When you joined the New York State and Local Retirement System (NYSLRS), you were assigned to a tier based on the date of your membership. There are six tiers in the Employees’ Retirement System (ERS) and five in the Police and Fire Retirement System (PFRS) — so there are many different ways to determine benefits for our members. Our series, NYSLRS – One Tier at a Time, walks through each tier and gives you a quick look at the benefits members are eligible for before and at retirement.

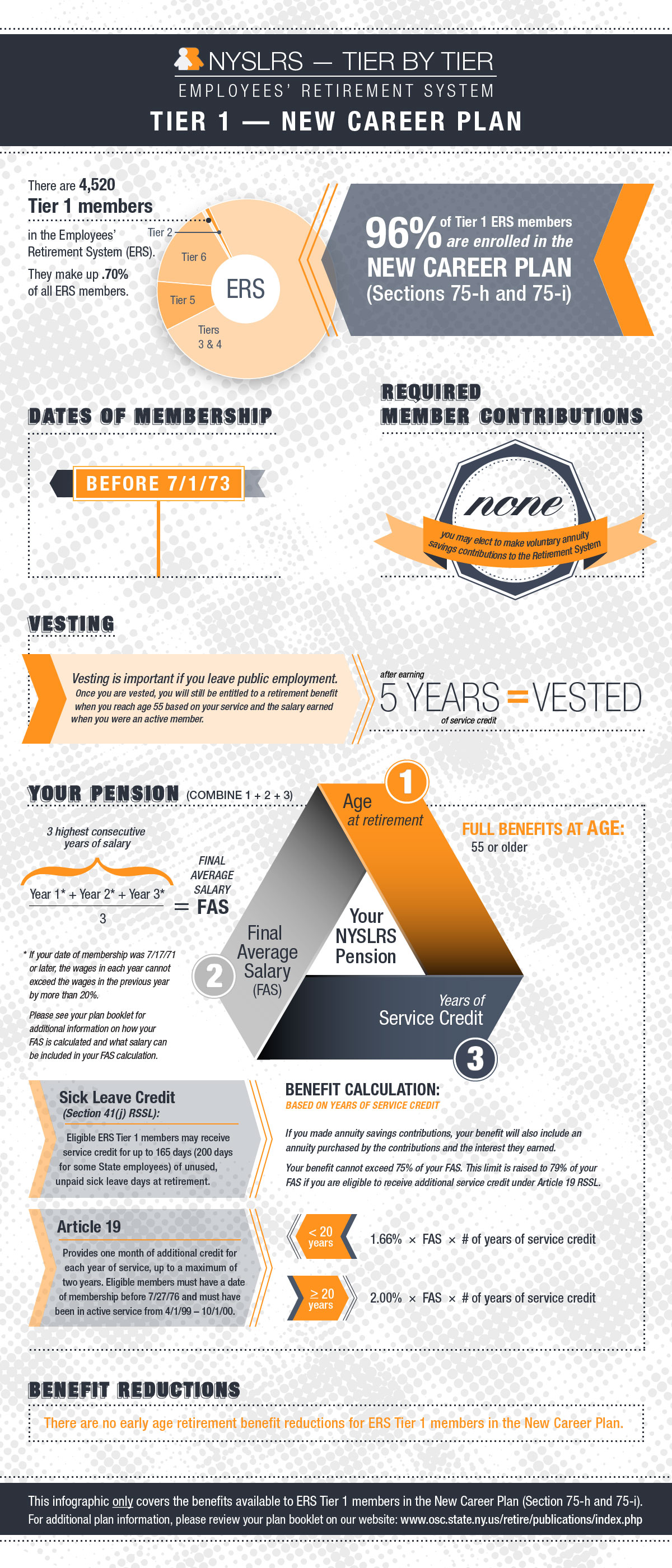

One of our smallest tiers is ERS Tier 1, which represents 0.7 percent of NYSLRS’ total membership. Overall, there are 4,520 ERS Tier 1 members. Today’s post looks at the major Tier 1 retirement plan in ERS – the New Career Plan (Section 75-h or 75-i).

