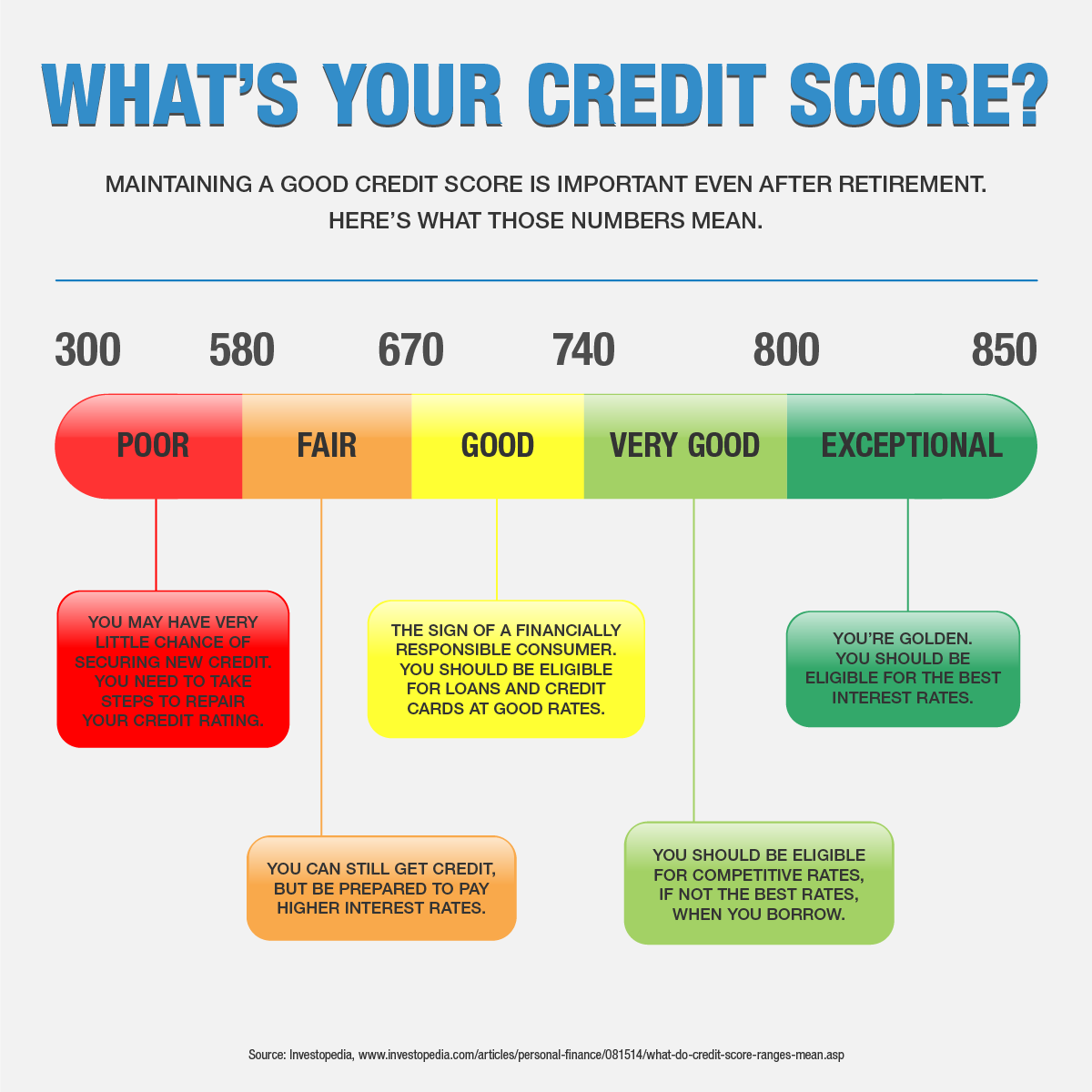

Striving to maintain a good credit score is just as important in retirement as it is during your working years. You may be retired, but financial necessities continue. You may need to get a car loan or refinance a mortgage, and good credit ensures you can borrow money at a decent interest rate. In fact, bad credit could prevent you from renting an apartment, or you may be required to pay higher insurance premiums. Fortunately, it seems maintaining good credit is just a matter of continuing what you’ve already been doing.

What is a Credit Score?

Your credit score is a three-digit number used by lenders to judge how likely you are to pay back money you’re loaned. It’s based on your past payment history and other interactions with lenders. These three digits affect you more than you might realize.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance. They are also used to determine the interest rate and credit limit you receive.”

How to Maintain a Good Credit Score

The best way to maintain your credit score is to borrow responsibly and manage debt effectively. That means:

Pay your bills on time. Pay more than the minimum payments if you can. Your payment history accounts for about a third of your credit score.

Avoid using all or most of your available credit. The ratio of debt to available credit is another factor in your credit. If all your credit cards have balances near the limit, your credit score will suffer.

Keep longstanding credit lines open. These accounts show your long history of being responsible with credit and help to boost your score.

Don’t accumulate excessive debt. You especially want to avoid opening several lines of credit in a short amount of time.

Things like age and salary are not part of the credit score equation, so being retired does not hurt your score. However, lenders do take income into account when you apply for a loan, so you may find it harder to borrow after retirement, even if you have good credit.

Check Your Credit Reports Annually

Even if you’re doing everything right, misinformation in the files of credit rating companies could hurt your credit. So, check your credits scores regularly.

Under federal law, the three nationwide credit reporting companies are required to provide a free credit report once every 12 months. But you must request it. You can request your credit report online at AnnualCreditReport.com or by calling 877-322-8228. AnnualCreditReport.com is a website maintained by the three major credit reporting agencies—Equifax, Experian and TransUnion. It is the only free credit report site authorized by the federal government. Beware of impostor sites.

