Tax season is here. If you received a distribution of retirement benefits from NYSLRS last year and need to report it as income on your taxes, you don’t have to wait for the mail—1099-R tax forms are available online.

While NYSLRS pensions are not subject to New York State or local income tax, most are subject to federal income tax.

Beneficiaries who received a death benefit and members who took a taxable loan or withdrew their contributions may also be subject to federal income tax.

If NYSLRS is required to report your distribution to the Internal Revenue Service (IRS), we provide a 1099-R tax form to you for filing your taxes.

We distribute 1099-R tax forms annually based on your delivery preference:

Mail: We mail printed 1099-Rs by January 31. (Note: The default delivery preference is mail.)

Email: We make 1099-Rs available in Retirement Online sooner than printed copies are mailed—we will notify you by email in mid-January. (Note: You will not receive a printed 1099-R in the mail.)

Select an option from Year dropdown. (Note: 2025, 2024 and 2023 are currently available online.)

Click Generate button.

If you have one 1099-R, the document will open in a new browser tab. If you have more than one 1099-R, the documents will compile into a zip file and download on to your computer. Go to your Downloads folder and double-click on the zip file to access the documents.

Please check your browser settings and disable pop-up blockers to ensure your 1099-R can be generated. By default, your browser may block pop-ups, which may prevent a new tab from opening or the file from downloading.

If you don’t have an account or for help signing in to an existing account, check out our Retirement Online Tools and Tips , for step-by-step instructions to register, reset your password, unlock your account and more.

Understanding Your 1099-R

Your tax form includes:

The total amount (before taxes and deductions) paid to you for the year indicated on the form.

The taxable portion of your benefit.

The amount of federal income tax withheld for the year indicated on the form and paid to the IRS on your behalf.

For more information, check out our interactive 1099-R guide. It walks you through a sample and offers a short explanation of each box on the form.

Get an Email Notification When 1099-R Tax Forms Are Available Online

You can get your 1099-R online sooner than printed copies are mailed. Update your delivery preference to email and when your 1099-R is available, we’ll send an email notifying you to sign in to Retirement Online.

Here’s some information to help you register, reset your password, unlock your account and more.

Register for Retirement Online

If you don’t have an account, learn more about Retirement Online and click Register Now. You will be asked to identify yourself, confirm your Social Security number and verify your identity for security reasons.

Next, you’ll create your User ID and password. Retirement Online has requirements to help you create a password that won’t be easily guessed or broken, but the Social Security Administration offers some additional helpful tips, including:

Instead of just random characters, use longer, easy to remember phrases in your password.

Use different passwords for your online accounts, so a single stolen password doesn’t compromise multiple accounts.

Don’t use personal information like your birthday or a pet’s name in your password.

Select Security Questions and Remember Your Answers

After you sign in for the first time, you’ll need to choose security questions and submit answers. Make sure you remember your responses. You’ll have to answer these questions again to look up your user ID, reset your password or unlock your account.

Over the last year, NYSLRS has seen an increase in check fraud and the delayed receipt of pension checks sent by mail. That is why we are urging all retirees and beneficiaries who still receive pension checks by mail to enroll in our Direct Deposit program, just as the Social Security Administration requires you to receive that benefit.

Direct deposit is fast, convenient and secure. Your pension payment will be deposited directly into your bank account on the last business day of each month and available to you immediately. No more waiting for a check in the mail or having to travel to the bank to cash it. And you won’t need to worry about your check being lost or stolen.

Use Retirement Online to Sign Up for Direct Deposit

Retirement Online is the fastest and most secure way to sign up for direct deposit.

From Account Homepage, look under I want to… (located at the top right)

Click Update Direct Deposit link.

Follow steps to add your bank account number and routing number.

If you have a joint account holder on your bank account, you’ll need to print and complete the Electronic Funds Transfer Direct Deposit Enrollment Application (RS6370) and have your joint account holder sign the form. It’s best to do this in advance so you can upload the completed form while signing up in Retirement Online. (However, you can upload the completed form later.)

Other Ways to Sign Up for Direct Deposit

If you don’t have a Retirement Online account, you can download and complete an Electronic Funds Transfer Direct Deposit Enrollment Application (RS6370). However, please be aware, you must attach a voided check or have a bank representative complete Section 3 of the form. Paper forms also take longer to process.

