NYSLRS provides pension benefits to more than 520,000 retirees and beneficiaries. You can find our retirees in every state in the US and in countries all around the world. However, most live right here in New York State.

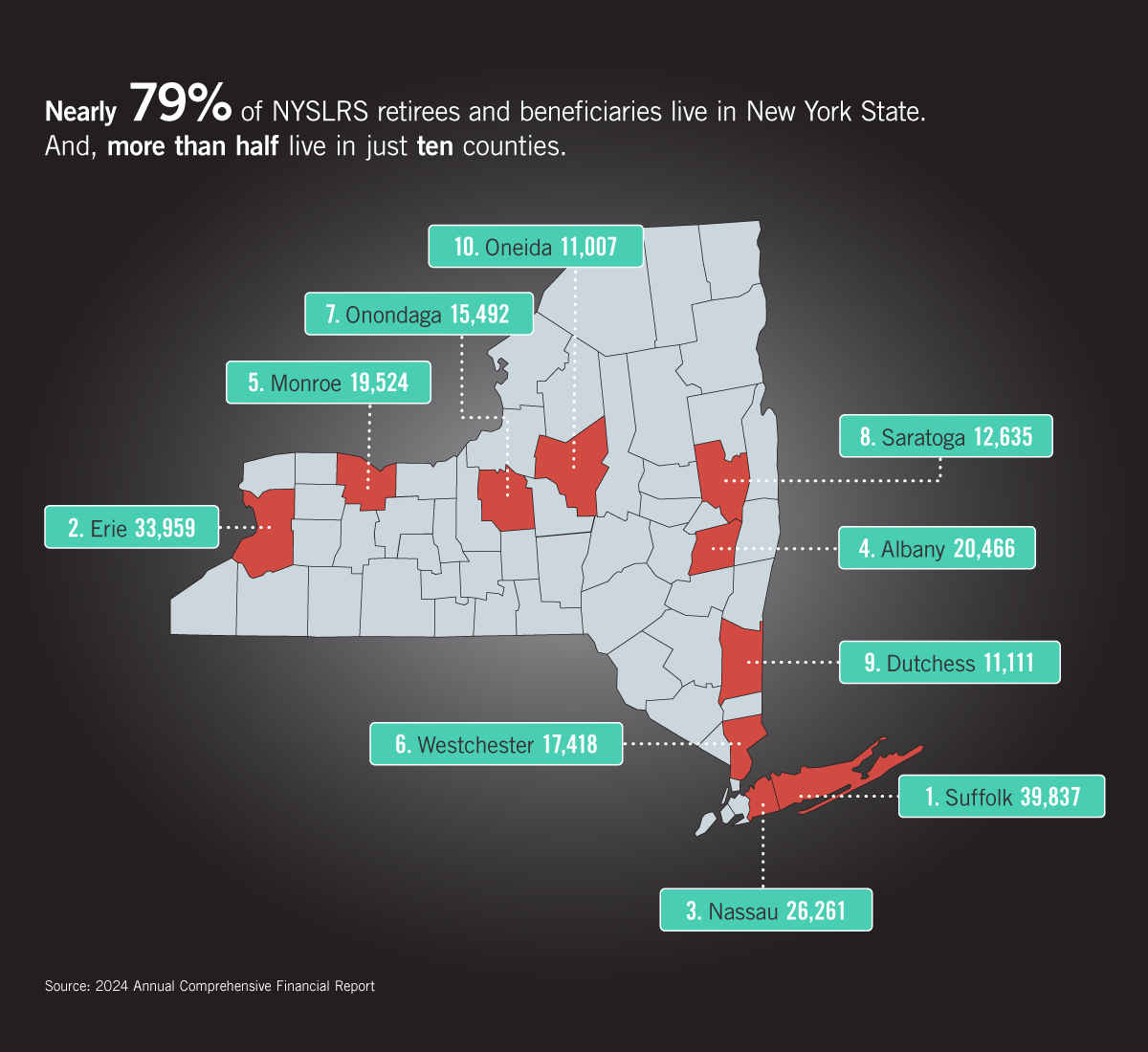

Nearly 79% of NYSLRS Retirees Stay in New York

The vast majority of NYSLRS retirees—nearly 79 percent—stay in New York State, and their pension dollars flow right back into our communities. Retirees in New York pay local property and sales taxes. Their spending supports local businesses, generates thousands of jobs and stimulates the economy.

Where in New York do these retirees call home?

Long Island is home to more than 66,000 retirees and beneficiaries. Suffolk County has the most and Nassau County has the third most benefit recipients of the counties outside of New York City. (The City, which has its own separate retirement systems for municipal employees, police and firefighters, has more than 24,000 retirees and beneficiaries.)

Erie County, which includes Buffalo, has the second most retirees—nearly 34,000. Albany County, home to the State capitol, is ranked fourth, with more than 20,000. Monroe, Westchester, Onondaga, Saratoga, Dutchess and Oneida Counties round out the top ten.

All told, retirees and beneficiaries in the top ten counties received $7 billion in retirement benefits in the fiscal year ending March 31, 2024.

Hamilton County has the fewest retirees. But, in this sparsely populated county in the heart of the Adirondacks, those 545 retirees represent about 10 percent of the county’s population and received $12.9 million in retirement benefits in the fiscal year ending March 31, 2024.