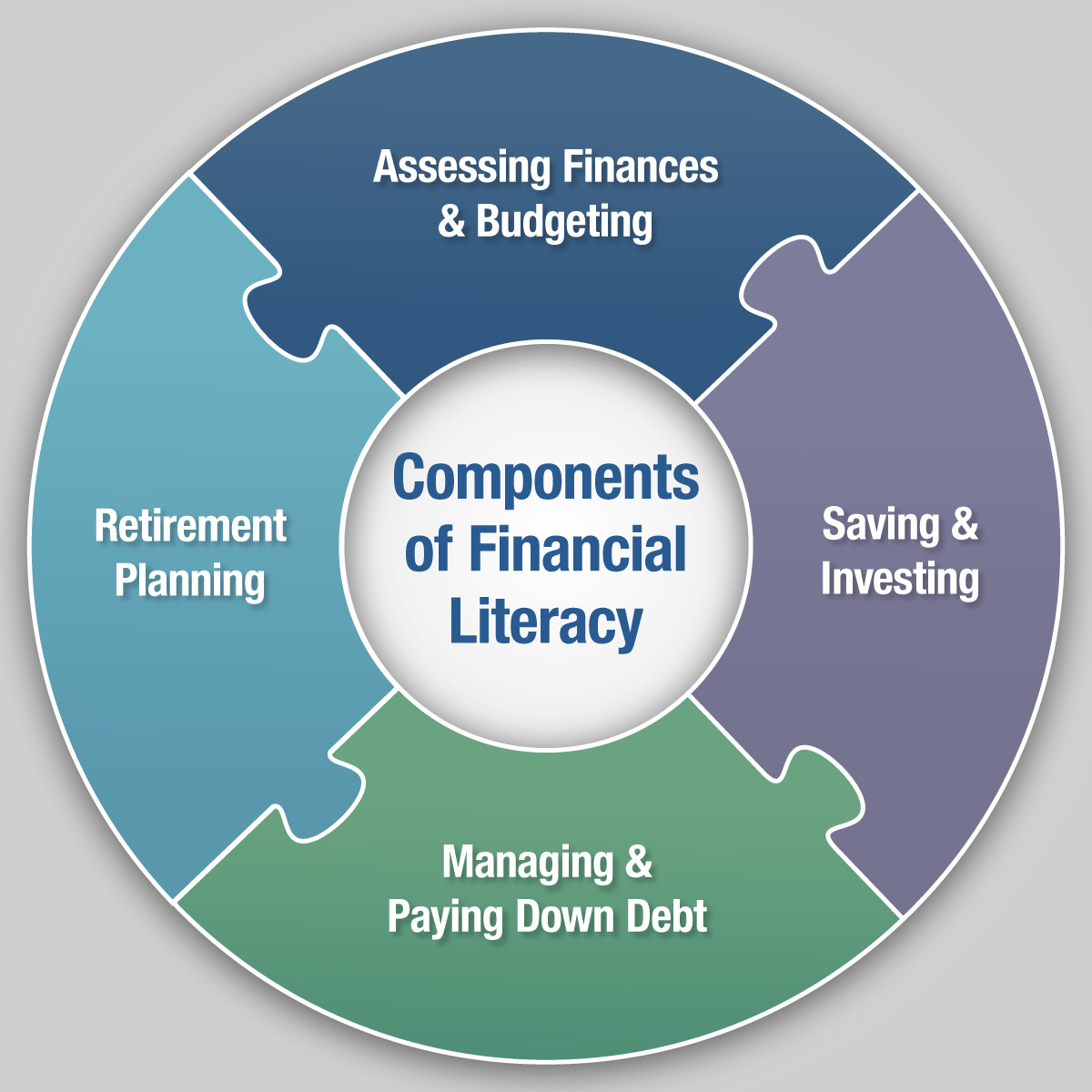

April is National Financial Literacy Month, a time dedicated to helping people make informed financial decisions and manage money effectively. Financial literacy means understanding and applying various skills of personal finance management, including budgeting, planning, saving and investing.

Financial literacy is essential for effective retirement planning. When you understand your NYSLRS benefits, your other sources of retirement income and your current financial situation, you’ll be in a better position to plan for retirement.

Key Components for Financial Literacy

Assessing Finances and Budgeting

Whatever your goals, wherever you are in life, a clear-eyed assessment of your finances and effective budgeting are necessary. The 50/30/20 budget rule is one framework that can help you with both. It’s a popular way to start and stick to a budget that can work whether you’re just out of school looking at your first paycheck or retired and trying to make your savings last.

Divide Your Expenses

The idea is to divide your expenses into three categories: needs, wants and savings.

Needs are things you have to pay and can’t avoid—for example, housing costs, food, healthcare, childcare and utilities.

Wants are optional expenses. They may be fun or convenient, but they aren’t essential—for example, dining out, shopping, entertainment and vacations.

Savings& Managing Debt can help you grow your retirement assets (see more under Retirement Planning and Saving and Investing below) or build an emergency fund. This category also includes paying down debt—such as student loans or credit card balances—beyond minimum payments.

Budget Your Spending

Then, you allocate your after-tax income, with 50 percent going to needs, 30 percent to wants and 20 percent to savings. As you budget, make sure you include expenses that occur periodically, such as car and life insurance, and property and school taxes.

Managing debt is an important aspect of financial literacy. Throughout your life, you’ll need to maintain good credit, borrow responsibly and repay your debt diligently.

Credit Scores

Your credit score is a three-digit number used by lenders to judge how likely you are to pay back money you’re loaned. It’s based on your past payment history and other interactions with lenders. These three digits affect you more than you might realize.

According to the Consumer Financial Protection Bureau (CFPB), “Companies use credit scores to make decisions on whether to offer you a mortgage, credit card, auto loan, and other credit products, as well as for tenant screening and insurance. They are also used to determine the interest rate and credit limit you receive.”

Even if you’re doing everything right, misinformation in the files of credit rating companies can hurt your credit. So, check your credits scores regularly. You can do it online at AnnualCreditReport, the free-credit-report site authorized by the federal government and maintained by the three major credit reporting agencies.

Responsible Borrowing

The best way to maintain your credit score is to borrow responsibly and manage debt effectively. That means:

Pay your bills on time; pay more than the minimum payments if you can.

Avoid using all or most of your available credit.

Keep longstanding credit lines open (like a credit card you’ve had for many years).

Avoid accumulating excessive debt—especially opening several lines of credit in a short amount of time.

If you have more than one credit card balance, many financial advisors recommend paying as much as you can on the card with the highest interest rate, while still making at least the minimum payments on your lower-interest cards.

Debt is not necessarily bad, but if you’re planning to retire soon, paying it down can give you more flexibility to enjoy the type of retirement you want.

Retirement Planning

Retirement is a big step. In many ways, confidence in a comfortable retirement is the reason saving and building financial literacy throughout our lives is so important.

Understand Your Sources of Income in Retirement

As a NYSLRS member, you are enrolled in something increasingly rare these days: a defined benefit plan. If you are vested and retire from NYSLRS, you will receive a monthly pension payment for the rest of your life based on your years of service and earnings.

However, your pension is just one of three main sources of income in retirement. Think of retirement security as a three-legged stool. Each leg is a source of income, and you need all three for a stable retirement.

Your NYSLRS pension is a guaranteed lifetime benefit. Find your retirement plan publication for comprehensive information about your pension and the other benefits you are entitled to receive. Most NYSLRS members can estimate their pension benefit in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit.

Your Social Security benefit is another source of income to help support you in retirement. At Social Security’s full retirement age, your benefit can replace a significant portion of your pre-retirement income, depending on how much you earned while working. You can estimate your benefit on the Social Security Administration website.

In addition to your NYSLRS and Social Security benefits, retirement savings can be an important financial asset when you retire. Savings can give you flexibility to travel, continue your education, pursue a hobby or start a business. It can be a resource in case of an emergency, act as a hedge against inflation and boost your retirement confidence.

Determine How Much You’ll Need in Retirement

Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement.

Use our Monthly Income & Expenses Worksheets to help you track your current spending habits and project your future needs. Remember to account for non-monthly expenses, such as car insurance, property taxes and school taxes.

If you’re already building your retirement savings, think about giving your savings a boost. Even a small increase could make a big difference over time.