Attach your completed form using the Browse… button.

Or by mail:

NYSLRS 110 State St. Albany, NY 12244-0001

Keep Your Direct Deposit Information Updated

It’s important to notify NYSLRS as soon as possible if you change financial institutions or accounts. Retirement Online is the fastest and most convenient way to update your bank account information. Your changes will generally be applied to your next month’s pension payment. Our Pension Payment Calendar lists the dates your pension payment will be deposited into your bank account each month.

Most State and municipal employees are required to join the New York State and Local Retirement System (NYSLRS) when they are hired. But for some employees, membership is optional, meaning you are not automatically enrolled. To join NYSLRS, you must submit a membership application to your employer, who will then enroll you in NYSLRS. It’s important to understand the valuable benefits of NYSLRS membership and why you should join as soon as possible.

Whose Membership is Optional or Mandatory

Membership is optional if:

You work less than 12 months per year, including 10-month school employees working full-time;

You work less than 30 hours per week or less than the number of hours for full-time employment, as established by your employer for your position;

You are in a temporary or provisional position (under Civil Service Law); or

Your annual compensation is less than New York State’s minimum wage multiplied by 2,000 hours.

Membership is mandatory if:

You are in a permanent, full-time, 12-month position of an employer who participates in NYSLRS; and

You are in a full- or part-time position covered by the Police and Fire Retirement System (PFRS), such as police officers and firefighters.

If you aren’t sure whether you’re a member, your employer should be able to let you know. Contact us if you have questions.

Benefits of Joining NYSLRS

NYSLRS is one of the largest retirement systems in the world, administering benefits for more than 1.2 million members, retirees and beneficiaries.

If you aren’t sure whether to join NYSLRS, here are the advantages:

Your NYSLRS pension is a defined benefit plan. When you retire, you will receive a monthly pension payment for the rest of your life. Once you reach retirement age, you can retire with as few as five years of service credit (part-time service is pro-rated).

You can request additional service credit for your public employment before joining NYSLRS or if you served in the U.S. Armed Forces and received an honorable discharge from active military duty.

You can transfer service if you are still a member of another public retirement system in New York State.

You can reinstate service if you withdrew your membership in NYSLRS or another public retirement system in New York State.

You can take aloan against your retirement contributions once you meet eligibility requirements.

NYSLRS retirement plans provide death and disability retirement benefits.

Nearly 3,000 employers participate in NYSLRS, allowing you to continue your membership if you take a job at another New York State public employer. And if you decide to leave public employment before you have ten years of service credit, you can withdraw your contributions plus interest or roll over your contributions into another retirement savings plan.

NYSLRS Membership Basics

Once you join and become a NYSLRS member:

You are assigned to a tier based on your date of membership. New members are in Tier 6.

You are required to contribute a percentage of your earnings toward your retirement. As a Tier 6 member, your contribution rate (between 3%–6%) will be based on your earnings.

It’s important to join NYSLRS at the start of your employment. If you don’t join right away, you can purchase service credit for your public employment from before you became a member, but it will cost more—6% of your earnings plus interest rather than contributing a percentage based on your earnings. Also, while you can request previous service credit and pay for the cost at any time, you must earn two years of service credit as a NYSLRS member before your purchased service can be credited.

Get Credit for All Your Public Service

Because service credit is a major factor in calculating your pension benefit, it’s important to make sure you get credit for all your public service. Once you join NYSLRS, you should request any additional service as early in your career as possible.

NYSLRS will need time to request records from your previous employer or retirement system.

The sooner you purchase your credit, the less it will generally cost.

Requesting early gives you time to pay for additional service.

Your request will be reviewed to determine your eligibility. We will send you a letter with the amount of service credit you are eligible to receive if you choose to purchase it, the cost and payment options. There are certain situations where purchasing additional service credit will not increase your pension. For more information, read about whether should you purchase additional service credit.

October is National Retirement Security Month. It’s a time to consider the importance of saving and to think about potential sources of income in retirement. Financial security doesn’t just happen—it takes preparation and time. Even if retirement seems far off, it’s never too early to start planning.

