Ready to retire? Retirement Online makes it fast and convenient to apply for retirement. There are no forms to mail in and nothing to have notarized. If you don’t already have an account, sign up today.

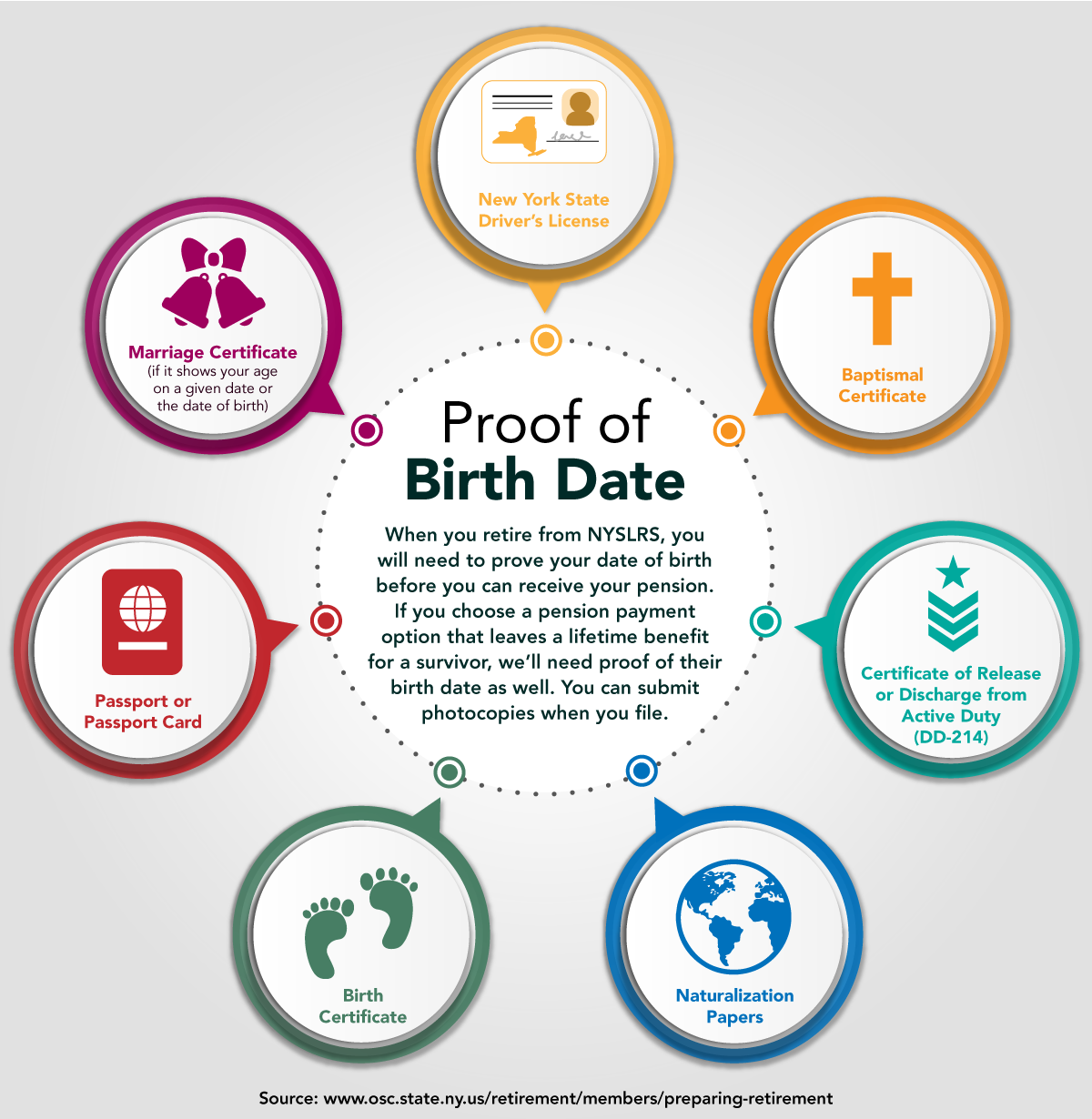

As a reminder, you must submit your application 15 – 90 days before your retirement date. Before you apply for retirement, make sure you have proof of your date of birth on hand. If you choose a pension payment option that leaves a lifetime benefit to a beneficiary when you die, we will need proof of their birth date too.