For New York State employees and many other NYSLRS members, there’s an easy way to get started. If you work for a participating employer, you can join the New York State Deferred Compensation Plan. If you don’t work for New York State, check with your employer to see if you are eligible. If you are not eligible, your employer may be able to direct you to an alternative retirement savings program.

Most NYSLRS members can create their own pension estimates in minutes using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates and beneficiaries to see how those choices would affect your benefit. When you’re done, print your pension estimate or save it for future reference.

Remember, the amounts are estimates, not a guarantee of what you’ll receive when you retire.

Most Tier 2 through 6 members (more than 90 percent of all NYSLRS members) can use the Retirement Online pension calculator. However, some members may not be able to—for example, members who recently transferred to NYSLRS and some PFRS members. The system will let you know if your estimate cannot be completed. In that case, please send us a message using our secure contact form (select Estimates from the Topic dropdown).

Do More With Retirement Online

In Retirement Online, you can view your account details—date of membership, tier, retirement plan, estimated total service credit and more. Check out what else members can do in Retirement Online.

NYSLRS retirement plans provide death benefits for beneficiaries of eligible members who die before retiring.

It’s important to name beneficiaries and review them periodically. Life circumstances change and a beneficiary you named before might not be one you would choose today. For instance, you may have a new partner or you may have children now. And NYSLRS can only pay a death benefit to the beneficiaries you’ve named.

Your primary beneficiary will receive your death benefit. You can list more than one primary beneficiary. If you do, they will share the benefit equally. Or, you can choose different percentages for each beneficiary, which must total 100 percent. (Example: John Doe, 50 percent; Jane Doe, 25 percent; and Mary Doe, 25 percent.)

A contingent beneficiary will only receive a benefit if all your primary beneficiaries die before you do. If you list multiple contingent beneficiaries, they will share the benefit equally unless you choose different percentages.

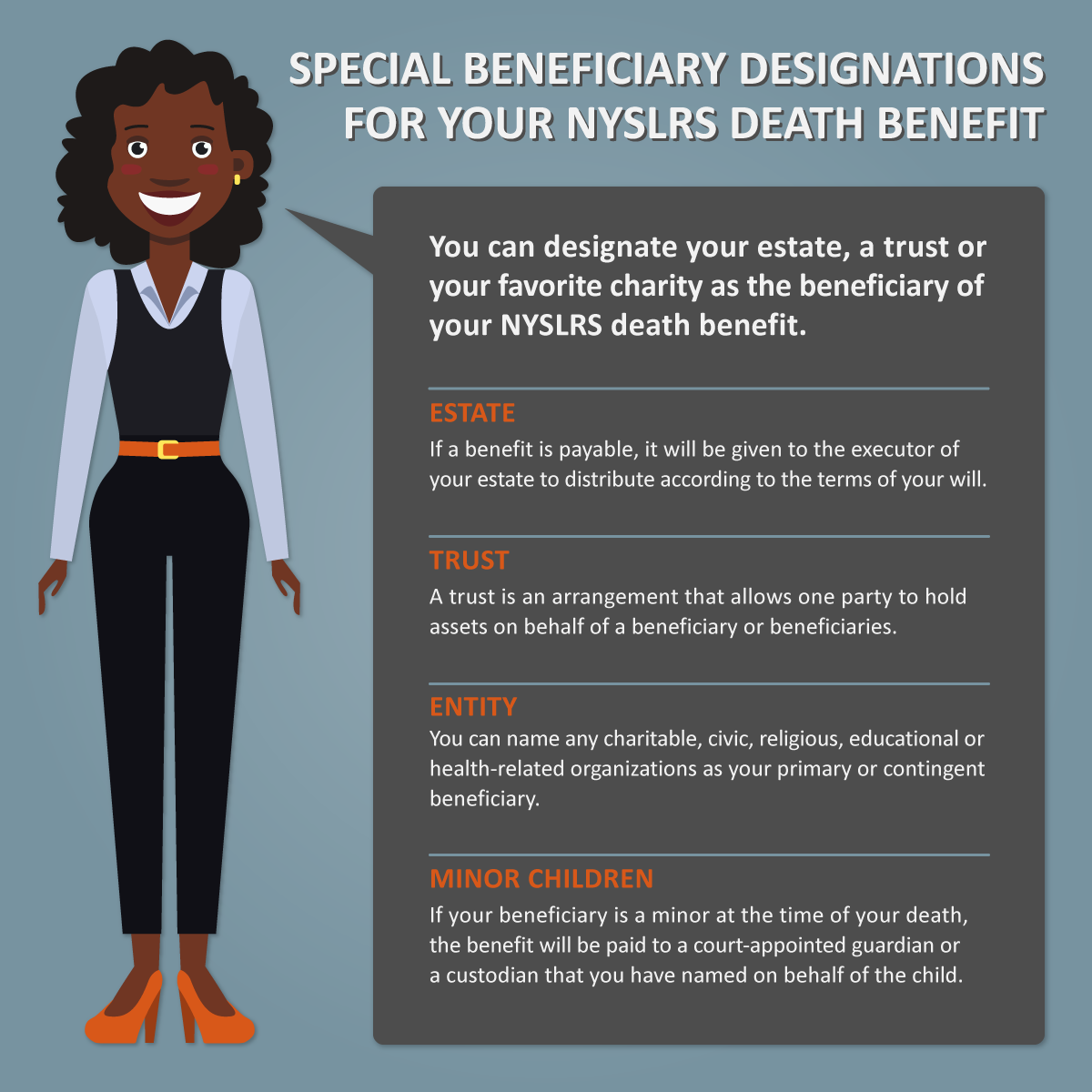

Special Beneficiary Designations

Your beneficiary doesn’t have to be a person. You can name your estate, a trust or a charity as your beneficiary.

Estate. When you die, your estate is the money and property you owned. Your death benefit will be given to the executor of your estate to be distributed according to the terms of your will. You can name your estate as the primary or contingent beneficiary of your death benefit. If you name your estate as the primary beneficiary, do not name a contingent beneficiary.

Trust. You can name a trust as a primary or contingent beneficiary if you have a trust agreement or provided for a trust in your will. The trust itself would be your beneficiary, not the individuals for whom you established the trust. (Speak with your attorney if you’re thinking about making your trust a beneficiary.)

Entity. You can also name any charitable, civic, religious, educational or health-related organization as a beneficiary.

Minor children. If your beneficiary is under the age of 18 at the time of your death, your benefit will be paid to the child’s court-appointed guardian. You may instead choose a custodian to receive the benefit on the child’s behalf under the Uniform Transfers to Minors Act (UTMA). Custodians can be designated in Retirement Online, or you can contact us for more information and the appropriate form before making this type of designation.

Keep Your Beneficiaries Up to Date with Retirement Online

You can change your beneficiaries at any time. In addition to adding or removing them to reflect your current wishes, you should review the contact information for your named beneficiaries so we can find them when needed.

The fastest way to view or update your beneficiaries is in Retirement Online.