NYSLRS and Retirement Security

Check out these blog posts to learn more about how your NYSLRS pension and other sources of retirement income can provide retirement security.

As a NYSLRS member, you are enrolled in a defined benefit plan, also known as a traditional pension plan. When you retire, you will receive a monthly pension payment for the rest of your life. Your pension will be calculated using a preset formula based on your earnings and years of service—it will not be based on the individual contributions you paid into the system.

Your NYSLRS pension is a good reason to be optimistic about your finances in retirement. But there is more to a financially secure retirement than having a pension. Think of retirement security as a three-legged stool. Each leg is a source of income to help support you when your working days are done.

If you want to improve your chances of a financially secure retirement, your plan should include retirement savings. It’s important to start saving early so your money has time to grow. When you invest your savings in an individual retirement account (IRA) or a 401(k)-style retirement savings plan, you earn a return on your investment, and those returns are compounded.

For greater financial stability and flexibility, you may want to invest in a deferred compensation savings plan. The New York State Deferred compensation plans are voluntary retirement savings plans like a 401(k), created for New York State employees and employees of other participating public employers.

As you get close to retirement, it’s a good idea to take inventory of any debt you owe. Paying down your debt—including any NYSLRS loans—will help avoid a pension reduction and can give you more flexibility in retirement.

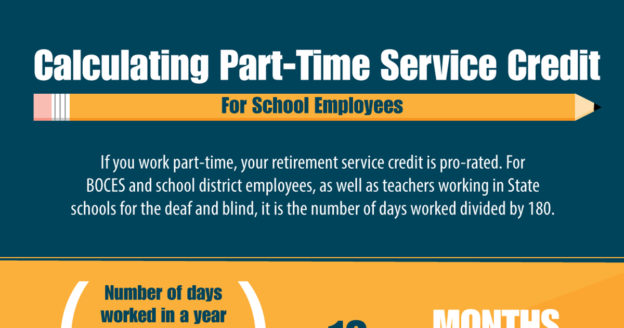

While most New York teachers and administrators are in the New York State Teachers’ Retirement System, other school employees are members of the New York State and Local Retirement System (NYSLRS). In fact, 1 out of 5 NYSLRS members works for a school district. Their employment is tied to the school year, which is usually 10 months long. So how do we determine service credit for school employees?

You earn service credit for your paid employment with a public employer in New York State. That credit is based on the number of days you work, which your employer reports to us.

Calculating Service Credit for Full-Time School Employees

If you work full-time, you receive one year of service credit per school year, which usually refers to the 10-month period from September through June.

You cannot earn more than one year of service credit, so if you work full-time during the school year, you will not earn additional service credit if you also work during the summer.