Retirement Online Makes It Fast and Convenient to Apply for Retirement

Sign up for direct deposit (have your bank account information ready);

Upload required documents, such as proof of date of birth;

Pay off your NYSLRS loan or service credit purchase; and

Review your employment history.

After you click the “Submit” button, make sure you receive a confirmation message that your retirement application has been successfully submitted before closing your browser.

One Exception — Disability Retirement

NYSLRS provides disability benefits for members who are permanently disabled and cannot perform their duties because of a physical or mental condition. Applications for disability retirement can’t be submitted in Retirement Online. Members who wish to apply for a disability retirement need to submit a paper application. Visit our Disability Benefits page for more information.

For Benefit Information, Read Your Retirement Plan Publication

Your service and disability retirement benefits and death benefits are based on your tier, plan, service credit, and other factors. For comprehensive information about your available benefits, find your NYSLRS retirement plan publication.

Brush up on your Retirement System knowledge! Here are 10 things all NYSLRS members should know.

Lifetime Retirement Benefit You are part of a defined benefit pension plan, which provides a lifetime benefit at retirement based on your earnings and years of service.

Qualify for a Retirement Benefit by Becoming Vested Becoming vested is a key milestone in every NYSLRS member’s career. Once you’re vested, you have earned enough service to qualify for a retirement benefit, once you meet the minimum age requirements established by your retirement plan.

Tier Determines Benefits Your tier determines your eligibility for benefits under your plan and how those benefits are calculated.

Conduct NYSLRS Business Using Retirement Online Retirement Online is the fastest and most convenient way to do business with NYSLRS. It only takes a few minutes to open your account. Use Retirement Onlineinstead of calling or mailing for instant access to benefit information and convenient tools to make account changes.

Estimate Pension Using Retirement Online Calculator Most members can use Retirement Online to create benefit estimates based on the most up-to-date information we have on file. You can enter different retirement dates and payment options to see how those choices would affect your benefit.

Use Plan Publication to Learn about Benefits Your retirement plan publication is a comprehensive source for information about your benefits.

Pension Calculated Using Highest Earnings Your final average earnings (FAE) is another major factor in calculating your NYSLRS pension. When we calculate your pension, we find the set of consecutive years (one, three or five, depending on your tier and retirement plan) when your earnings were highest.

Request Past Service Credit Before Retirement Service credit is one of the major factors in calculating your NYSLRS pension. You earn a year of service credit for each year of full-time employment with a participating employer. In some cases, you may also be able to request additional credit for past service.

NYSLRS Membership Includes Death and Disability Benefits NYSLRS membership provides more than just retirement benefits. If you become seriously ill or injured, you may be eligible for a disability benefit. And, you may also be eligible to leave a beneficiary a death benefit if you die while working for a public employer.

Best-Funded, Best-Managed The New York State Common Retirement Fund holds and invests the assets of NYSLRS on behalf of members, retirees and their beneficiaries and continues to be one of the best-funded and best-managed public pension funds in the nation. Comptroller Thomas P. DiNapoli is the administrative head of NYSLRS and trustee of the Common Retirement Fund.

NYSLRS is one of the largest public retirement systems in America, serving more than 1.2 million members, retirees and beneficiaries. Read A Look Inside NYSLRS to learn more about your retirement system.

Becoming vested is a crucial milestone for NYSLRS members. It means you have earned enough service to qualify for a retirement benefit once you meet the age or service requirements established by your retirement plan. Vesting is automatic — you don’t have to fill out any paperwork to become vested.

Years of Service Credit to Become Vested

NYSLRS members in Tiers 2 – 6 need five years of service credit to be vested.

If you work part-time, or if you have an unpaid leave of absence, it will take longer to become vested. For example, if you work half-time, you earn six months of credit toward vesting for each year on the job.