Many financial experts cite a common rule of thumb when discussing income in retirement. They say you need 70 to 80 percent of your pre-retirement income to maintain your standard of living once you retire. This is meant to account for the range of expenses you’ll no longer have in retirement, such as payroll taxes, commuting costs or saving for retirement. As a NYSLRS member, your plan for income in retirement likely includes your NYSLRS pension and Social Security benefits. However, for greater financial stability and flexibility, you may want to supplement with retirement savings. For example, you might start investing in a savings plan like the New York State Deferred Compensation Plan (NYSDCP).

What is Deferred Compensation?

Deferred compensation plans are voluntary retirement savings plans like 401(k) or 403(b) plans—but designed and managed with public employees in mind. NYSDCP is the 457(b) plan created for New York State employees and employees of other participating public employers in New York.

Just like with other retirement savings plans, you have options for how you make your NYSDCP contributions. You might choose a tax-deferred account where you make contributions with pre-tax money. With this option, you won’t pay State or federal taxes on the earnings you contribute until you start making withdrawals. Your employer may also offer the option for a Roth account where you make contributions with after-tax money. With this option, you do pay taxes now, but you won’t pay taxes on the withdrawals you make in retirement. Learn more about how traditional retirement savings and Roth accounts compare.

If your employer is not an NYSDCP participating employer, check with your human resources or personnel office about other retirement savings options.

What Does Deferred Compensation Mean for Me?

Deferring income from your take-home pay may mean less money to spend in the short-term, but you’re planning ahead for your financial future.

As a NYSLRS member, you are enrolled in something increasingly rare these days: a defined benefit plan. If you are vested and retire from NYSLRS, you will receive monthly pension payments for the rest of your life based on your years of service and earnings. Your NYSLRS pension can provide a significant part of your retirement income, but it’s a good idea to supplement your pension and Social Security with a retirement savings account.

Additional retirement savings can give you flexibility to travel, continue your education, pursue a hobby or start a business. It can be a resource in case of an emergency or act as a hedge against inflation.

Your Retirement Savings Goal

How much you save is a personal decision. You can estimate your pension in Retirement Online to get an idea of the income it will provide in retirement. Use a retirement savings calculator to see how much a retirement savings plan could yield over time. Test the results with different savings amounts.

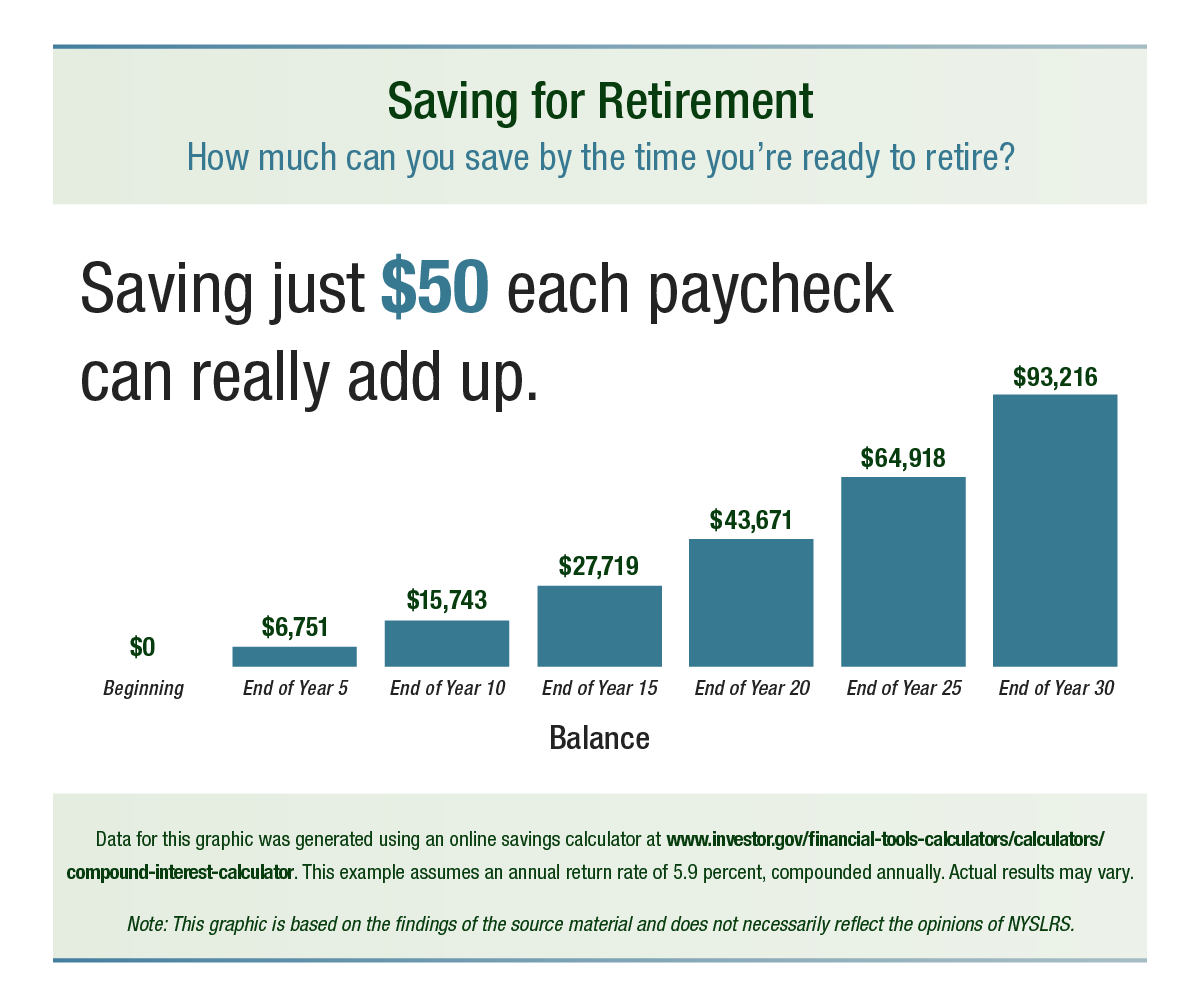

Below you can see the potential savings of someone who invests 50 dollars every two weeks for 30 years. While the stock market can be turbulent in the short term, in the long term, it returns on average about 10 percent a year as measured by the S&P 500 index.

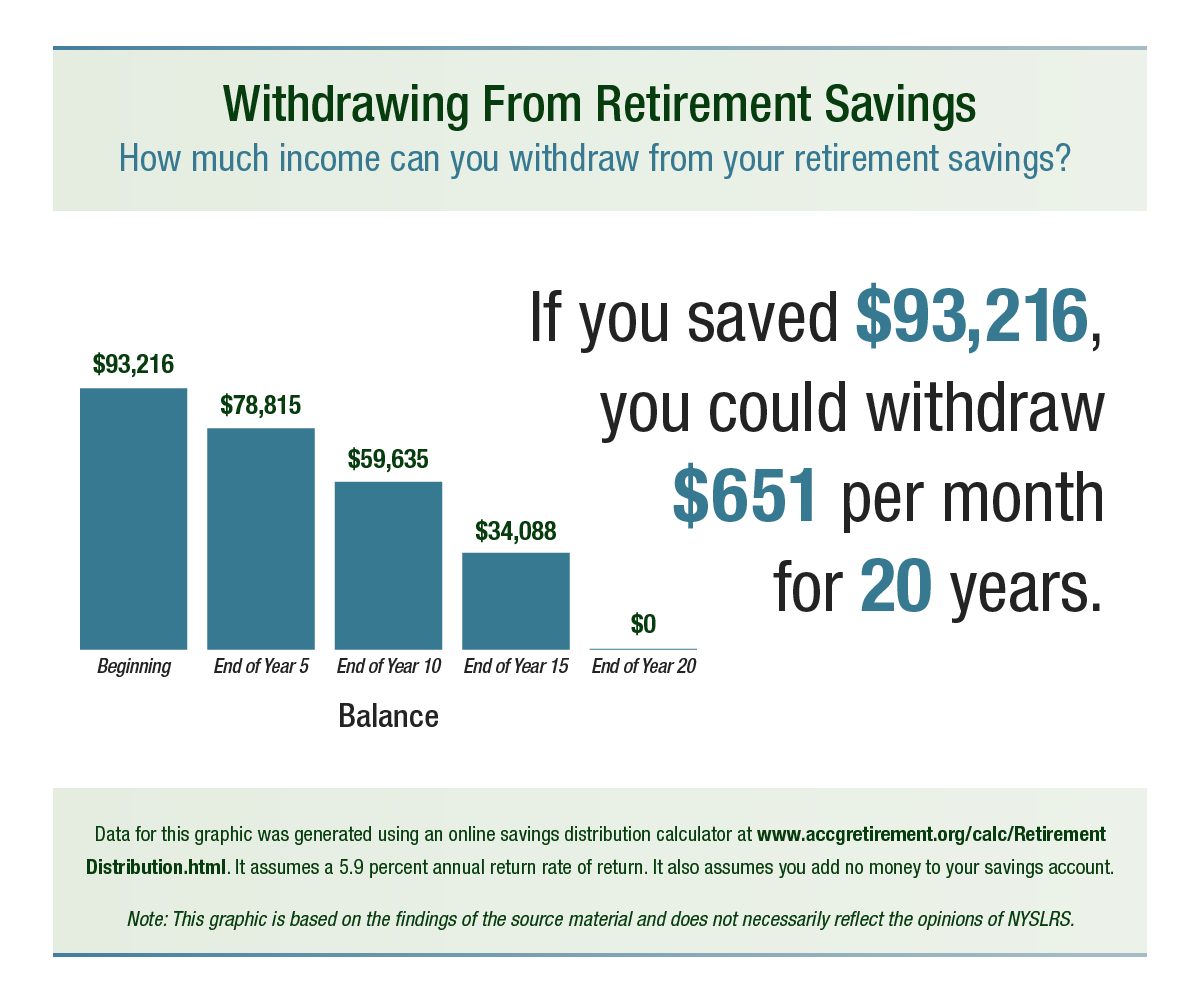

As you get closer to retirement, you should develop a plan to withdraw money from your savings. That will give you a better idea of the income you might expect from your nest egg and a sense of how long it will last.

Here is one possible withdrawal strategy, which provides retirement income for 20 years. Please note, if your retirement is far in the future, the money you withdraw may not have the same value that it would have today.

If you find you’ll need to save more to meet your goal, you can make adjustments to help ensure you’ll have enough savings in retirement.

Note: Generally, whatever your withdrawal strategy, federal law will eventually require you withdraw a certain amount each year from any tax-deferred retirement plan account. These are called required minimum distributions.

New York State Deferred Compensation Plan

One way State employees and many municipal employees can save for retirement is through the New York State Deferred Compensation Plan (NYSDCP). Once you’ve signed up, your retirement savings—which may be tax-deferred depending on the plan you choose—will be automatically deducted from your paycheck.

Check with your employer’s human resources or personnel office to see whether they participate in NYSDCP or if they offer other savings options. (NYSDCP is not affiliated with NYSLRS.)

Read More About Retirement Savings

When it comes to saving for retirement, there’s a lot to consider. You can find more information in these posts:

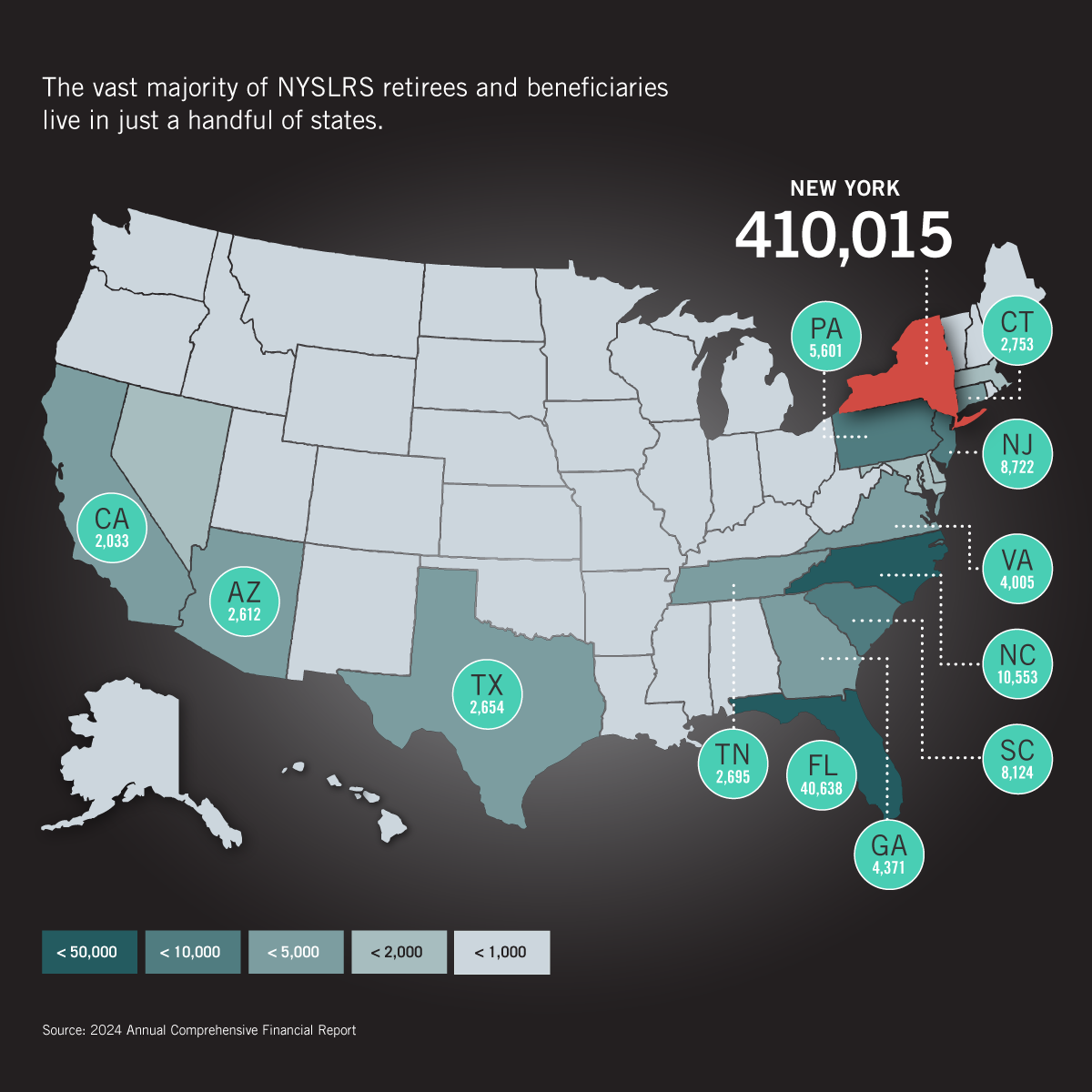

NYSLRS provides pension benefits to more than 520,000 retirees and beneficiaries. You can find our retirees in every state in the US and in countries all around the world. However, most live right here in New York State.

