October is National Retirement Security Month. It’s a time to consider the importance of saving and to think about potential sources of income in retirement. Even if retirement seems far off, it’s never too early to start planning.

NYSLRS and Retirement Security

Check out these blog posts to learn more about how your NYSLRS pension and other sources of retirement income can provide retirement security.

What is a Defined Benefit Plan? Your NYSLRS pension is a defined benefit retirement plan. When you retire, you’ll receive a guaranteed, lifetime benefit based on your earnings and years of service. A preset formula determines your benefit; it’s not limited to your accumulated contributions and investment returns, like with a 401(k)-style plan.

The 3-Legged Stool Approach to Retirement Confidence Think of your retirement security as a three-legged stool. Each leg represents a different income source that supports you in retirement. The first leg of the stool is your NYSLRS pension, and the second is your Social Security benefit. The third leg is your own personal savings, which can help provide security in retirement and give you more freedom to do the things you want to do.

Compounding: A Great Way for Your Money to Grow The sooner you start saving, the better—especially if you invest in a retirement savings plan that reinvests the returns you earn. Such compounded savings increase in value by earning interest on both the principal and accumulated returns. But for your money to make more money in this way, it needs time to grow.

Deferred Compensation: Another Source of Retirement Income Deferred compensation plans are voluntary retirement savings plans like 401(k) or 403(b) plans designed and managed with public employees in mind. You can contribute as little as 1 percent of your earnings—automatically deducted from your paycheck. Deferring income from your take-home pay may mean less money to spend in the short-term, but it’s an easy way to start saving extra for retirement.

Give Your Retirement Savings a Boost Once you’ve started saving for retirement, you may want to look for ways to increase how much you save. Even small increases can make a big difference over time—and may have a minimal impact on your take-home pay.

Remember, retirement security doesn’t just happen—it takes planning.

Visit our Retirement Planning page for more information about your NYSLRS pension, including a calculator to estimate your monthly payments and a tool to help you find your retirement plan publication for a complete description of your benefits.

That depends. If you choose a pension payment option that provides a lifetime benefit for a beneficiary, you cannot change your beneficiary even if they die before you do. However, if you choose a pension payment option that provides a benefit for a certain period after retirement, you can change your beneficiary after you retire. Learn more about the different pension payment options and whether they allow you to change your beneficiary below.

If your retirement plan provides a one-time lump sum death benefit after you retire, you can also change your beneficiary (or beneficiaries) for that benefit.

Single Life Allowance option: Provides the maximum monthly benefit payment to you for the rest of your life. This option does not provide a continuing benefit so you will not select a beneficiary, and all payments stop when you die.

Joint Allowance options:Provide a lifetime benefit to a loved one in exchange for a reduction to your monthly benefit payment. After your death, your beneficiary will continue to receive your pension (or part of it, depending on the option you choose) for the rest of their life. If your beneficiary dies before you, your monthly benefit payment remains the same and all payments stop when you die. However, if you choose one of the Popup-Up/Joint Allowanceoptions and your beneficiary predeceases you, your monthly benefit payments will increase to the amount payable under the Single Life Allowance option. For these options, you can only choose one beneficiary, and you cannot change your beneficiary after you retire.

Five Year Certain or Ten Year Certain options:Provide a benefit for a certain period after retirement in exchange for a reduction to your monthly benefit payment. If you die within the five- or ten-year period after your retirement (depending on the option you choose), your beneficiary will continue to receive your monthly pension payment for the remainder of the five- or ten-year period. For these options, you can choose more than one beneficiary, and you can change your beneficiary after you retire.

Post-Retirement Death Benefit

Your pension is not your only NYSLRS retirement benefit. Most NYSLRS retirees are eligible to leave a death benefit if they retired directly from payroll or within one year of leaving employment. The post-retirement death benefit is a one-time lump sum payment. For information on how it’s calculated, visit our Death Benefits for Retirees page.

You can change your beneficiary for this benefit at any time, and your beneficiaries for this benefit do not have to be the same as your pension payment option beneficiary.

Manage Your Beneficiaries in Retirement Online

The fastest way to view or update your beneficiaries for your post-retirement death benefit is in Retirement Online.