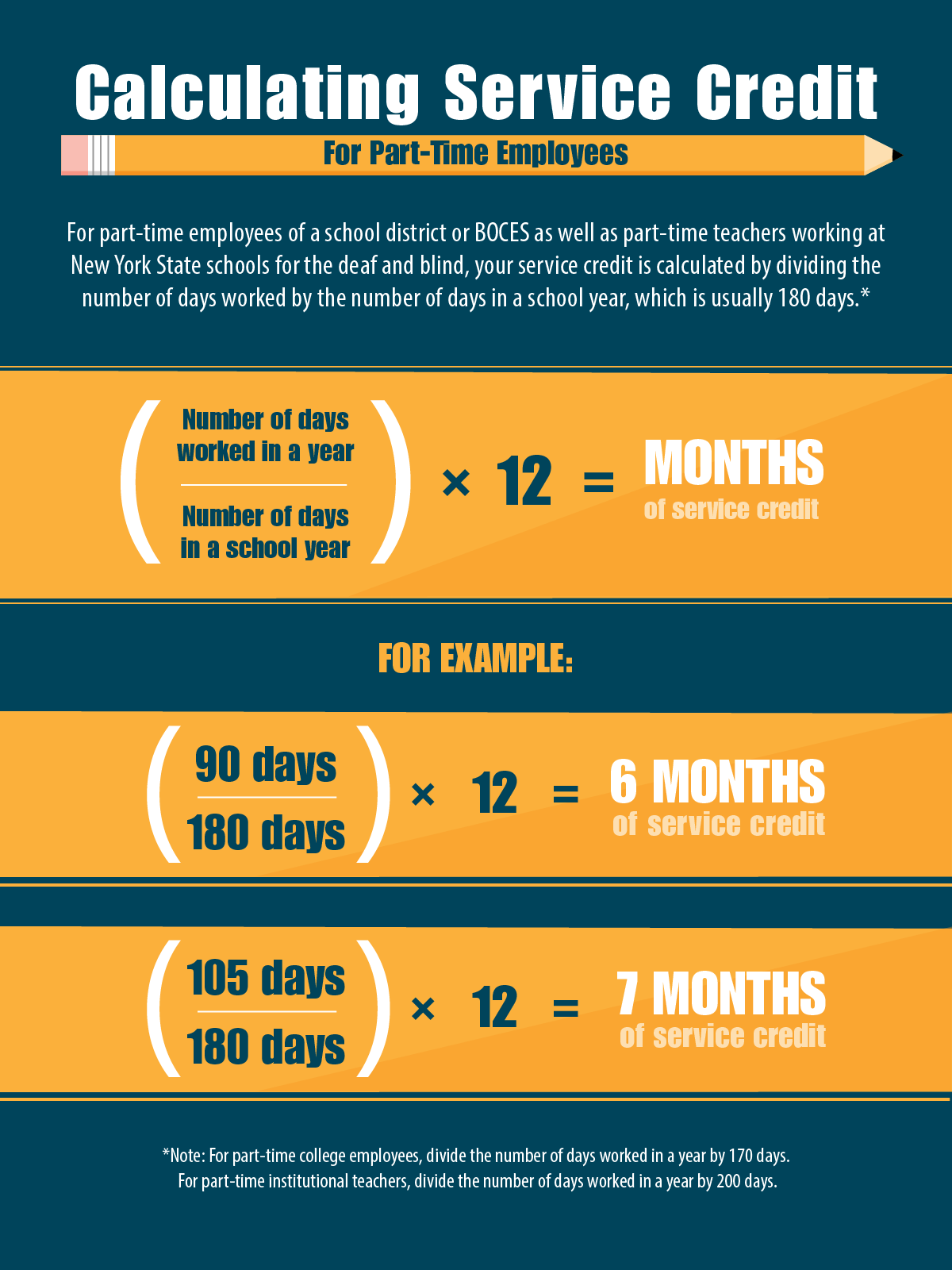

Calculating Service Credit for Part-Time School Employees

Your employer determines how many hours are in a full-time day for your position and reports the number of days you work to NYSLRS. Your service credit for the year is then calculated by dividing the number of days worked by the number of days in a school year. Usually, a school year refers to the 10-month period from September through June, which is 180 days. However, depending on your employer, an academic year can be 170 or 200 days.

For employees of school districts and BOCES, as well as teachers working at New York State schools for the deaf and blind: Number of days worked ÷ 180 days

For college employees: Number of days worked ÷ 170 days

For institutional teachers: Number of days worked ÷ 200 days

Look for Total Estimated Service under My Account Summary.

Get Credit for All Your Public Service

Service credit is one of the major factors in calculating your pension benefit, so it’s important to make sure you get credit for all your public service.

Worked for your current or another public employer before joining NYSLRS; or

Served in the U.S. Armed Forces and received an honorable discharge from active military duty.

Or you may be able to:

Transfer service: If you are still a member of another New York State public retirement system.

Reinstate service: If you withdrew your membership in NYSLRS or another New York State public retirement system.

In most cases, you have to pay for additional service or to reinstate service. But because service credit is a factor in the calculation of your retirement benefits, it will usually increase your pension.

If you choose to purchase the additional service, you should submit your request as early in your career as possible. Records we need to verify your service will be more readily available. And the sooner you purchase your credit, the less it will generally cost.

The celebration of everything New York begins Wednesday, August 20, and runs through Monday, September 1 (Labor Day). Our information representatives will be at the fairgrounds in Syracuse daily, from 10:00 am to 9:00 pm.

NYSLRS will be in the Center of Progress Building, Building 3 on the State Fair map, near the Main Gate. Look for us at booth 227.

