Since taking office in 2007, Comptroller Thomas P. DiNapoli has been committed to fighting public corruption and protecting the New York State and Local Retirement System from pension fraud.

Teamwork

Comptroller DiNapoli, through his Division of Investigations, partners with federal, state, and local law enforcement at every level of government. The Division’s pension fraud investigations have resulted in dozens of arrests and convictions and the recovery of nearly $3 million dollars.

The Retirement System’s Pension Integrity Bureau (PIB) is responsible for recovering erroneously paid pension benefits. In many cases, this is due to the survivors’ failure to report the death of a retiree in a timely manner, but some cases involve schemes to conceal the retiree’s death to continue pocketing pension payments. When PIB comes across apparent criminal activity, it refers the case to the Division of Investigations.

Recent Cases

In June 2021, an Ontario County woman pleaded guilty to grand larceny for stealing $2,076 that was intended for a deceased friend. The woman and her friend, who was retired from the Tonawanda Public Works Department, had a joint bank account. After his death, the woman unlawfully withdrew his pension payment and $3,216 in Veterans Affairs benefits and closed the account.

That same month, an Orange County woman was arrested and charged with grand larceny for allegedly stealing her late mother’s pension payments. She attempted to hide her mother’s death from NYSLRS and more than $50,000 in pension payments were deposited into a joint account after her mother’s death. The woman allegedly used the money to pay bills and make personal purchases, including fast food, liquor, clothing, gas and entertainment.

Other Notable Cases

Some people have taken elaborate measures to keep the pension payments coming in. For example, there was the Queens man who left his father’s body in a morgue for more than a year while he siphoned off $7,542 in pension payments and $17,790 in Social Security from his father’s bank account.

In many instances, the pension fraud involves substantial amounts of money which can lead to serious penalties for those who get caught. A few years ago, a Florida woman was sentenced to 2-to-6 years in State prison after she was convicted of stealing more than $120,000 in pension payments after her uncle’s death. She sent false information to his bank indicating he was still alive, then used her power of attorney to withdraw pension payments for several years.

Then there was the man who impersonated his dead brother in order to collect more than $180,000 in pension benefits. The Retirement System learned of the brother’s death and stopped payments to a trust account the man controlled. The man phoned the NYSLRS Call Center pretending to be his deceased brother demanding his money and insisted he was alive. The ploy failed and he was sentenced to 6 months in jail and 5 years probation. He also signed a $180,140 judgment and had to repay NYSLRS.

Your Pension Fund is Secure

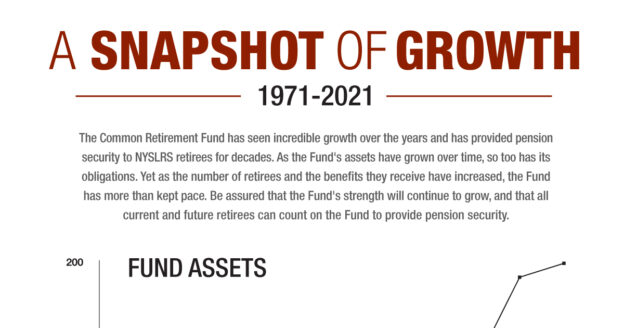

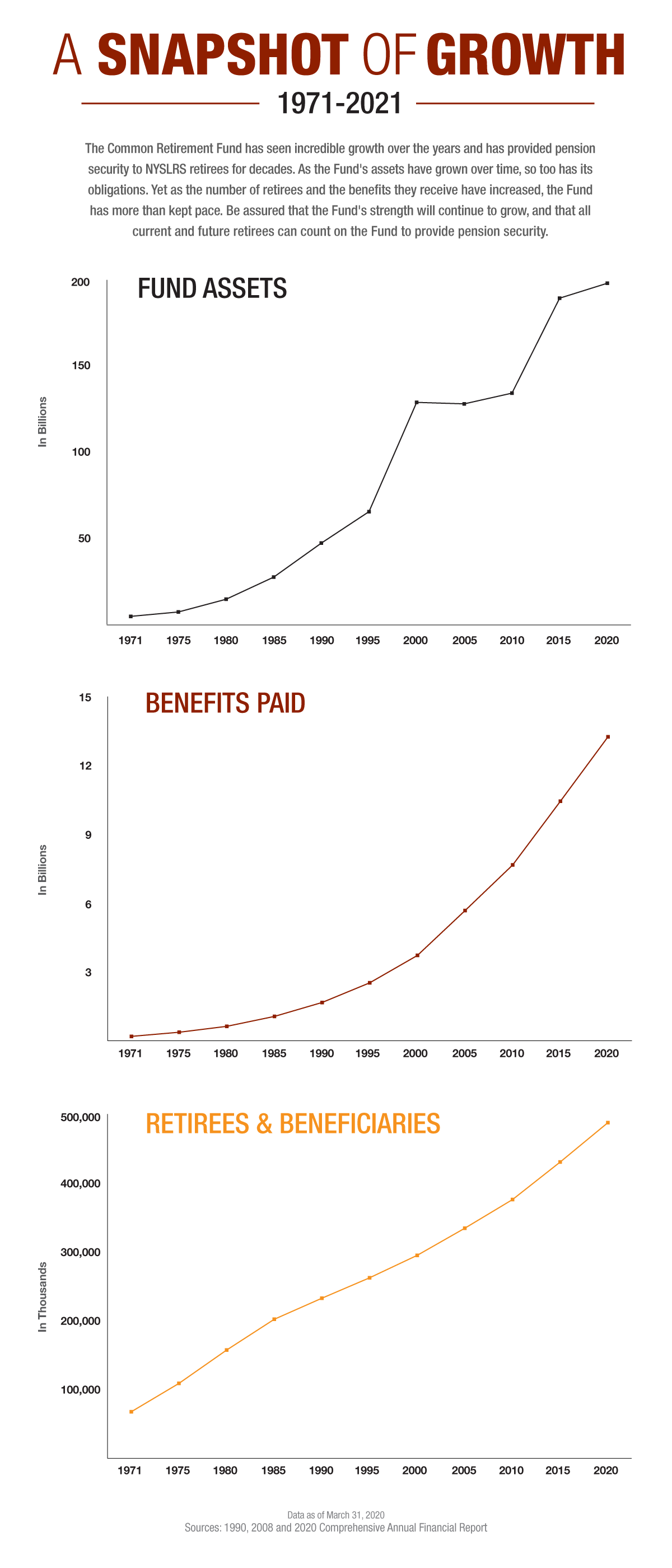

The Pension Fund, which provides the money for pension payments and was valued at an estimated $254.8 billion as of March 31, 2021, has long been recognized as one of the best-managed and best-funded public pension funds in the nation. The State Comptroller’s ongoing effort to combat pension fraud and abuse is just one more reason that the Fund remains safe and secure.

New Yorkers can report allegations of fraud involving taxpayer money by calling the toll-free Fraud Hotline at 1-888-672-4555.