Note: Previously, Tier 5 and 6 members needed ten years of service to be eligible for a service retirement benefit. However, as of April 9, 2022, these members only need five years of service credit to be vested. The new law did not change benefit rules such as how long members must contribute, pension benefit calculations, the full retirement age, reductions to retire early or the cost to purchase previous service.

Applying for Retirement

Vesting is automatic, but you will need to apply for retirement to receive your pension — NYSLRS will not pay out your pension benefit unless you apply for it.

Pension eligibility requirements and benefit calculations depend on your tier and retirement plan. To find your tier and retirement plan, sign in to your Retirement Online account and go to the ‘My Account Summary’ section. Once you know your tier and retirement plan, you can find your retirement plan publication for comprehensive information about your benefits and filing instructions.

A lot can change in our lives, and sometimes people switch jobs or professions during their career. Perhaps you were a teacher, and you recently began working for New York State. Or maybe you had a job with New York City, and you took a position with a municipality outside of the city. If you are an active member of more than one public retirement system in New York State, you may have the option of transferring that membership to NYSLRS and receiving credit for that service.

Considering Service Credit

Service credit is a factor in calculating a NYSLRS pension benefit, so increasing your service credit will generally increase your pension benefit.

In some cases, transferring membership may not be beneficial. For example, if you are in a retirement plan that allows for retirement after 20 or 25 years of service (regardless of age), your service usually must be in specific job titles to be creditable toward your pension benefit. If you are in one of these plans, find your retirement plan publication to learn what service is creditable.

If you have questions, contact a customer service representative before you apply to transfer a membership. You can message them using our secure contact form.

Transferring Membership

Members who are transferring membership to NYSLRS must:

Be on the payroll in a job that is covered by NYSLRS;

No longer work in the job that was covered by the other retirement system; and

Still be an active member of the other system (off payroll for that job, but your membership in the other system has not been terminated or withdrawn).

To transfer a membership to NYSLRS, you first must submit a transfer request to your other retirement system. When we receive your membership information from the other retirement system, we will compare your date of membership in NYSLRS with your date of membership in the other system. When the transfer is complete, your date of membership will be the earlier of the two dates. If applicable, your tier will change.

If You Need to Transfer to Another System

You can submit an online request to NYSLRS to transfer your membership from NYSLRS to another New York State public retirement system:

The New York State and Local Retirement System (NYSLRS) administers two distinct systems. They are:

The Employees’ Retirement System (ERS) with 659,750 members; and

The Police and Fire Retirement System (PFRS) with 35,754 members.

During the State fiscal year that ended on March 31, NYSLRS provided pension benefits to nearly 515,000 retirees and beneficiaries. Altogether, that’s more than 1.2 million participants, making NYSLRS one of the largest public retirement systems in the nation.

New York State Common Retirement Fund

NYSLRS benefits are provided by the New York State Common Retirement Fund. State Comptroller Thomas P. DiNapoli is administrative head of NYSLRS and trustee of the Fund, which is widely recognized as one of the best-managed and best-funded public retirement funds in the nation. It’s also exceptionally enduring; 2021 marked the 100-year anniversary of the Retirement System.

NYSLRS Members

But NYSLRS is more than just the pension fund. Here are some facts about NYSLRS members as of March 31:

514,150 active members (that is, members still on the public payroll) work for 2,979 public employers statewide.

About one-third of those active members work for New York State. The rest work for counties, cities, towns, villages, school districts and public authorities.

Nearly 94 percent of total active members are in ERS. PFRS accounts for 6 percent of total active membership.

Almost 60 percent of all members are in Tier 6.

In ERS, 58.8 percent of members are in Tier 6, while 36.7 percent are in Tiers 3 and 4.

In PFRS, 51.1 percent of members are in Tier 6, while 43.4 percent are in Tier 2.

NYSLRS Retirees and Beneficiaries

The average pension for an ERS retiree was $27,227 as of March 31, 2023; the average for a PFRS retiree was $60,592. But these pension payments don’t just benefit retirees and beneficiaries. About 78 percent of retirees and beneficiaries stay in New York State and generate billions of dollars in economic activity. Their spending supports local businesses, contributes to local taxes and creates jobs in our communities.