Find Unclaimed Funds at the State Fair

OSC’s Office of Unclaimed Funds booth will also be in the Center of Progress Building. An unclaimed fund is lost or forgotten money. If an organization such as a bank, insurance company, corporation or state agency owes you money but hasn’t been able to contact you, they turn that money over to the Comptroller’s Office.

Student Youth Day— Free admission for youths and students under 18 years old. ID showing date of birth may be requested.

Agriculture Career Day

Friday, August 22

Pride Day—The first state fair in America to host an official Pride Day to celebrate the LGBTQIA+ community.

New Americans Day

Family Fishing Day

Monday, August 25

Law Enforcement Day—Free admission for any active or retired law enforcement or corrections personnel with a badge or picture ID from the department where they are or were employed.

State Parks Day

Maple Day

Tuesday, August 26

Fire, Rescue and EMS Day—Free admission for any active or retired member of a fire department, emergency services or EMS organization with a picture ID from that department or organization.

Comptroller DiNapoli Visits the Fair—He is the trustee of the New York State Common Retirement Fund, the administrative head of NYSLRS and custodian of unclaimed funds. He will present area residents and organizations with unclaimed funds and stop by the NYSLRS booth.

Beef Day

Wednesday, August 27

Women’s Day

Sensory Friendly Day

Thursday, August 28

Armed Forces Day—Free admission for any active-duty service member or veteran with military identification (military ID card, form DD-214, or NYS driver license, learner permit or nondriver ID card with a veteran designation).

Dairy Day

Stomp Out Stigma Day

Friday, August 29

Native American Days—Free admission for all members of Native American tribes, no ID required.

When you’re ready, Retirement Online makes applying for retirement fast and convenient. There are no forms to mail in and nothing to have notarized. When you apply online, you’ll be able to:

See estimates of your pension for the payment options available to you.

Upload documents while applying or after submitting your application.

Submit changes to your application quickly and easily if needed.

Your date of retirement is up to you! Keep in mind:

You must apply at least 15 days but no more than 90 days before your chosen retirement date.

You must stop working and be off your employer’s payroll on your retirement date (your last day on payroll must be no later than the day before your retirement date).

Your date of retirement can be a weekend or holiday (for example, if your last day of work is a Friday your retirement date can be Saturday).

Select Your Pension Payment Option

You can choose from several pension payment options, all of which provide you with monthly pension payments for the rest of your life. The Single Life Allowance provides the maximum amount, but upon your death, payments will stop—there will be no continuing payments to a beneficiary, even if you die soon after retiring. Or, you can choose to receive a reduced monthly pension payment to provide for:

Most NYSLRS pensions are subject to federal income tax, and NYSLRS is required to withhold federal income tax from your pension benefit at the default withholding status of “single with no adjustments” unless you inform us otherwise. Enter federal tax withholding information to adjust the amount withheld.

Note: NYSLRS pensions are not subject to New York State or local income tax. However, if you permanently move to another state, that state may tax your pension.

Sign Up for Direct Deposit

With direct deposit, your pension payment will be deposited directly into your bank account on the last business day of each month. It’s fast, convenient and secure. Save time and set up direct deposit pension payments when you apply for retirement by entering your bank account number and routing number.

If you have a joint account holder on your bank account, you’ll need to print and complete the Electronic Funds Transfer Direct Deposit Enrollment Application (RS6370) and have your joint account holder sign the form. It’s best to do this in advance so you can upload the completed form while adding your direct deposit information in Retirement Online. However, you can upload the completed form later.

Upload Proof of Date of Birth

You must submit proof of your date of birth before any pension benefits can be paid. If you select a pension payment option that provides a lifetime pension benefit to a beneficiary upon your death, you must submit proof of your beneficiary’s date of birth as well.

Upload one of the following acceptable documents:

Birth certificate

New York State driver’s license

Passport or passport card

Marriage certificate, if it shows your age on a given date or the date of birth

If you don’t have one of these documents available when you apply online, you can submit them later. However, if your submission is not timely, your first payment may be delayed.

Pay Off Outstanding Loans and Service Credit Purchases

You’ll see which employers reported service credit for you. Review your employment history and add any missing public employment.

You can request additional service credit for previous employment or military service, or you can request a transfer or tier reinstatement when you apply to retire. However, remember it’s best to make these requests well before you apply.