Sometimes a small misunderstanding can have a big impact on your retirement benefits. We debunked some common retirement myths in an earlier blog post. Here are five more myths you should be aware of.

Retirement Myths vs Facts

I updated my contact information with my employer, so I don’t need to update it with NYSLRS.

You need to update your contact information with both your employer and NYSLRS. Your employer does not provide updated member contact information to us. Make sure we have your current mailing address, phone number and email address on file so you receive the news, correspondence and statements we send you. Retirement Online is the fastest way to view and update your contact information with NYSLRS.

I can’t estimate my pension benefit until I’m close to retirement.

Even if you are years away from retiring, you can estimate your pension benefit in minutes using Retirement Online. Enter different retirement dates and beneficiaries to see how your choices affect your potential benefit and customize your estimate by adjusting your earnings if you anticipate a pay increase before you retire. (Note: Some members may not be able to use the Retirement Online pension calculator because of their circumstances—the system will notify you if your estimate cannot be completed, and you can send us a message using our secure contact form to request one.)

If I retire with an outstanding loan, my pension payment will be reduced temporarily until the loan is paid off.

If you retire with an outstanding loan, your pension will be permanently reduced.* We do not withhold loan deductions after retirement and apply it toward the outstanding balance until it’s paid in full.

Also, all or part of your outstanding loan balance may be subject to federal income taxes. If you retire before age 59½, the IRS may charge an additional 10 percent penalty.

*Employees’ Retirement System (ERS) members can repay their NYSLRS loan after they retire. However, you would need to pay the full balance of the loan in a one-time lump sum payment. Your pension would then be recalculated to remove the reduction and your monthly payment would increase going forward, but it would not be retroactive to your date of retirement.

The only way to file for retirement and begin receiving my pension is by completing a bunch of paper forms.

You can apply for retirement in Retirement Online, which is faster and more convenient than printing and mailing forms, and there’s nothing to have notarized. And when you apply online, you can also make changes online before your date of retirement—for example, if you need to change your banking or tax information. Watch our video for more information.

I can change my pension beneficiary after I retire.

Most retirees have 30 days from the start of the month following their retirement date to change their option election. After those 30 days, only certain pension payment options let you change your beneficiary.

The Single Life Allowance option provides the maximum monthly benefit payment to you for the rest of your life, but all payments stop upon your death, so nothing will be paid to a beneficiary.

The Five Year Certain or Ten Year Certain options provide benefit payments to a beneficiary for a finite period if you die within five or ten years of your retirement—if you choose one of these options, you can change your beneficiary at any time. If you live beyond the five- or ten-year period, your beneficiary will not receive a pension benefit upon your death.

Note, most retirement plans also provide a post-retirement death benefit, which is a one-time lump sum payment to your beneficiaries—you can change your beneficiaries for this at any time.

You can find more facts about your NYSLRS benefits in your retirement plan publication. If you have account-specific questions, please message our customer service representatives using our secure contact form.

The laws governing your NYSLRS retirement benefit can be confusing. Sometimes a small misunderstanding can have a big impact on your finances. So base your financial decisions on retirement facts, not common myths.

Retirement Myths vs Facts

My NYSLRS pension is like a 401(k)-style retirement savings account and I will get my contributions back when I retire.

Your NYSLRS pension is a defined benefit plan. Your pension will be a lifetime benefit based on your earnings and years of service—it will not be based on your contributions. Member contributions support the benefits earned by current and future retirees and are an important asset of the Common Retirement Fund.

If I work for more than one NYSLRS participating employer, the service credit from both will count toward my pension benefit.

It depends. You can only earn one year of service credit in a 12-month period. If you work part-time for two participating employers, you would receive credit toward retirement from both, up to the maximum of one year. However, if you already work full-time for one NYSLRS employer, plus you work part-time for another employer, your part-time job won’t increase your retirement service credit. Also, if you are a full-time employee of a school district, you won’t earn extra service credit if you work during the summer.

NYSLRS administers health insurance coverage for its retirees.

NYSLRS does not administer health insurance programs. We may deduct premiums from a retiree’s monthly pension benefit to pay for health insurance coverage if their former employer instructs us to do so, but we can’t answer questions about coverage or changes in premium amounts.