If you’re an ERS Tier 1 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

- New Career Plan for ERS Tier 1 Members (VO1504)

- Career Plan for ERS Tier 1 Members (VO1503)

- State Correction Officers and Security Hospital Treatment Assistants Plan for ERS Tier 1 Members (VO1525)

- Sheriffs, Undersheriffs and Deputy Sheriffs Special Plan for ERS Tier 1 Members (VO1840)

- Legislative and Executive Retirement Plan for Tier 1 Members (VO1861)

- Non-Contributory Plan With Guaranteed Benefits for ERS Tier 1 Members (ZO1502)

- Non-Contributory Plan for ERS Tier 1 Members (ZO1501)

- Basic Plan for ERS Tier 1 Members (ZO1500)

Be on the lookout for more NYSLRS – One Tier at a Time posts. Want to learn more about the different NYSLRS retirement tiers? Check out some earlier posts in the series:

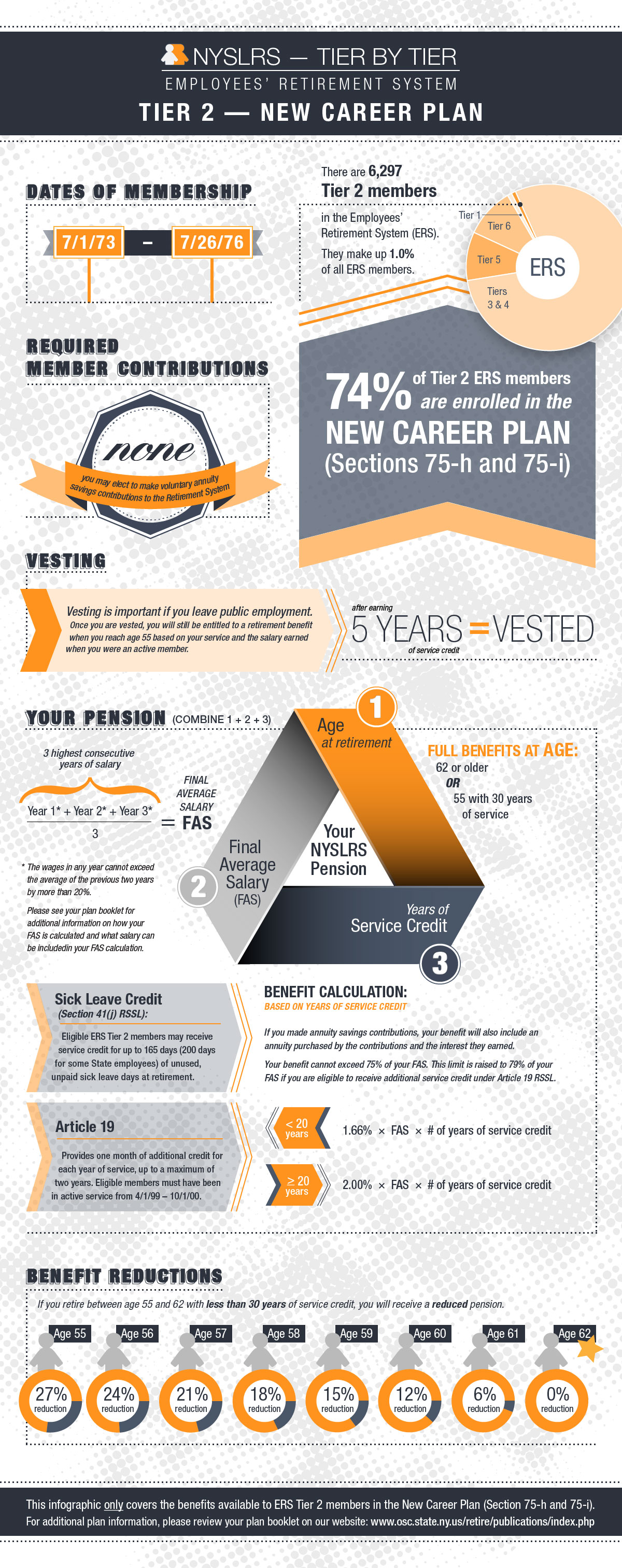

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits:

If you’re an ERS Tier 2 member in an alternate plan, you can find your retirement plan publication below for more detailed information about your benefits: