Here are some things you can do to protect yourself from AI-enhanced scams.

Don’t share sensitive information through text or social media.

Don’t send or transfer money to unknown locations.

Consider designating a safe word for your family to use to identify themselves and share that word with family members and close contacts.

When in doubt, hang up and call your loved one back.

Doing Business With NYSLRS

To protect yourself from potential scams and keep your personal information secure, use your NYSLRS ID to verify your identify when doing business with NYSLRS, instead of providing your Social Security number. You can find your NYSLRS ID by signing in to your Retirement Online account, or by checking your annual statement or other correspondence from NYSLRS.

Generally, NYSLRS will only call you if we are following up on a previous communication from you—a phone call, secure email message, Retirement Online request, form or letter. If you haven’t completed a transaction or submitted changes recently, be wary of unexpected calls or requests for your NYSLRS information.

Make sure you review the communications you receive from NYSLRS. We send you letters or emails (depending on your delivery preference in Retirement Online) whenever you update your Retirement Online account or benefit information. If you receive a letter or email about an account change you did not make, contact us immediately.

Keep Your Retirement Online Account Secure

Retirement Online is the fastest and most convenient way to access your retirement account information and conduct business with NYSLRS. And it’s safe to use—it has the same security safeguards used for online banking and by other financial institutions. Here are steps you can take to help ensure your Retirement Online account stays secure:

Once you have an account, keep your username and password in a safe place, and don’t share them with anyone. NYSLRS will never ask for your password.

Sign in to Retirement Online at least once a year and update your password so it doesn’t expire. If you forgot your user ID or password, don’t worry—from the customer login page, you can:

Click the Forgot ID link to look up your user ID.

Click the Forgot Password link to reset your password.

You’ll need to identify yourself and answer security questions you set when you signed in for the first time.

Update your delivery preference to receive an email notifying you when you have correspondence to view in Retirement Online. That way, when there are changes to your account, you’ll receive an email notifying you instead of waiting for printed notices through the mail.

Most NYSLRS members can create their own pension estimates in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit. When you’re done, print your pension estimate or save it for future reference.

Remember, the amounts are estimates, not a guarantee of what you’ll receive when you retire.

Most Tier 2 through 6 members (more than 90 percent of all NYSLRS members) can use the Retirement Online pension calculator. However, some members may not be able to—for example, members who recently transferred to NYSLRS and some PFRS members. The system will let you know if your estimate cannot be completed. In that case, please send us a message using our secure contact form (select Estimates from the Topic dropdown).

Do More With Retirement Online

In Retirement Online, you can view your account details—date of membership, tier, retirement plan, estimated total service credit and more. Check out what else members can do in Retirement Online.

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring.

It’s important to name beneficiaries and review them periodically. Life circumstances change and a beneficiary you named before might not be one you would choose today. For instance, you may have a new partner or you may have children now. And NYSLRS can only pay a death benefit to the beneficiaries you’ve named.

Your primary beneficiary will receive your death benefit. You can list more than one primary beneficiary. If you do, they will share the benefit equally. Or, you can choose different percentages for each beneficiary, which must total 100 percent. (Example: John Doe, 50 percent; Jane Doe, 25 percent; and Mary Doe, 25 percent.)

A contingent beneficiary will only receive a benefit if all your primary beneficiaries die before you do. If you list multiple contingent beneficiaries, they will share the benefit equally unless you choose different percentages.

Special Beneficiary Designations

Your beneficiary doesn’t have to be a person. You can name your estate, a trust or a charity as your beneficiary.

Estate. When you die, your estate is the money and property you owned. Your death benefit will be given to the executor of your estate to be distributed according to the terms of your will. You can name your estate as the primary or contingent beneficiary of your death benefit. If you name your estate as the primary beneficiary, do not name a contingent beneficiary.

Trust. You can name a trust as a primary or contingent beneficiary if you have a trust agreement or provided for a trust in your will. The trust itself would be your beneficiary, not the individuals for whom you established the trust. (Speak with your attorney if you’re thinking about making your trust a beneficiary.)

Entity. You can also name any charitable, civic, religious, educational or health-related organization as a beneficiary.

Minor children. If your beneficiary is under the age of 18 at the time of your death, your benefit will be paid to the child’s court-appointed guardian. You may instead choose a custodian to receive the benefit on the child’s behalf under the Uniform Transfers to Minors Act (UTMA). Custodians can be designated in Retirement Online, or you can contact us for more information and the appropriate form before making this type of designation.

Keep Your Beneficiaries Up to Date with Retirement Online

You can change your beneficiaries at any time. In addition to adding or removing them to reflect your current wishes, you should review the contact information for your named beneficiaries so we can find them when needed.

The fastest way to view or update your beneficiaries is in Retirement Online.

When it comes to managing your NYSLRS account, Retirement Online is the fastest way to do it. Skip printing forms, having them notarized and sending them through the mail. When you submit your requests online, NYSLRS has them immediately, and your changes will be completed more quickly. It’s convenient, and it’s secure.

Get Email Notifications for Important Documents and Help Us ‘Go Green’

You can help us ‘go green’ and reduce paper waste by choosing email as your delivery preference for correspondence and other important documents. When you have something to view, we’ll send an email notifying you to sign in to Retirement Online. And it’ll save time—you’ll get access to your important documents sooner than printed copies are mailed.

To update your delivery preferences:

Look under My Profile Information.

Click update next to ‘Contact by’ or ‘Member Annual Statement by.’

Choose Email from dropdown.

Be sure the email address listed in your profile is current.

If you choose email as your delivery preference, you will not receive a printed copy in the mail.

Update Your Contact Information

It’s important we have your current contact information so you receive the news, correspondence and statements we send you.

To update your contact information:

Look under My Profile Information.

Click update next to email address, mailing address or phone number.

If you don’t already have an email address on file, please provide it so we can contact you quickly with important information, such as a change to your benefits. Use a personal email address you will have access to before and after you retire, not a work email address.

Manage Your Beneficiaries

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring. It’s a good idea to review your beneficiaries from time to time to make sure they reflect your current wishes. The beneficiary you named before might not be the one you would choose today. You should also review the contact information for your named beneficiaries so we can find them when needed.

To add or remove beneficiaries or update their contact information:

Look under My Account Summary.

Click View and Update My Beneficiaries button.

Estimate Your Pension

How much will your pension be? It’s an important question as you plan for retirement. In just a few steps, most members can use Retirement Online to estimate their pension based on the most up-to-date account information we have on file, then save or print the estimate. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit and help you choose the retirement date that’s right for you.

Look under My Account Summary.

Click Estimate My Pension Benefit button.

Apply for a Loan and Manage Loan Payments

The fastest way to apply for a loan is in Retirement Online. You can see how much you are eligible to borrow, what the repayment amount would be and whether your loan will be taxable—all before you apply.

Look under My Account Summary.

Click Apply for a Loan button.

If you have an existing loan, you can check your current loan balance and adjust your payment amount or make an additional one-time payment.

Look under My Account Summary.

Click Manage My Loans button.

Request Additional Service Credit

You may be able to request additional service credit if you worked for a participating employer before joining NYSLRS, worked for a public employer that later participated in NYSLRS, or served in the U.S. Armed Forces. In most cases, you have to pay for additional service credit. But because service credit is a factor in the calculation of your retirement benefits, purchasing additional service credit will usually increase your pension. You must submit your request before retirement, and you should do it as early in your career as possible—the sooner you purchase your credit, the less it will generally cost.

To submit your request online:

Look under My Account Summary.

Click Manage My Service Credit Purchases button.

Click Request Additional Service Credit link.

Get Your Member Annual Statement

Your Member Annual Statement is a valuable snapshot of your NYSLRS membership and benefits as of March 31, the end of the state fiscal year. You can access Statements dating back to 2020 online.

Look under My Account Summary.

Click View MyMember Annual Statement button.

Statements are made available online each year in early May, sooner than printed copies are mailed—update your delivery preference to get notified.

Generate a Mortgage Verification Letter

If you are applying for a mortgage and need a summary of your NYSLRS account information, you can quickly generate a mortgage verification letter online. The document will show your contribution balance, the date and amount of your last loan, and if you have an existing loan, the current balance, the payroll deduction amount and the interest rate.

Look under I want to… (located at the top right).

Click Generate Mortgage Verification Letter link.

Apply for Retirement

When you are ready to retire, avoid the hassle of paper forms and apply online. You’ll be able to see an estimate of your pension, select your payment option, enter federal tax withholding information, sign up for direct deposit, submit required documents and much more. Learn more about the advantages and how to apply for retirement in Retirement Online.