One Exception—Disability Retirement

You may be eligible for a disability retirement benefit if you are permanently disabled and cannot perform your duties because of a physical or mental condition. Applications for disability retirement can’t be submitted in Retirement Online. If you are applying for a disability retirement, you must submit a paper application. Visit our Disability Benefits page for more information.

For Benefit Information, Read Your Retirement Plan Publication

Your service and disability retirement benefits and death benefits are based on your tier, retirement plan, service credit, and other factors. For comprehensive information about your retirement benefits and how your pension will be calculated, find your NYSLRS retirement plan publication.

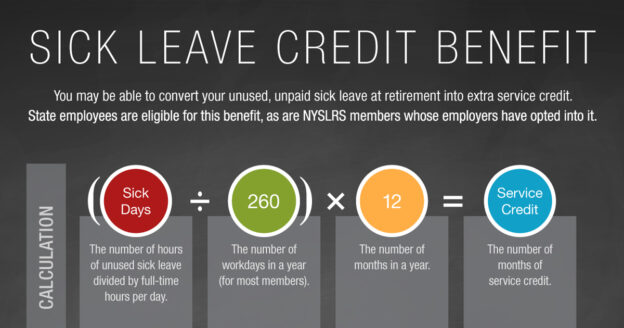

To receive this benefit, you must retire directly from public service or within a year of leaving. The additional service credit for your unused, unpaid sick leave, up to a certain limit, will be added to your total years of service when calculating your pension benefit. However, it cannot be used to:

Qualify for vesting. For example, if you have four years and ten months of service credit and you need five years to be vested, your sick leave credit cannot be used to reach the five years.

Qualify for a better retirement benefit calculation. For example, if you have 19 ½ years of service credit but your pension calculation will improve substantially if you have 20 years, your sick leave credit cannot be used to reach the 20-year calculation.

Meet the service credit requirement for a special 20- or 25-year plan.

Increase your pension beyond the maximum allowed under your retirement plan.

The additional service credit is based on your total hours of unused, unpaid sick leave and the number of hours in your employer’s standard workday.

For More Information

For comprehensive information about your retirement benefits and how your pension will be calculated, find your retirement plan publication. And as you approach retirement, read our Preparing for Retirement blog post for guidance, including topics to consider and actions to take as you plan.

Retirement is a big step, and we want to make sure you’re ready when the time comes. Read on for guidance on preparing for retirement, including topics to consider as you plan and actions to take.

Understand Your NYSLRS Pension

Your NYSLRS pension will be based on your tier, service credit, final average earnings and your retirement plan. For most members, age is also an important factor in your NYSLRS benefits.

Service credit is one of the major factors in calculating your pension benefit, so it’s important to make sure you get credit for all your public service. You may be able to request additional service credit if you:

Worked for your current or another public employer before joining NYSLRS; or

Served in the U.S. Armed Forces and received an honorable discharge from active military duty.

Or you may be able to:

Transfer service: If you are still a member of another New York State public retirement system.

Reinstate service: If you withdrew your membership in NYSLRS or another New York State public retirement system.

You must submit your request before retirement, and you should do it as early in your career as possible. NYSLRS will need time to request records from your previous employer or retirement system, and requesting early also gives you time to pay for additional or reinstated service. Also, the sooner you purchase your credit, the less it will generally cost.

Pay Off Service Credit Purchases

If you requested additional service credit for previous public employment or military service and you received a cost letter, make sure you’re on track to pay off your service credit purchase before you retire.

You won’t receive credit for optional service that is not paid off when you retire.

If you are in the process of paying for mandatory service credit (for example, from a reinstated membership or if insufficient contributions were made to NYSLRS) and it’s not paid off by your date of retirement, your pension will be permanently reduced.

Sign in to Retirement Online to check your service credit purchase balance, make a lump sum payment or increase your payroll deduction amount.

Pay Off Your NYSLRS Loan

It’s important to understand the implications of retiring with an outstanding loan. Your pension will be permanently reduced, and in most cases, you’ll need to report at least some portion of the loan balance as income to the Internal Revenue Service (IRS). If you retire before age 59½, the IRS may also charge an additional 10% penalty.