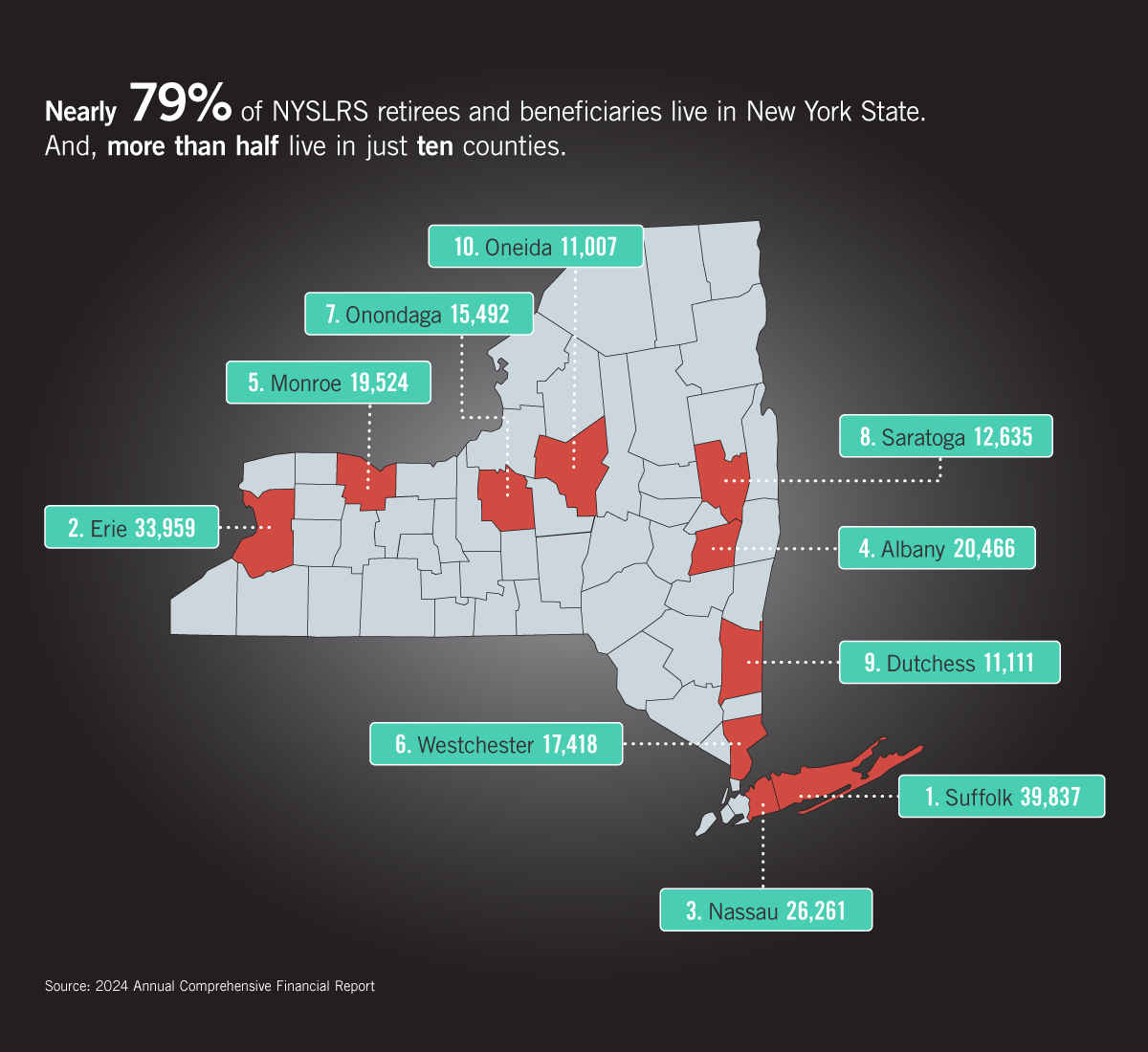

Nearly 79% of NYSLRS Retirees Stay in New York

The vast majority of NYSLRS retirees—nearly 79 percent—stay in New York State, and their pension dollars flow right back into our communities. Retirees in New York pay local property and sales taxes. Their spending supports local businesses, generates thousands of jobs and stimulates the economy.

Where in New York do these retirees call home?

Long Island is home to more than 66,000 retirees and beneficiaries. Suffolk County has the most and Nassau County has the third most benefit recipients of the counties outside of New York City. (The City, which has its own separate retirement systems for municipal employees, police and firefighters, has more than 24,000 retirees and beneficiaries.)

Erie County, which includes Buffalo, has the second most retirees—nearly 34,000. Albany County, home to the State capitol, is ranked fourth, with more than 20,000. Monroe, Westchester, Onondaga, Saratoga, Dutchess and Oneida Counties round out the top ten.

All told, retirees and beneficiaries in the top ten counties received $7 billion in retirement benefits in the fiscal year ending March 31, 2024.

Hamilton County has the fewest retirees. But, in this sparsely populated county in the heart of the Adirondacks, those 545 retirees represent about 10 percent of the county’s population and received $12.9 million in retirement benefits in the fiscal year ending March 31, 2024.

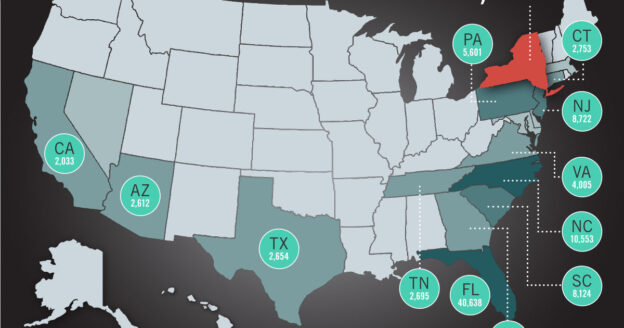

NYSLRS Retirees in the United States

NYSLRS retirees are found in every state. Florida, not surprisingly, is the second choice for retirees after New York. Roughly 41,000 call the Sunshine State home. North Carolina is third, followed by New Jersey and South Carolina. North Dakota has the fewest retirees and beneficiaries—only 23.