If you leave public employment with less than ten years of service credit, you can withdraw your membership online and request a refund of your contributions. However, this will end your NYSLRS membership. Before you submit a withdrawal application, we recommend speaking with a customer service representative by sending a message using our secure contact form.

Your Retiree Annual Statement provides a year-end summary of your pension payments for the last calendar year, including the total amount you received and a breakdown of credits, deductions and taxes. It also gives you an explanation of the pension payment option you chose at retirement.

We mail printed Retiree Annual Statements by the end of February. However, we make Statements available in Retirement Online sooner than printed copies are mailed—and you can sign in to your account now to access yours.

If Retirement System is blank, click Look Up icon and select ERS or PFRS from dialog box.

Click Look Up icon next to Calendar Year field and select an option from dialog box.

Click Generate Statement.

The document will download on to your computer.

If you don’t have an account, check out our Retirement Online Tools and Tips blog post where you’ll find a link to step-by-step instructions to help you register for Retirement Online.

Understanding Your Retiree Annual Statement

Your annual Statement provides year-end benefit and payment information for the previous calendar year, including:

Your total pension benefit amount before credits, deductions and taxes.

Credits for adjustments or reimbursements, such as a cost-of-living adjustment (COLA) or Medicare reimbursements. (Only applicable credits appear in your Statement.)

Deductions for recoveries, payments to an alternate payee, health insurance, or other dues or fees you’ve authorized to have deducted from your pension benefit. (Only applicable deductions appear in your Statement.)

The amount withheld for federal taxes.

Your total net benefit after credits, deductions and taxes.

If you have questions about the information and terms used in your Statement, check out our Guide to Your Statement for a short explanation of each.

Do Not Use Your Statement for Tax Purposes

While your Retiree Annual Statement includes pension payment and tax information, it is not a tax document. If your pension is taxable, we provide a 1099-R tax form (either through Retirement Online or by mail, depending on your delivery preference) for filing your taxes.

View Your Pension Pay Stub for Year-to-Date Information

Your pay stub gives you valuable insight into your monthly pension payment, including a breakdown of credits, deductions and taxes. Throughout the year, you can access your pay stubs online to see year-to-date totals.

From Account Homepage, click View Pension Check link.

Select date of the pension payment to view.

Get an Email Notification for Your Statement

Next year, you can get access to your Statement sooner by updating your delivery preference to email. When your Statement is available, we’ll send an email notifying you to sign in to Retirement Online.

Tax season is here. While your NYSLRS pension is not subject to New York State or local income tax, most NYSLRS pensions are subject to federal income tax. Each year, we provide a 1099-R tax form with the information you need to file your taxes.

We mail printed 1099-Rs by January 31. However, we make 1099-Rs available in Retirement Online sooner than printed copies are mailed—and you can sign in to your account now to access yours.

Select 2024 from Year dropdown. (Note: 2024 and 2023 are currently available online.)

Click Generate button.

If you have one tax form, the document will open in a new browser tab. If you have more than one tax form, the documents will download to your computer.

Please check your browser settings and disable pop-up blockers to ensure your tax form is generated. By default, your browser may block pop-ups, which could prevent a new tab from opening or the file from downloading.

If you don’t have a Retirement Online account, check out our Retirement Online Tools and Tips blog post, where you’ll find a link to step-by-step instructions to help you register.

Understanding Your 1099-R

Your tax form includes:

The total benefit paid to you in a calendar year.

The taxable amount of your benefit.

The amount of taxes withheld from your benefit.

If you have questions about the information on your tax form, check our interactive 1099-R tutorial. It walks you through a sample and offers a short explanation of each box on the form.

Get an Email Notification for Your 1099-R

Next year, you can get access to your tax form sooner by updating your delivery preference to email. When your 1099-R is available, we’ll send an email notifying you to sign in to Retirement Online.

As a NYSLRS retiree, you can work and still receive your pension. However, there may be a limit on how much you can earn each year without affecting your NYSLRS pension.

Working While Receiving a Service Retirement Benefit

Generally, an earnings limit of $35,000 applies to NYSLRS retirees who:

Are under age 65;

Receive a service retirement benefit (see disability benefit rules below); and

Return to work for a public employer (including contract or consultant work, if you joined NYSLRS on or after May 31, 1973).

There is no earnings limit if you are self-employed or if you work for:

The federal government;

A state or local government in another state; or

A private employer.