The New York State Department of Civil Service administers the New York State Health Insurance Program (NYSHIP) for New York State retirees and some municipal retirees. If you are still working, your employer’s Human Resources (Personnel) office should be able to answer your questions about post-retirement coverage.

I can take out a NYSLRS loan after I retire.

You need to actively work for New York State or a participating employer to take a NYSLRS loan. They are not available to retirees.

If I’m vested and no longer working for a public employer, NYSLRS will automatically start paying my pension as soon as I’m eligible.

Your pension is not automatic. You must apply for retirement 15 to 90 days before your retirement date. Your retirement date is up to you. In order to retire, a NYSLRS member must terminate employment and be removed from the payroll of their employer(s) before the effective date of retirement.

Most NYSLRS members can begin collecting their pension as early as age 55. If you retire between age 55 and your full retirement age (62 or 63, depending on your tier and plan), you may face a permanent benefit reduction. If you have left public employment though, your benefit won’t increase after you reach full retirement age so don’t delay filing for retirement beyond that point.

You can find more answers about your NYSLRS benefits in your retirement plan publication. If you have account-specific questions, please message our customer service representatives using our secure contact form.

We’ve written about how divorce may affect your pension. However, as a NYSLRS member, you have other benefits divorce may affect.

If your ex-spouse will receive a share of your retirement benefits, domestic relations order (DRO) must be filed with NYSLRS. A DRO is a court order specifying how your pension should be divided as well as the distribution of other benefits discussed below.

Death Benefits and Your Beneficiaries

As of July 7, 2008, beneficiary designations for certain death benefits are automatically revoked when a divorce, annulment or judicial separation becomes final. If you are divorced, it is especially important to review your beneficiary designations to ensure your benefits will be distributed according to your wishes and your divorce agreement.

If your ex-spouse is awarded a portion of your death benefits, a DRO will specify how much your ex-spouse will receive and direct you to name your ex-spouse as a beneficiary. You should file the DRO with NYSLRS as soon as it’s officially accepted by the court and choose additional beneficiaries for the remainder of any benefits. However, if your designations conflict with the terms of the DRO, the DRO will take precedence over any other beneficiary designations.

The best way to view and update your death benefit beneficiaries is by using Retirement Online. If you are already retired, visit our Death Benefit page for retirees for information about available death benefits and how to update your beneficiaries and their contact information.

Ordinary Death Benefit

Your ordinary death benefit would be payable to your beneficiaries if you die in active service (before retiring).

Post-Retirement Death Benefit

Most members of the Employees’ Retirement System (ERS) are covered by a post-retirement death benefit, which provides a one-time, lump sum payment to your beneficiaries if you die after retiring.

Accidental Death Benefit

Your accidental death benefit may be payable to certain beneficiaries if you die as a result of an on-the-job accident. The beneficiaries of this benefit are designated by law, and only those beneficiaries may receive this benefit — even if there is a DRO.

Loans

NYSLRS members who meet eligibility requirements can take out a NYLSRS loan by borrowing a percentage of their contribution balance. Even if you are eligible, a DRO may be written to prohibit you from taking future loans.

If you retire with an outstanding loan balance, your pension will be reduced. The ex-spouse’s share of the pension will also be reduced unless the DRO specifically states the ex-spouse’s share should be calculated without reference to outstanding loans.

Contribution Refunds

Occasionally, NYSLRS may refund a member’s contributions because of a tier reinstatement, membership withdrawal or membership transfer. Some members are eligible to make voluntary contributions and withdraw them as excess contributions. Generally, if a DRO doesn’t mention a contribution refund, the member will receive the full amount.

For More Divorce Information

Visit our Divorce and Your Benefits page for more information, including how divorce can affect service credit, disability benefits or cost-of-living adjustments.

Retirees, brush up on your Retirement System knowledge!

Get Your 1099-R Tax Form in Retirement Online Starting in 2024, your 1099-R tax form will be available in Retirement Online! Get yours faster and help us ‘go green’ — update your delivery preference now to receive an email when it’s ready, instead of waiting for it in the mail. (If you choose to receive your 1099-R by email, you will not receive a printed copy in the mail. Regardless of your delivery preference, you will be able to view and print your 1099-R by signing in to Retirement Online at the end of January.)