NYSLRS Retirees Around the World

There are 649 NYSLRS retirees and beneficiaries living around the world but the most common countries are:

If you’re planning to retire soon, it’s a good idea to take inventory of any debt you owe. Paying down your debt can give you flexibility to enjoy the type of retirement you want.

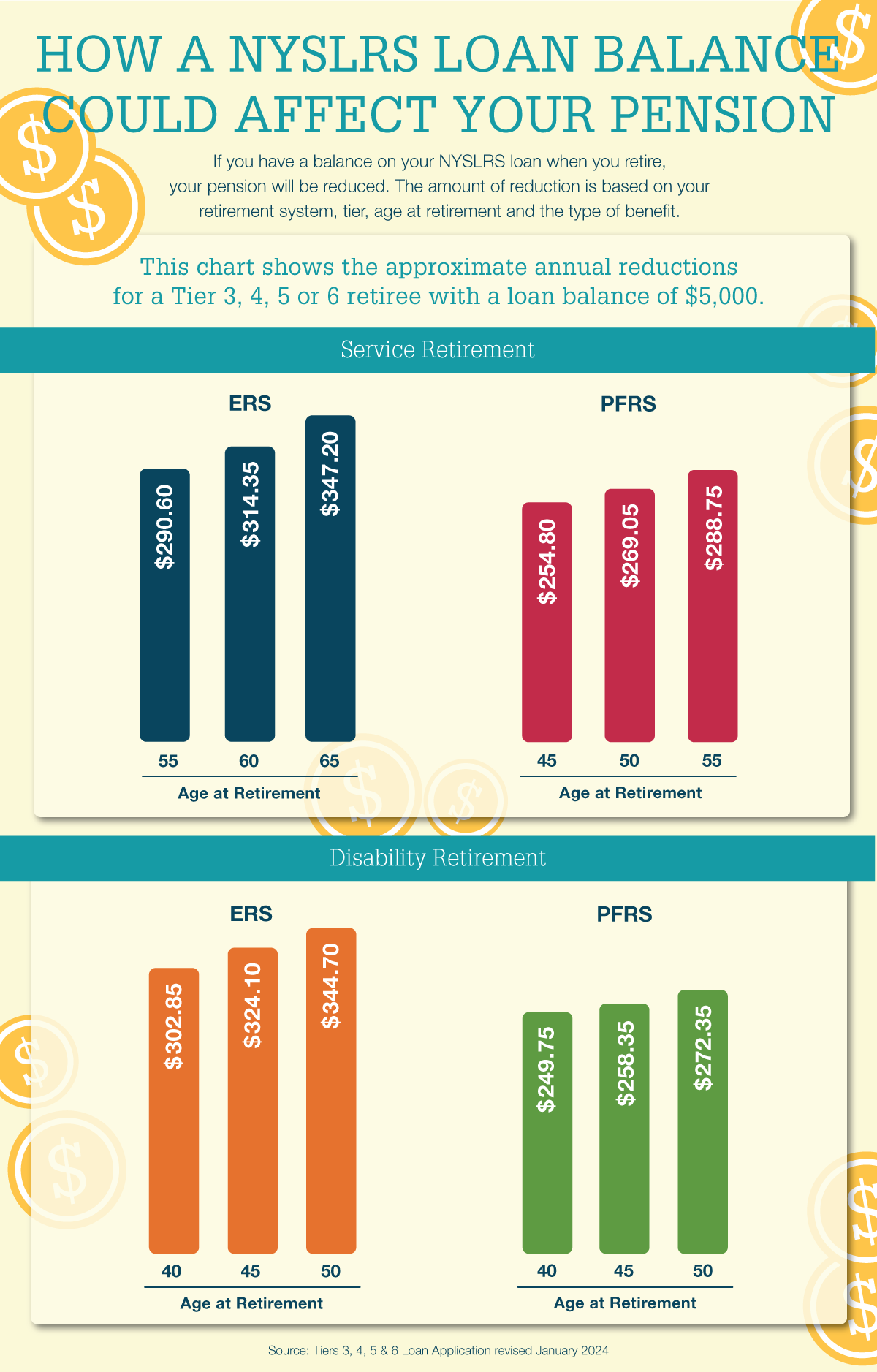

NYSLRS Loan Debt

If you have an outstanding NYSLRS loan balance when you retire, it will reduce your pension. The amount of the reduction is based on:

Your retirement system—Employees’ Retirement System (ERS) or Police and Fire Retirement System (PFRS);

Your tier;

Your age at retirement; and

Whether you retire with a service retirement benefit or a disability retirement benefit.

It is important to understand:

The reduction does not go toward repaying the outstanding loan balance—it’s a permanent reduction to your pension.

At least part of the loan balance at retirement will be subject to federal income taxes.

ERS members may repay a loan after retiring. They must pay the full balance that was due at retirement in a single lump sum payment. Once they repay the loan, their pension will increase to the amount it would have been without the loan reduction. It will not increase retroactively back to the date of retirement.

Other Debt to Check

Credit Cards

Another priority should be paying off credit cards before retirement. Credit card statements include a warning telling you how long it will take—and how much it will cost—to pay off your balance making only minimum payments.

If you have more than one credit card balance, many financial advisors recommend paying as much as you can on the card with the highest interest rate, while still making at least the minimum payments on your lower-interest cards. Once you’ve paid off your highest-interest card, focus on the one with the next-highest rate, and so on. Other advisors say it might be better to pay off the card with the smallest balance first. The idea there is to gain a sense of accomplishment, and make the process seem less daunting.

Mortgages

Advice varies on whether you should try to pay off your mortgage before you retire. It would eliminate a major expenditure and let you spend your retirement income on other things. On the other hand, if your mortgage interest rate is relatively low, you may want to focus on paying off other high-interest debt or boosting your retirement savings. What works best for you will depend on your situation.