Also, beginning in the calendar year you turn 65, the earnings limit no longer applies.

Update Regarding the Earnings Limit

The earnings limit for retirees employed by school districts or Boards of Cooperative Educational Services (BOCES) is suspended through June 30, 2025. (April 2024 legislation extended the date from 2024 to 2025.) This earnings limit suspension does not apply to retirees who work for a college, university or charter school.

For most other retirees under the age of 65, the $35,000 limit is in effect and applies to the entire calendar year in 2025.

NYSLRS retirees can return to work part-time for a public employer. However, a retiree must have had a “bona fide” termination of employment. This means the retiree was removed from their employer’s payroll before the effective date of their retirement, and the member and their employer had no expectation of further work after the retirement date. If these conditions are not met, the retiree’s service retirement can be voided and pension payments received will be recovered by NYSLRS.

Working While Receiving a Disability Retirement Benefit

Almost all earnings for retirees who are working while receiving a disability retirement benefit are limited whether they work for a public or private employer. The limit is specific to each retiree. To find out your earnings limit, please contact us.

How the Earnings Limit Applies

The limit applies to all earnings for the calendar year, including money earned in the calendar year, but paid in a different calendar year (for example earned in December but paid in January).

The limit does not apply to:

Payments received after you retire from your employer, such as for vacation or sick time you earned when you were still working; and/or

A retroactive payment for a new union contract, if the earnings are for employment before you retired.

Reporting Your Earnings

It is your responsibility to notify NYSLRS if you earn more than the limit. If you know you are going to exceed the limit, contact us at least a month before you do.

You can message us using the secure contact form, or you can fax a letter to 518-402-2498. Be sure to include the name of your employer, the approximate date you expect to exceed the limit and a daytime phone number in case we have questions.

If You Exceed the Earnings Limit

If you earn more than the limit, you must:

Pay back NYSLRS for the pension payments you received after the date you reached the limit. If you continue to work, your pension will be suspended for the remainder of the calendar year and resume the following January.

OR

Rejoin NYSLRS, in which case your pension will be suspended until you retire again at some future date. (You’d need to reapply.)

Earnings Limit Waiver

Under Section 211 of the Retirement and Social Security Law, the earnings limit can be waived if your prospective employer gets approval before hiring you. Approval is not automatic; it is based on the employer’s needs and your qualifications. In most cases, the New York State Department of Civil Service would be the approving agency. A Section 211 waiver covers a fixed period, normally up to two years.

For More Information

Before you decide to return to work, please read our publication What If I Work After Retirement? It includes information such as how earnings limits are calculated for retirees receiving a disability retirement benefit, consequences to consider before returning to NYSLRS membership and more. If you have questions, please contact us.

Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement. As a NYSLRS member, your plan for income in retirement likely includes your NYSLRS pension and Social Security benefits. However, for greater financial stability and flexibility, you may want to supplement with retirement savings. For example, you might start investing in a savings plan like the New York State Deferred Compensation Plan (NYSDCP).

What is Deferred Compensation?

Deferred compensation plans are voluntary retirement savings plans like 401(k) or 403(b) plans—but designed and managed with public employees in mind. NYSDCP is the 457(b) plan created for New York State employees and employees of other participating public employers in New York.

Just like with other retirement savings plans, you have options for how you make your NYSDCP contributions. You might choose a tax-deferred account where you make contributions with pre-tax money. With this option, you won’t pay State or federal taxes on the earnings you contribute until you start making withdrawals. Your employer may also offer the option for a Roth account where you make contributions with after-tax money. With this option, you do pay taxes now, but you won’t pay taxes on the withdrawals you make in retirement. Learn more about how traditional retirement savings and Roth accounts compare.

If your employer is not an NYSDCP participating employer, check with your human resources or personnel office about other retirement savings options.

What Does Deferred Compensation Mean for Me?

Deferring income from your take-home pay may mean less money to spend in the short-term, but you’re planning ahead for your financial future.

Tax season is here. While your NYSLRS pension is not subject to New York State or local income tax, most NYSLRS pensions are subject to federal income tax. Each year, we provide a 1099-R tax form with the information you need to file your taxes.

Tax season is here. While your NYSLRS pension is not subject to New York State or local income tax, most NYSLRS pensions are subject to federal income tax. Each year, we provide a 1099-R tax form with the information you need to file your taxes.