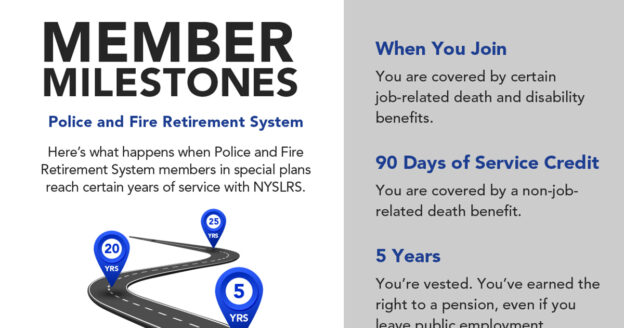

The Police and Fire Retirement System (PFRS) covers nearly 32,000 police officers and firefighters across New York State. As a PFRS member, you’ll pass a series of important milestones throughout your career. Knowing and understanding these milestones will help you better plan for your financial future.

Some milestones are common to most PFRS members; others are shared by members in a particular tier or retirement plan. For example, your plan determines when you would be eligible to apply for a non-job-related disability benefit.

A recent amendment to Retirement law changed a milestone for some members. As of April 9, 2022, Tier 5 and 6 members are now vested after earning five years of service credit. Previously, members in these tiers needed ten years of service to become vested. Being vested means you are entitled to a NYSLRS pension, even if you leave public employment before retirement age.

Member Milestones to Remember

Most PFRS members are in special plans that allow them to retire with full benefits, regardless of age, after 20 or 25 years of service. If you are in a special plan, only certain job titles would give you creditable service toward a 20- or 25-year milestone. For example, if you are in the State Police plan, service with a city police department would be creditable, but service as a sheriff’s deputy or corrections officer would not be.

PFRS members in regular plans can retire as early as age 55, but may face a benefit reduction if they retire before their full retirement age.

Your specific milestones, along with your pension calculation, are determined by your retirement plan, so it is important to familiarize yourself with the details of your plan. You can find information about your milestones in your retirement plan booklet on our Publications page. Not sure which retirement booklet is yours? Your retirement plan is listed in your Retirement Online account or you can ask your employer. You can also read our recent blog post for tips on finding your plan booklet.

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

Let’s say you work as a firefighter, so you’re a member of PFRS. You decide to take on a part-time job as a bus driver for your local school district. Your school district participates in ERS, so you’re eligible for ERS membership. You fill out the membership application, and now you’re a member of both ERS and PFRS. The date you join each system determines

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.

manages more than 300 retirement plan combinations for its members, which are described in more than 50 plan booklets. But, for all that complexity, they breakdown into just two main types: regular plans and special plans. Under a regular plan, you need to reach certain age and service requirements to receive a pension. For instance, if you’re a Tier 4 member in the Employees’ Retirement System (ERS) with a regular plan, you’re eligible for a benefit when you turn 55 and have five or more years of service credit. Most of our ERS members are in regular plans.