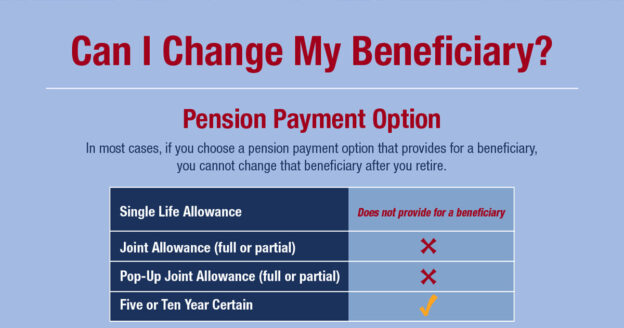

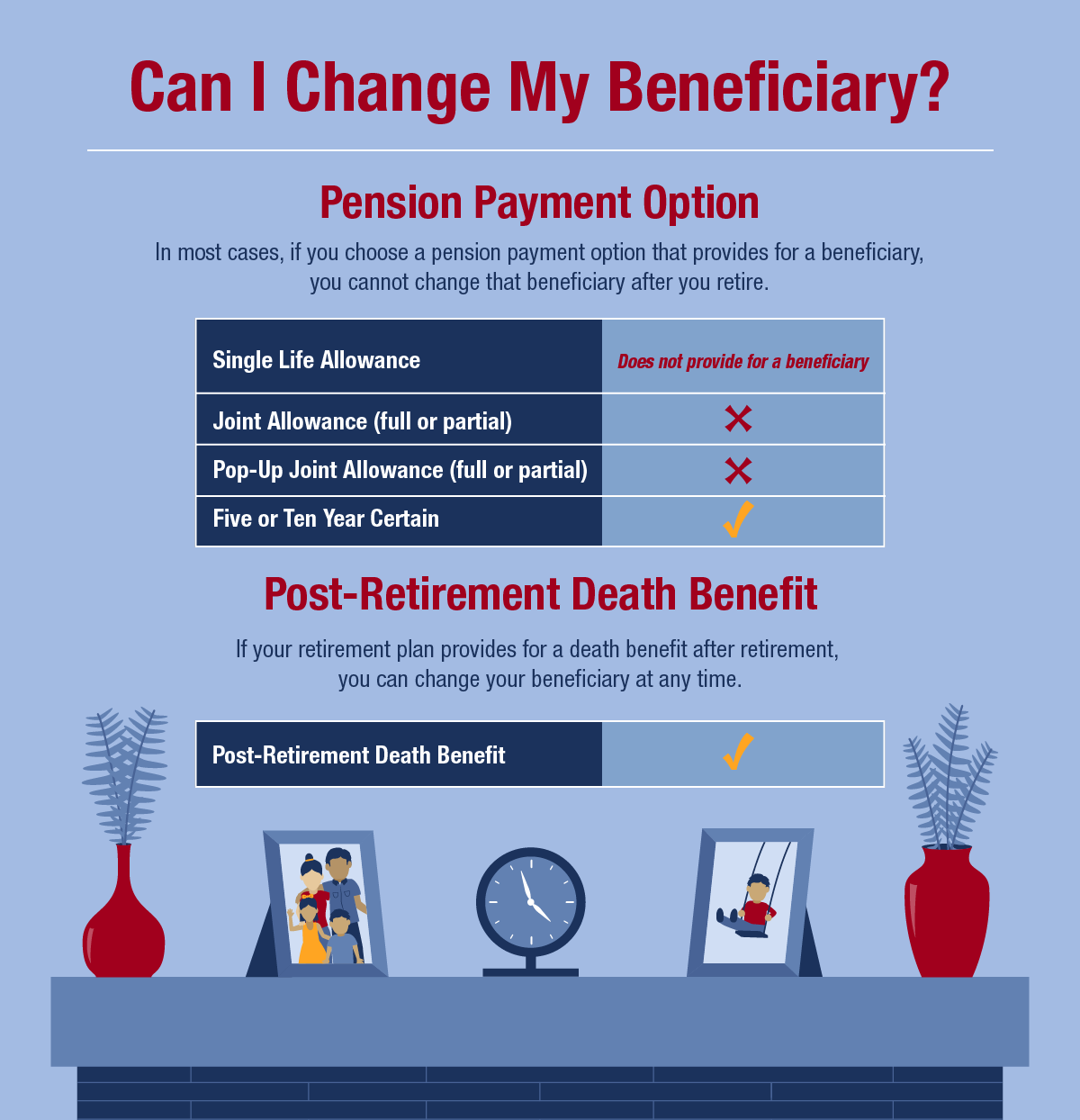

That depends. If you choose a pension payment option that provides a lifetime benefit for a beneficiary, you cannot change your beneficiary even if they die before you do. However, if you choose a pension payment option that provides a benefit for a certain period after retirement, you can change your beneficiary after you retire. Learn more about the different pension payment options and whether they allow you to change your beneficiary below.

If your retirement plan provides a one-time lump sum death benefit after you retire, you can also change your beneficiary (or beneficiaries) for that benefit.

Single Life Allowance option: Provides the maximum monthly benefit payment to you for the rest of your life. This option does not provide a continuing benefit so you will not select a beneficiary, and all payments stop when you die.

Joint Allowance options:Provide a lifetime benefit to a loved one in exchange for a reduction to your monthly benefit payment. After your death, your beneficiary will continue to receive your pension (or part of it, depending on the option you choose) for the rest of their life. If your beneficiary dies before you, your monthly benefit payment remains the same and all payments stop when you die. However, if you choose one of the Popup-Up/Joint Allowanceoptions and your beneficiary predeceases you, your monthly benefit payments will increase to the amount payable under the Single Life Allowance option. For these options, you can only choose one beneficiary, and you cannot change your beneficiary after you retire.

Five Year Certain or Ten Year Certain options:Provide a benefit for a certain period after retirement in exchange for a reduction to your monthly benefit payment. If you die within the five- or ten-year period after your retirement (depending on the option you choose), your beneficiary will continue to receive your monthly pension payment for the remainder of the five- or ten-year period. For these options, you can choose more than one beneficiary, and you can change your beneficiary after you retire.

Post-Retirement Death Benefit

Your pension is not your only NYSLRS retirement benefit. Most NYSLRS retirees are eligible to leave a death benefit if they retired directly from payroll or within one year of leaving employment. The post-retirement death benefit is a one-time lump sum payment. For information on how it’s calculated, visit our Death Benefits for Retirees page.

You can change your beneficiary for this benefit at any time, and your beneficiaries for this benefit do not have to be the same as your pension payment option beneficiary.

Manage Your Beneficiaries in Retirement Online

The fastest way to view or update your beneficiaries for your post-retirement death benefit is in Retirement Online.

A good estimate of your post-retirement income is essential for effective retirement planning. But gauging your income can be tricky when it comes from multiple sources. Fortunately, there are a variety of online calculators that can help you get started.

NYSLRS Benefit Calculator

Most NYSLRS members can quickly create a pension estimate using Retirement Online. Your estimate will be based on the most up-to-date account information we have on file for you. You can enter different retirement dates to see how those choices would affect your benefit and adjust your earnings or service credit if you anticipate a raise or plan to purchase past service.

If you are saving for retirement, a simple savings calculator can give you an idea of how your money can grow over the years. However, simple calculators like this assume a fixed amount of savings each month. Most people increase their retirement savings as their income grows.

Savings withdrawal calculators are designed to help determine how much savings remains after a series of withdrawals. These are especially helpful tools to use when trying to determine how long your retirement savings will last, based on a starting amount, how much you expect to withdraw, how often and some other factors.

How Much Do You Need?

Now that you’ve estimated your potential sources of retirement income, it’s important to understand your anticipated expenses in retirement. Our Income and Expenses Worksheet can help you create a post-retirement budget.

Think of retirement security as a three-legged stool, with your NYSLRS pension, social security benefit and retirement savings working together to provide financial stability. Your NYSLRS pension is a defined benefit, or traditional pension, that will provide you with a monthly payment for the rest of your life. Having a retirement savings account can give you more flexibility to do the things you want to do, or provide a source of cash in case of an emergency. Start saving for retirement if you haven’t already, or give your retirement savings a boost.