Change Your Federal Tax Withholding in Retirement Online Retirement Online is the fastest way to update your withholding. Changes submitted by the middle of the month will generally appear in that month’s payment. Most NYSLRS pensions are subject to federal income tax (some disability benefits are not taxable).

Not Taxed by New York State Your NYSLRS pension is not subject to New York State or local income taxes. Visit our Taxes and Your Pension page for more information. If you move to another state, your pension may be subject to that state’s income tax. If you’re thinking of moving to another state, check with that state’s tax department.

Get Your Retiree Annual Statement in Retirement Online Starting in 2024, you can use Retirement Online to view and print your annual statement. Help us go green and update your delivery preference to receive an email when it’s available, instead of waiting to receive it in the mail.

Manage Your Direct Deposit in Retirement Online Use Retirement Online to securely update your direct deposit bank account information. Whether you’ve switched banks or need to move your deposits to a different account, you can make those changes quickly with Retirement Online. Changes are generally applied within one to two payments. You can find out when your next pension payment is coming by checking our online pension payment calendar.

Prove Your Pension Income Using Retirement Online You may need proof of your retirement income for housing or as part of an application for the Home Energy Assistance Program (HEAP). With Retirement Online, you can print or save an income verification letter any time you need one.

Receiving Your Annual Cost of Living Increases Once you become eligible for a cost-of-living adjustment (COLA), you will receive a permanent increase to your pension amount every September. When your net benefit amount changes, NYSLRS will inform you.

View Your Pension Payment “Pay Stub” in Retirement Online Sign in to Retirement Online to access full pay stubs for your pension payments. Select the date of the payment you want to review to see a breakdown of your pension payment, including your most recent COLA amount as well as any deductions made for health insurance, union dues, tax withholding or disbursements under a domestic relations order.

You May Leave a Death Benefit Your survivors may be entitled to a death benefit after you die. Retirement Online makes it easy for eligible retirees to view their beneficiary selections, choose different beneficiaries or change contact information for an existing beneficiary. Anyone can report the death of a retiree by using our online death report form.

Best-Funded, Best-Managed The New York State Common Retirement Fund holds and invests the assets of NYSLRS on behalf of members, retirees and their beneficiaries and continues to be one of the best-funded and best-managed public pension funds in the nation. Comptroller Thomas P. DiNapoli is the administrative head of NYSLRS and trustee of the Common Retirement Fund.

Brush up on your Retirement System knowledge! Here are 10 things all NYSLRS members should know.

Lifetime Retirement Benefit You are part of a defined benefit pension plan, which provides a lifetime benefit at retirement based on your earnings and years of service.

Qualify for a Retirement Benefit by Becoming Vested Becoming vested is a key milestone in every NYSLRS member’s career. Once you’re vested, you have earned enough service to qualify for a retirement benefit, once you meet the minimum age requirements established by your retirement plan.

Tier Determines Benefits Your tier determines your eligibility for benefits under your plan and how those benefits are calculated.

Conduct NYSLRS Business Using Retirement Online Retirement Online is the fastest and most convenient way to do business with NYSLRS. It only takes a few minutes to open your account. Use Retirement Onlineinstead of calling or mailing for instant access to benefit information and convenient tools to make account changes.

Estimate Pension Using Retirement Online Calculator Most members can use Retirement Online to create benefit estimates based on the most up-to-date information we have on file. You can enter different retirement dates and payment options to see how those choices would affect your benefit.

Use Plan Publication to Learn about Benefits Your retirement plan publication is a comprehensive source for information about your benefits.

Pension Calculated Using Highest Earnings Your final average earnings (FAE) is another major factor in calculating your NYSLRS pension. When we calculate your pension, we find the set of consecutive years (one, three or five, depending on your tier and retirement plan) when your earnings were highest.

Request Past Service Credit Before Retirement Service credit is one of the major factors in calculating your NYSLRS pension. You earn a year of service credit for each year of full-time employment with a participating employer. In some cases, you may also be able to request additional credit for past service.

NYSLRS Membership Includes Death and Disability Benefits NYSLRS membership provides more than just retirement benefits. If you become seriously ill or injured, you may be eligible for a disability benefit. And, you may also be eligible to leave a beneficiary a death benefit if you die while working for a public employer.