October is National Retirement Security Month, a time to learn more about the importance of saving and your potential sources of income in retirement. Even if your own retirement seems far off in the future, it’s never too early to start developing your plans for retirement.

NYSLRS and Retirement Security

Check out these blog posts to learn more about how your NYSLRS pension and other sources of retirement income can provide retirement security.

What is a Defined Benefit Plan? Your NYSLRS pension is a defined benefit retirement plan. When you retire, you’ll receive a guaranteed lifetime benefit based on your earnings and years of service. It will be calculated using a preset formula rather than being limited to your accumulated contributions and your investment returns, as it would be in a 401(k)-style plan.

The 3-Legged Stool: An Approach to Retirement Confidence Think of your retirement security as a three-legged stool — each leg represents a different income source that supports you in retirement. The first leg of the stool is your NYSLRS pension, and the second leg is your Social Security benefit. The third leg is your own personal savings, which can give you more flexibility during retirement, helping to ensure that you’ll be able to do the things you want to do.

Compounding: A Great Way for Your Money to Grow The sooner you can start saving, the better — especially if you have a retirement savings account with compounding interest. When your money is compounded, it increases in value by earning interest on both the principal and accumulated interest. But for your money to make more money, it needs time to grow.

Deferred Compensation: Another Source of Retirement Income Deferred compensation plans are voluntary retirement savings plans. Your contributions will be automatically deducted from your paycheck, and you can contribute as little as 1 percent of your earnings. It’s a savings vehicle to consider if you want to start saving extra for retirement but aren’t sure where to start.

Give Your Retirement Savings a Boost Once you’re on your way and saving for retirement, you may want to look at ways to increase how much you save. Even the smallest increase can make a big difference over time, while having a minimal impact on your take-home pay.

Remember, retirement security doesn’t just happen — it takes planning. Visit our Retirement Planning page for more information about your NYSLRS pension, including an overview of how it’s calculated, estimating your amount and how to find a description of the benefits provided by your specific retirement plan.

A good estimate of your post-retirement income is essential for effective retirement planning. But gauging your income can be tricky when it comes from multiple sources. Fortunately, there are a variety of online calculators that can help you get started.

NYSLRS Benefit Calculator

Most NYSLRS members can quickly create a pension estimate using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit and adjust your earnings or service credit if you anticipate a raise or plan to purchase past service.

If you are saving for retirement, a simple savings calculator can give you an idea of how your money can grow over the years. However, simple calculators like this assume a fixed amount of savings each month. Most people increase their retirement savings as their income grows.

Savings withdrawal calculators are designed to help determine how much savings remains after a series of withdrawals. These are especially helpful tools to use when trying to determine how long your retirement savings will last, based on a starting amount, how much you expect to withdraw, how often and some other factors.

How Much Do You Need?

Now that you’ve estimated your potential sources of retirement income, it’s important to understand your anticipated expenses in retirement. Our Income and Expenses Worksheet can help you create a post-retirement budget.

Think of retirement security as a three-legged stool, with your NYSLRS pension, social security benefit and retirement savings working together to provide financial stability. Your NYSLRS pension is a defined benefit, or traditional pension, that will provide you with a monthly payment for the rest of your life. Having a retirement savings account can give you more flexibility to do the things you want to do, or provide a source of cash in case of an emergency. Start saving for retirement if you haven’t already, or give your retirement savings a boost.

It may not come up during your career, but if you leave public employment before you are eligible to retire, you should know what happens with your NYSLRS membership and benefits. Your options will depend on how many years of service you have. It’s also important to keep your account information up to date. If you remain a member of NYSLRS after you leave public employment, you can regularly review your account information and keep it up to date by using Retirement Online.

If you have 5 or more years of service when you leave public employment, and you leave public employment before you are eligible to retire, you can receive a vested retirement benefit when you become eligible.

If you leave with between five and ten years of service, you can either remain a member and receive a vested retirement benefit when you become eligible or terminate your membership and receive a refund of your contributions.

If you leave with more than ten years of service, you cannot withdraw your NYSLRS membership and you can receive a vested retirement benefit when you become eligible and apply.

If you leave with less than ten years of service, you can end your membership and receive a refund of your contributions.

Keep Your Contact Information Updated

It’s important to make sure we have your current mailing address, phone number and personal email address, and let us know about any future changes. That way, you won’t miss important information from us, such as your Member Annual Statement.

To update your contact information, sign in to Retirement Online. Go to ‘My Profile Information,’ find your address, phone number or email address under ‘My Profile Information’ and click “update.”

Keep Your Beneficiaries Updated

If you leave public employment, your beneficiaries may still be eligible for a death benefit, so you should review your beneficiary designations periodically. Sign in to Retirement Online, go to the ‘My Account Summary’ area of your Account Homepage and click “View and Update My Beneficiaries.” Your beneficiary changes will be considered filed on the day you submit them.

Repay Any NYSLRS Loans

If you leave public employment, you will no longer be able to pay off your NYSLRS loans by payroll deduction. If you have any outstanding NYSLRS loans, you must make payments directly to NYSLRS at least once every three months and repay your loan within five years of when it was issued, or you will default on the loan. Defaulting on a loan may carry considerable tax consequences: You’ll need to pay ordinary income tax and possibly an additional 10 percent penalty on the taxable portion of the loan. You can make loan payments to NYSLRS via Retirement Online.

You aren’t eligible to take a new NYSLRS loan once you are off the public payroll.

Receiving a Vested Retirement Benefit

If you are vested, once you reach retirement age, you can receive a lifetime pension based on your salary and service from when you were working in public employment. It’s your responsibility to apply for retirement — NYSLRS will not pay out your pension benefit unless you apply for it.

The earliest date you can receive your retirement benefit depends on your tier and retirement system.

Tier 1 and 2 members are eligible for a vested retirement benefit as early as the first of the month following your 55th birthday.

Tier 3, 4 and 5 members and Employees’ Retirement System (ERS) Tier 6 members are eligible for a vested retirement benefit as early as your 55th birthday.

Police and Fire Retirement System (PFRS) Tier 6 members are eligible for a vested retirement benefit on your 63rd birthday.

For most members, however, if you retire before your full retirement age, you would face a permanent early retirement benefit reduction. The full retirement age is 62 for Tier 1 – 5 members, and age 63 for ERS Tier 6 members and off-payroll PFRS Tier 6 members.

Most members can estimate your pension amount using the benefit calculator in Retirement Online. Sign in to your Retirement Online account, go to the ‘My Account Summary’ area of your Account Homepage and click the “Estimate my Pension Benefit” button. You can also apply for your retirement benefit using Retirement Online.

If You Leave Public Employment with Less than Ten Years of Service

With less than ten years of service credit, you can choose to end your membership and request a refund of your contributions. If you withdraw your contributions, however, you will no longer be eligible to receive a pension benefit. You can withdraw by signing in to Retirement Online, going to the ‘My Account Summary’ area of your Account Homepage, and clicking “Withdraw My Membership.”

You cannot withdraw from NYSLRS once you have ten years of service credit.

(Note: Tier 1 and 2 members and PFRS Tier 3 (Article 11) members covered by a non-contributory retirement plan can make voluntary contributions. These members can withdraw their voluntary contributions without ending their membership. Contact us if you have questions.)

If you have less than five years of service credit (aren’t vested) and don’t withdraw your contributions, they will continue to earn 5 percent interest for seven years. After seven years off the public payroll, your membership ends automatically, and your contributions will be deposited into a non-interest-bearing account until you withdraw them.

If you’re planning to retire soon, it’s a good idea to take inventory of any debt you owe. Paying down your debt can give you flexibility to enjoy the type of retirement you want.