To ensure you’re on track to pay off your loan before you retire, sign in to Retirement Online to check your balance, make a lump sum payment or increase your payroll deduction amount.

Estimate Your Pension

Finding out how much you can expect to receive is a critical step in preparing for retirement. Most members can estimate their pension using Retirement Online in just a few quick and easy steps.

Retirement Online uses your current earnings and service information to calculate your estimate, including your final average earnings (FAE) and the amounts for the pension payment options available to you. You can fine-tune your estimate or see how different choices would affect your benefit.

Remember, the amounts are estimates, not a guarantee of what you’ll receive when you retire.

Understand How Divorce May Affect Your Pension

In New York State, pensions and retirement benefits earned during the marriage may be marital property and can be divided when a marriage ends. Divorce can affect your pension and other retirement benefits in the following ways:

Your ex-spouse may be entitled to a portion of your pension.

You may be required to name your ex-spouse as the beneficiary of any death benefit.

You may be required to choose a pension payment option that provides a continuing benefit to your ex-spouse when you die.

Your ex-spouse may be entitled to a portion of your cost-of-living adjustment (COLA).

Any division of pension and retirement benefits must be stated in the form of a Domestic Relations Order (DRO)—a court order issued after a final judgment of divorce which specifies how benefits should be split.

It’s important to complete and submit your DRO to NYSLRS well before you apply for retirement to avoid changes or delays in your pension payments.