Best-Funded, Best-Managed The New York State Common Retirement Fund holds and invests the assets of NYSLRS on behalf of members, retirees and their beneficiaries and continues to be one of the best-funded and best-managed public pension funds in the nation. Comptroller Thomas P. DiNapoli is the administrative head of NYSLRS and trustee of the Common Retirement Fund.

NYSLRS is one of the largest public retirement systems in America, serving more than 1.2 million members, retirees and beneficiaries. Read A Look Inside NYSLRS to learn more about your retirement system.

Becoming vested is a crucial milestone for NYSLRS members. It means you have earned enough service to qualify for a retirement benefit once you meet the age or service requirements established by your retirement plan. Vesting is automatic — you don’t have to fill out any paperwork to become vested.

Years of Service Credit to Become Vested

NYSLRS members in Tiers 2 – 6 need five years of service credit to be vested.

If you work part-time, or if you have an unpaid leave of absence, it will take longer to become vested. For example, if you work half-time, you earn six months of credit toward vesting for each year on the job.

Note: Previously, Tier 5 and 6 members needed ten years of service to be eligible for a service retirement benefit. However, as of April 9, 2022, these members only need five years of service credit to be vested. The new law did not change benefit rules such as how long members must contribute, pension benefit calculations, the full retirement age, reductions to retire early or the cost to purchase previous service.

Applying for Retirement

Vesting is automatic, but you will need to apply for retirement to receive your pension — NYSLRS will not pay out your pension benefit unless you apply for it.

Pension eligibility requirements and benefit calculations depend on your tier and retirement plan. To find your tier and retirement plan, sign in to your Retirement Online account and go to the ‘My Account Summary’ section. Once you know your tier and retirement plan, you can find your retirement plan publication for comprehensive information about your benefits and filing instructions.