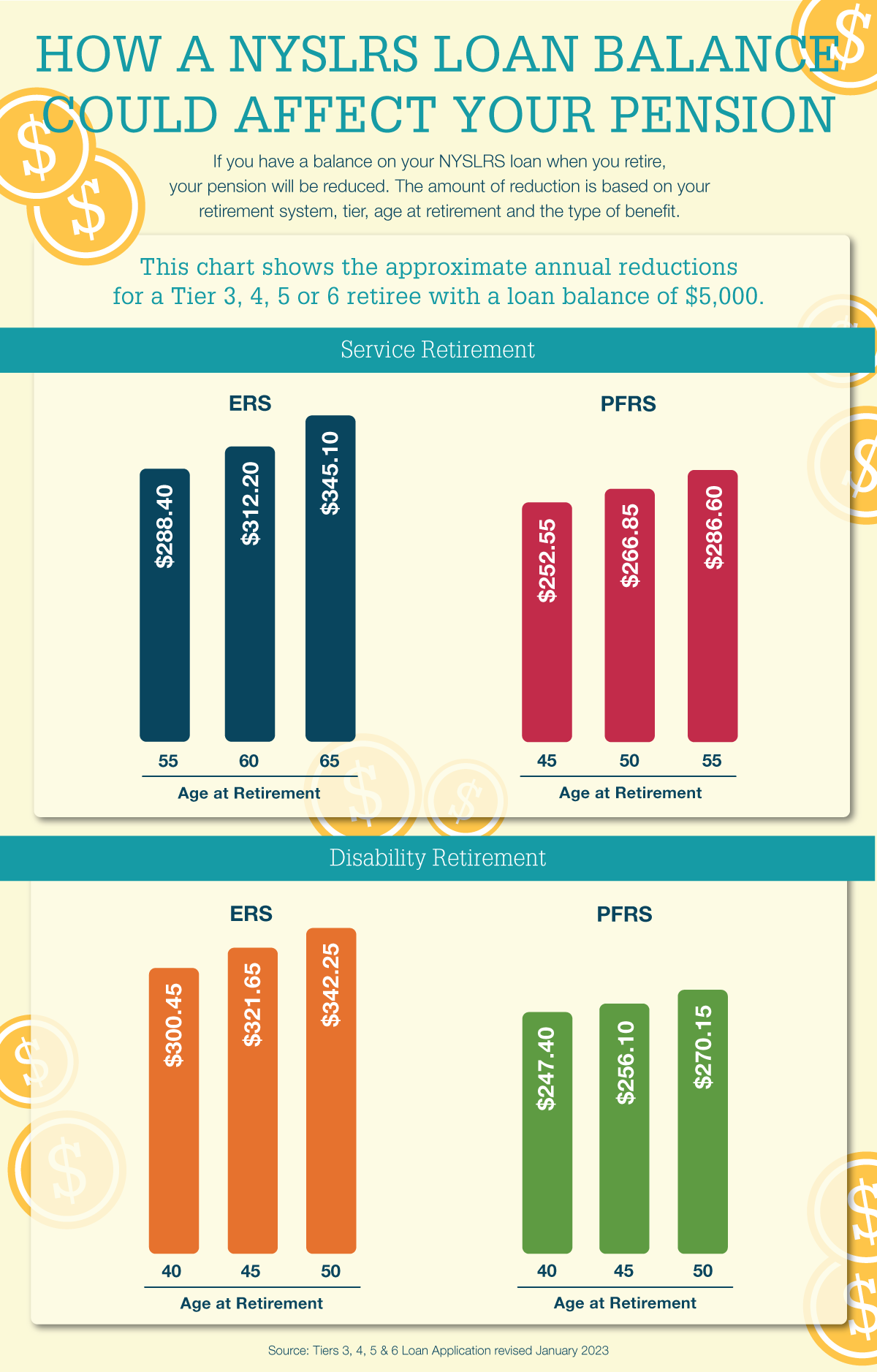

NYSLRS Loan Debt

If you have an outstanding NYSLRS loan balance when you retire, it will reduce your pension. The amount of your reduction is based on:

Your retirement system — Employees’ Retirement System (ERS) or Police and Fire Retirement System (PFRS);

Your tier;

Your age at retirement; and

Whether you retire with a service retirement benefit or a disability retirement benefit.