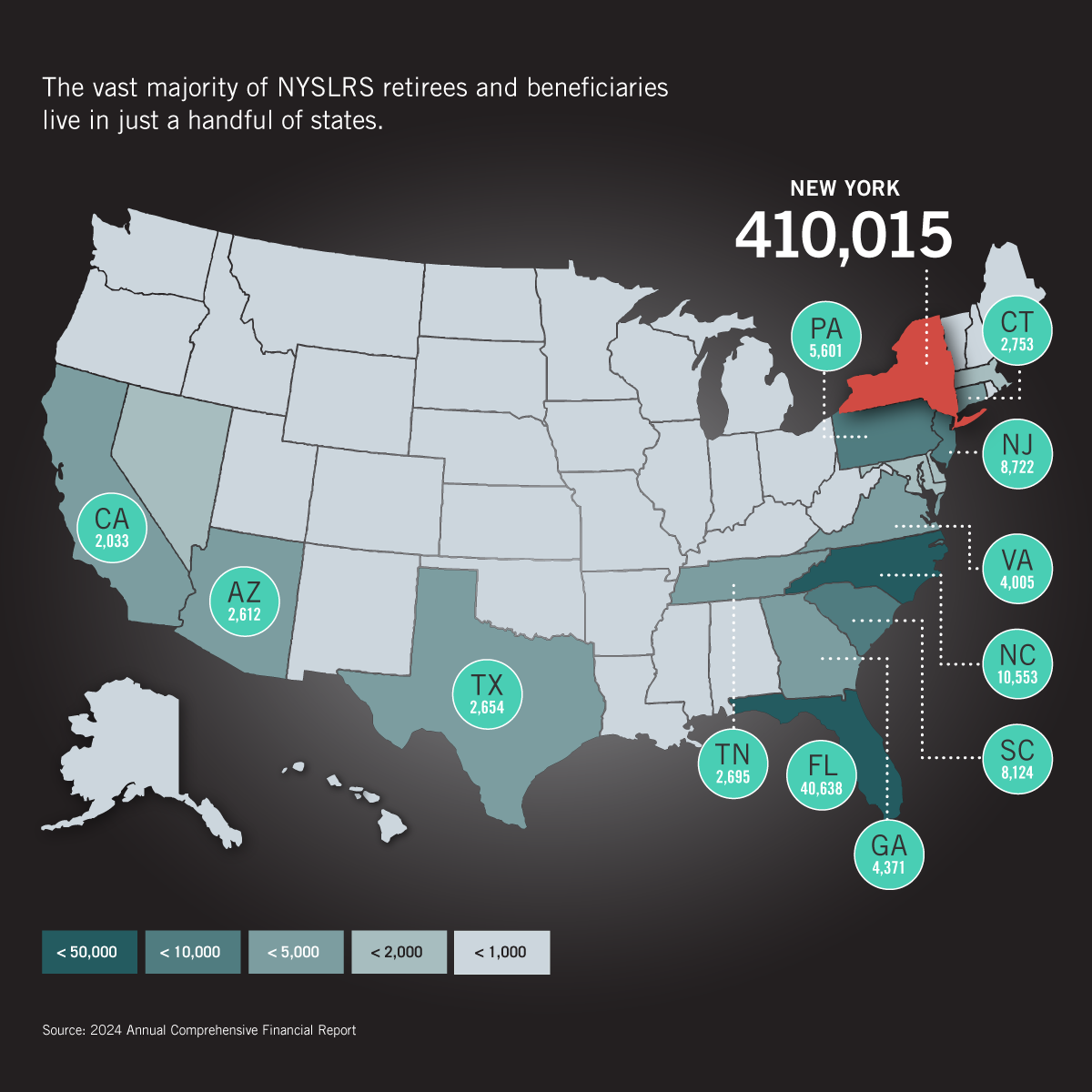

NYSLRS Retirees in the United States

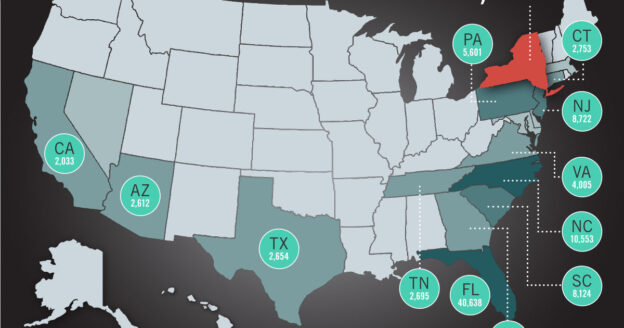

NYSLRS retirees are found in every state. Florida, not surprisingly, is the second choice for retirees after New York. Roughly 41,000 call the Sunshine State home. North Carolina is third, followed by New Jersey and South Carolina. North Dakota has the fewest retirees and beneficiaries—only 23.

NYSLRS Retirees Around the World

There are 649 NYSLRS retirees and beneficiaries living around the world but the most common countries are:

- Canada: 176

- Israel: 48

- England: 32

- Philippines: 32

- US Virgin Islands: 29

Learn More

Check out our 2024 Annual Comprehensive Financial Report for more information about NYSLRS, the Common Retirement Fund and our nearly 1.2 million members, retirees and beneficiaries.

Note: All data is as of the State fiscal year end, March 31, 2024.