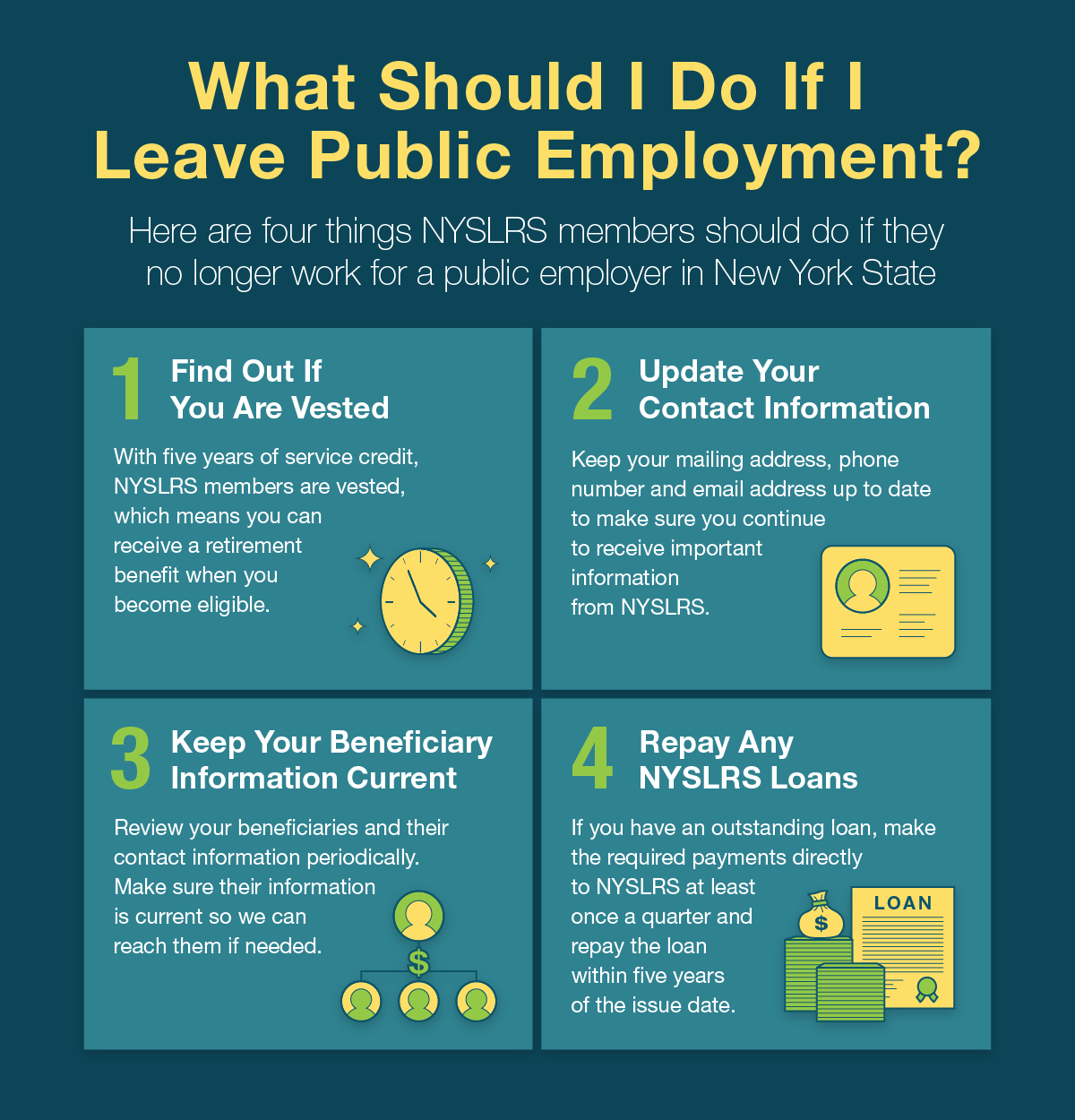

It may not come up during your career, but if you leave public employment before you are eligible to retire, you should know what happens with your NYSLRS membership and benefits. Your options will depend on how many years of service you have. It’s also important to keep your account information up to date. If you remain a member of NYSLRS after you leave public employment, you can regularly review your account information and keep it up to date by using Retirement Online.

If you have 5 or more years of service when you leave public employment, and you leave public employment before you are eligible to retire, you can receive a vested retirement benefit when you become eligible.

If you leave with between five and ten years of service, you can either remain a member and receive a vested retirement benefit when you become eligible or terminate your membership and receive a refund of your contributions.

If you leave with more than ten years of service, you cannot withdraw your NYSLRS membership and you can receive a vested retirement benefit when you become eligible and apply.

If you leave with less than ten years of service, you can end your membership and receive a refund of your contributions.

Keep Your Contact Information Updated

It’s important to make sure we have your current mailing address, phone number and personal email address, and let us know about any future changes. That way, you won’t miss important information from us, such as your Member Annual Statement.

To update your contact information, sign in to Retirement Online. Go to ‘My Profile Information,’ find your address, phone number or email address under ‘My Profile Information’ and click “update.”

Keep Your Beneficiaries Updated

If you leave public employment, your beneficiaries may still be eligible for a death benefit, so you should review your beneficiary designations periodically. Sign in to Retirement Online, go to the ‘My Account Summary’ area of your Account Homepage and click “View and Update My Beneficiaries.” Your beneficiary changes will be considered filed on the day you submit them.

Repay Any NYSLRS Loans

If you leave public employment, you will no longer be able to pay off your NYSLRS loans by payroll deduction. If you have any outstanding NYSLRS loans, you must make payments directly to NYSLRS at least once every three months and repay your loan within five years of when it was issued, or you will default on the loan. Defaulting on a loan may carry considerable tax consequences: You’ll need to pay ordinary income tax and possibly an additional 10 percent penalty on the taxable portion of the loan. You can make loan payments to NYSLRS via Retirement Online.

You aren’t eligible to take a new NYSLRS loan once you are off the public payroll.

Receiving a Vested Retirement Benefit

If you are vested, once you reach retirement age, you can receive a lifetime pension based on your salary and service from when you were working in public employment. It’s your responsibility to apply for retirement — NYSLRS will not pay out your pension benefit unless you apply for it.

The earliest date you can receive your retirement benefit depends on your tier and retirement system.

Tier 1 and 2 members are eligible for a vested retirement benefit as early as the first of the month following your 55th birthday.