The pension reduction does not go toward repaying the outstanding loan balance — it’s a permanent reduction. And, at least part of the loan balance at retirement will be subject to federal income taxes.

When you apply to retire using Retirement Online and have an outstanding NYSLRS loan balance, the pension reduction amounts are provided to you. They are also listed on the loan applications on our Forms page. If you are nearing retirement, be sure to check your loan balance. If you are not on track to repay your loan before you retire, you can increase your loan payments, make additional lump sum payments or both (see the Change Your Payroll Deductions or Make Lump Sum Payments section of our Loans page.)

Although ERS members may repay their loan after retiring, they would have to pay the full balance that was due at retirement in a single lump sum payment. Then, going forward, the pension would be increased to the amount it would have been without the loan reduction. However, it would not be increased retroactively back to the date of retirement.

Other Debt to Check

Credit Cards

Another priority is paying off credit cards. Credit card statements carry a minimum payment warning that tells you how long it will take, and how much it will cost, to pay off your balance making only minimum payments.

If you have more than one credit card balance, many financial advisors recommend you pay as much as you can on the card with the highest interest, while making at least the minimum payments on lower-interest cards. Once you’ve paid off the high-interest card, focus on the one with the next-highest rate, and so on. Other advisors say it might be better to pay off the card with the smallest balance first. The idea is to gain a sense of accomplishment, and make the process seem less daunting.

Mortgages

Should you try to pay off your mortgage before you retire? Advice varies on that question. It would eliminate a major expenditure and let you spend your retirement income on other things. On the other hand, if your mortgage interest rate is relatively low, you may want to focus on paying off other high-interest debt or boosting your retirement savings. What works best for you will depend on your situation.

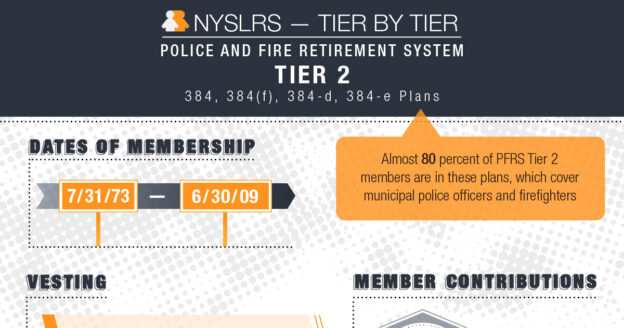

When you join the New York State and Local Retirement System (NYSLRS), you’re assigned a tier based on the date of your membership. This post looks at Tier 2 members of the Police and Fire Retirement System (PFRS).

Your tier determines such things as your eligibility for benefits, the calculation of those benefits, death benefit coverage and whether you need to contribute toward your benefits.

PFRS has five tiers. Almost half of PFRS members are in Tier 2, which began on July 31, 1973, and ended on June 30, 2009. Most are in special retirement plans that allow for retirement after 20 or 25 years, regardless of age, without penalty.

The special plans that cover most police officers and firefighters fall under Sections 384, 384(f), 384-d, and 384-e of Retirement and Social Security Law. You can sign in to Retirement Online to find your benefit plan, which is listed under ‘My Account Summary.’

Where to Find PFRS Tier 2 Information

Whether you’re in one of the retirement plans described in this post or another retirement plan, we encourage you to visit our website to find your NYSLRS retirement plan publication. It’s a comprehensive description of the benefits you’re entitled to receive as a PFRS member.

You can check your service credit total and estimate your pension using Retirement Online. Most members can use our online pension calculator to create an estimate based on the salary and service information NYSLRS has on file for them. You can enter different retirement dates to see how your choices would affect your potential benefit.

Members may not be able to use the Retirement Online calculator in certain circumstances, for example, if they have recently transferred a membership to NYSLRS, if they are a Tier 6 member with between five and ten years of service, or if they have worked for multiple employers and were covered by different retirement plans. These members can contact us to request an estimate or use the “Quick Calculator” on our website. The Quick Calculator generates estimates based on information you provide.

{kind=link}