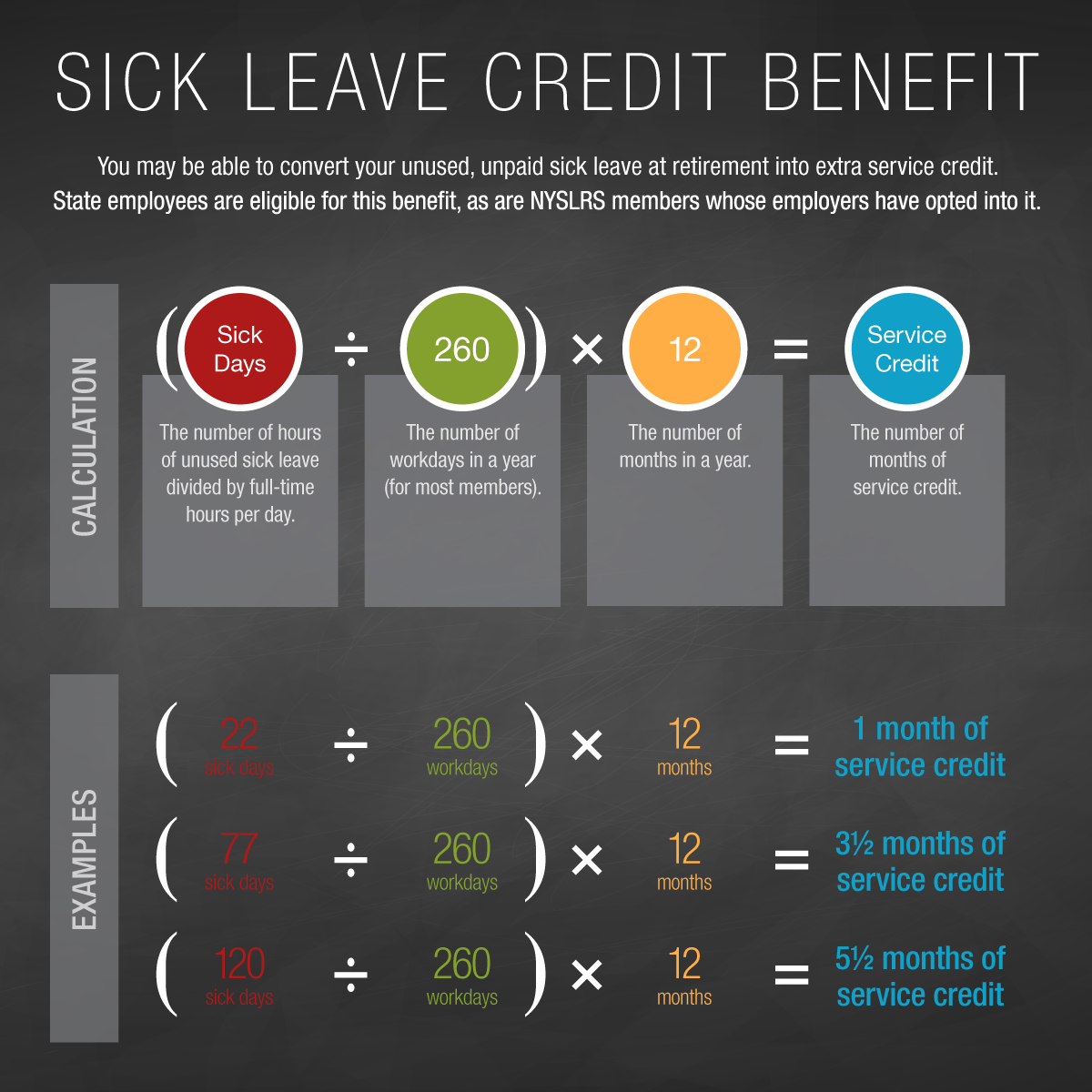

Check Your Eligibility for the Sick Leave Benefit

To be eligible for the Sick Leave Benefit, your employer must have adopted Section 41(j) of the Retirement and Social Security Law (RSSL) for ERS members or 341(j) of the RSSL for PFRS members. If your employer has chosen to offer this benefit, you may receive service credit for unused, unpaid sick leave at retirement.

To check if this benefit is available to you, ask your employer or sign in to Retirement Online and look for Sick Leave Eligibility.

To receive this benefit, you must retire directly from public service or within a year of leaving. The additional service credit for your unused, unpaid sick leave, up to a certain limit, will be added to your total years of service when calculating your pension benefit. However, it cannot be used to:

Qualify for vesting. For example, if you have four years and ten months of service credit and you need five years to be vested, your sick leave credit cannot be used to reach the five years.

Qualify for a better retirement benefit calculation. For example, if you have 19 ½ years of service credit but your pension calculation will improve substantially if you have 20 years, your sick leave credit cannot be used to reach the 20-year calculation.

Meet the service credit requirement for a special 20- or 25-year plan.

Increase your pension beyond the maximum allowed under your retirement plan.

Review Your Health Insurance Coverage

NYSLRS does not administer health insurance programs. When you’re nearing retirement, you should check with your employer’s human resources or personnel office or your health benefits administrator to determine your eligibility for health insurance coverage during retirement. If your former employer instructs us to do so, we will deduct health insurance premiums from your monthly pension payment, but NYSLRS cannot answer questions about coverage or changes in premium amounts.

If you are eligible to use your unused, unpaid sick leave to offset the cost of NYSHIP, payment towards your health insurance coverage will not affect your eligibility for the Sick Leave Benefit.

Schedule a Pre-Retirement Consultation

Before you apply for retirement, you may want to consider scheduling a pre-retirement consultation where you can speak with one of our representatives to review your benefits and ask any questions you may have.

Ready to Apply for Retirement?

When you’re ready, Retirement Online makes it fast and convenient to apply for retirement. There are no forms to mail in and nothing to have notarized. You’ll see an estimate of your pension, including the amounts for the pension payment options available to you. You’ll also be able to upload documents while applying or after submitting your application. And if you need to update your application, you can quickly and easily submit changes. But before applying, visit our Preparing and Applying for Retirement page for an overview of the retirement application so you know what to expect and what information you’ll need to submit.

Tax season is here. If you received a distribution of retirement benefits from NYSLRS last year and need to report it as income on your taxes, you don’t have to wait for the mail—1099-R tax forms are available online.

Tax season is here. If you received a distribution of retirement benefits from NYSLRS last year and need to report it as income on your taxes, you don’t have to wait for the mail—1099-R tax forms are available online.

Over the last year, NYSLRS has seen an increase in check fraud and the delayed receipt of pension checks sent by mail. That is why we are urging all retirees and beneficiaries who still receive pension checks by mail to enroll in our

Over the last year, NYSLRS has seen an increase in check fraud and the delayed receipt of pension checks sent by mail. That is why we are urging all retirees and beneficiaries who still receive pension checks by mail to enroll in our

While most New York teachers and administrators are in the

While most New York teachers and administrators are in the