Tier 3, 4 and 5 members and Employees’ Retirement System (ERS) Tier 6 members are eligible for a vested retirement benefit as early as your 55th birthday.

Police and Fire Retirement System (PFRS) Tier 6 members are eligible for a vested retirement benefit on your 63rd birthday.

For most members, however, if you retire before your full retirement age, you would face a permanent early retirement benefit reduction. The full retirement age is 62 for Tier 1 – 5 members, and age 63 for ERS Tier 6 members and off-payroll PFRS Tier 6 members.

Most members can estimate your pension amount using the benefit calculator in Retirement Online. Sign in to your Retirement Online account, go to the ‘My Account Summary’ area of your Account Homepage and click the “Estimate my Pension Benefit” button. You can also apply for your retirement benefit using Retirement Online.

If You Leave Public Employment with Less than Ten Years of Service

With less than ten years of service credit, you can choose to end your membership and request a refund of your contributions. If you withdraw your contributions, however, you will no longer be eligible to receive a pension benefit. You can withdraw by signing in to Retirement Online, going to the ‘My Account Summary’ area of your Account Homepage, and clicking “Withdraw My Membership.”

You cannot withdraw from NYSLRS once you have ten years of service credit.

(Note: Tier 1 and 2 members and PFRS Tier 3 (Article 11) members covered by a non-contributory retirement plan can make voluntary contributions. These members can withdraw their voluntary contributions without ending their membership. Contact us if you have questions.)

If you have less than five years of service credit (aren’t vested) and don’t withdraw your contributions, they will continue to earn 5 percent interest for seven years. After seven years off the public payroll, your membership ends automatically, and your contributions will be deposited into a non-interest-bearing account until you withdraw them.

NYSLRS membership provides more than just retirement benefits. For most members, if you die while in active service, your beneficiary may be eligible to receive a death benefit. Here is an overview of member death benefits. If you are retired, visit our Death Benefit page for retirees to learn about your available benefits.

Types of Death Benefits

Most members who die while they’re still working will leave their beneficiaries what’s called an “ordinary death benefit.” This is a lump sum payment that’s usually equal to one year of your earnings per year of service, up to a maximum of three years.

Generally, to leave your beneficiaries this death benefit, you must have at least one year of service credit and your death must occur while you are on the public payroll.

Some members who die because of an on-the-job accident (not due to their own willful negligence) may leave their beneficiary an accidental death benefit. The accidental death benefit is a pension payable to your spouse. Other beneficiaries, as specified by law, may be eligible if there is no spouse.

For Employees’ Retirement System (ERS) Tier 4, 5 and 6 members, the benefit would be 50 percent of your earnings from your last year of service.

For most other members, the benefit would be 50 percent of your final average earnings (less any workers’ compensation benefit).

There is no minimum service credit requirement to leave an accidental death benefit.

The specific death benefits that may be available to your beneficiaries depend on your tier and retirement plan. Find Your NYSLRS Retirement Plan Publication and check it for specific benefit amount and eligibility information.

Note: For public employees who contract COVID-19 on the job and die from COVID-19, their beneficiaries may be eligible for an enhanced death benefit. Find out more about the Enhanced Death Benefit for Survivors of COVID-19 Victims.

Review and Update Your Beneficiaries

You should periodically review your beneficiary designations. Life circumstances sometimes change, and the beneficiary you may have named before might not be the one you would choose today. You should also make sure your beneficiary’s contact information is up to date so we can find them when needed.

Retirement Online is the best way to manage your beneficiary information. Sign in to Retirement Online today and click “View and Update My Beneficiaries” to review your named beneficiaries, and update them if needed.

Reporting a Death

NYSLRS cannot pay out death benefits until after we are notified of a member’s death and have a certified copy of the death certificate. The fastest way for survivors to report a member’s death to NYSLRS is using our online form on our website. Survivors can also upload a copy of the certified death certificate, which enables us to start reaching out to the beneficiary. It’s important to talk with your family about your benefits and how to report your death to NYSLRS.

Payment of Death Benefits

NYSLRS will reach out to your beneficiaries on file and send them the application and instructions for receiving benefits. NYSLRS can pay death benefits once it receives the required documentation.

We’ve written about how

We’ve written about how